Better Vibes

Monday 22 August 2022

The US Federal Reserve, fighting headline inflation in both literal and cultural terms, is starting to make progress. Markets have actually done a pretty good job this year, discounting the likely path of both US monetary policy and the economy itself, as each struggle with the inflation problem. The stock market went through a painful six month valuation reset to better reflect the dilutive effect inflation would have on corporate earnings. The bond market, at the short end, started pumping up the yield on the 2 Year Treasury last October which, acting like a hard brake on the economy, sent ripples through the US housing market—which has now rolled over. And the futures market, which attempts to price in the path of rate hikes, also adjusted ever upward to reflect a far more aggressive monetary policy when inflation readings became sticky.

But these were responses to the front end of the Fed’s tightening campaign, and now we’re at a different place along that journey. The latest data release on CPI for example showed that month-over-month inflation actually fell to zero. That’s just one data point, and a short one at that, but together with multiple arrows turning downwards globally, it’s probably much closer to signal, than noise. Production, manufacturing, and demand globally are very weak, for example, and it’s partly why the price of oil has finally come down along with all other commodities, from copper to cotton. Global growth has been downgraded mainly on the back of a very sluggish China, a Eurozone that’s already in recession, and now the ebbing of demand in the US. So, for those expecting US inflation to eventually stop growing, last month’s reading was less of a surprise, and more of an inevitability. Even Federal Reserve real time inflation forecasts have started to come down. Indeed, after the big .75% increase in Fed Funds last month, markets now believe the FOMC will not repeat a hike of that size again, and will instead go with a .50% hike this September.

Fighting inflation is not straightforward however, given the blunt tool of interest rate hikes. This is especially true now that inflation is a global problem. Complicating the effort further is that a great deal of inflation turns on psychology, and the perception of the future. That’s why a central bank relies at least as much on words, yes words, to bring inflation down because the establishment of credibility in a fiat based system is a way to set broad expectations. Some think the US Federal Reserve lost this credibility, if only momentarily, during the past year. So the tough talk, the hawkish posturing, and the constant drumbeat of Fed speechmaking this year has clearly had a singular aim: making sure the public hears loud and clear that the Fed is engaged in the fight.

Put another way, the Fed knows it must fight inflation “in the streets.” It’s not enough to fight inflation through the monthly release of dry government and market data. The average person has no idea how to find the CPI webpage, and to be honest, even educated people need to go through a short learning curve to figure out what it all means. When the Fed started indicating therefore that it wanted to fight “headline inflation” which technically on one level is an actual data term referring to the trailing 12 months of inflation data, some light criticism developed that in doing so, the Fed would be fighting lagging data, and ignoring future risks. But in a broad sense, “headline inflation” refers to political conversations on AM talk radio, the front page of the news blaring out the latest inflation data points, and of course actual prices of gasoline, butter, and meat. The Fed wants to drill directly into the public consciousness a very basic idea: whatever challenges you’re currently having because of inflation, those challenges will recede soon.

This leads us to a policy paradox, which is perhaps the best way to describe our current position. Powell, in his remarks after July’s FOMC meeting, finally began to acknowledge that tightening was beginning to have real impact. While on one level this merely acknowledges changing reality, critics pointed to the stock market rally as evidence that Powell had somehow undermined the inflation-fight. And when the Fed minutes were released, we learned that a group of less hawkish FOMC members—referencing the risk of going too far too fast— was starting to emerge. It’s not surprising some FOMC members are starting to admit there are risks in tightening too fast. The tightening campaign has been compressed into a very short time span. But now the paradox: will acknowledging progress on inflation by Powell and the Fed lead to a backtracking in progress, on inflation?

Yields on longer-term US bonds meanwhile have generally fallen the past two months, but importantly, the peak still stands. The decline in rates at the long end has slowed however as the market understandably began to sniff out the possibility that the US may not be headed for a major recession if inflation is indeed tamed, because then the Fed could slow down its pace of hikes or stop altogether. Some may find this math overly complex but here is an easy way to think about it: any set of gathering forces that point to a future recession will cause the yields on long term bonds to fall. And any set of gathering forces that point to economic growth will either cause long term bond yields to rise, or to stop falling. Markets are currently poised between the two outcomes, waiting for further information.

Emotions have also been running high about inflation, to the point where many believe it will take ages to bring it back down to 2.00%. But what if inflation falls faster than those beliefs? What if monthly inflation starts consistently running around zero: sometimes flat, sometimes negative, or just slightly above positive? In such a case, the “headline” inflation figure will still take quite a while to move down, given its lagging-data construction. But will markets respond to the headline figure, if the monthly inflation reading steadily falls? Not a chance. Market will respond to the leading edge, not the trailing data.

Inflation in the United States has now peaked. This alone doesn’t imply that any decline would be rapid. Rather, it’s the data on housing, the global economy, energy prices, commodity prices, and supply chain improvements that suggest not only that the decline has started, but that it could be rapid.

A sentiment extreme occurs when a vast majority of people come to believe in a view so intensely that it becomes difficult to pry them away, from that view. We have seen a number of sentiment extremes this year and the contrarian surprise dynamic is alive and well. Right as everyone believed the stock market would fall another 20%, it actually rose 20%. Just as everyone accepted gasoline prices would stay elevated for a long while, they too reversed, and started falling. Imagine if you formed a political message based on the belief that gasoline prices would never decline? And now we see the same happening with inflation. Not just in the CPI, but in myriad industrial surveys here in the US of prices paid. And the final piece of the puzzle: public expectations of inflation are falling steadily now, as evidenced by recent University of Michigan surveys.

Inflation is going to continue agitating the global economy. But the rate and the intensity of that agitation is weakening. That change alone probably leads to an improvement in global economic conditions. And markets may be probing now for that possibility. Vibes—the less quantified area of human perception—are improving.

Coda: there are myriad data points from the past 60-90 days that were already pointing to the peak inflation. Here, one of the more unique framings is cited, because again it suggests we’re finally getting good signals, and not just noise, that inflation is rolling over:

ICE sales in China are set to fall for a fifth consecutive year, as EV sales explode higher. From a peak at over 28 million sales in 2017, ICE sales in China are set to fall below 20 million this year. This decline represents both the opportunity, and the challenge, of energy transition more broadly. Growth of clean(er) technologies is powering forward. Legacy technologies still have a firm grip, however, on the world.

In previous issues The Gregor Letter has spoken to the 5% market share phenomenon, and how that repeatedly shows up as a takeoff point for new technologies. In China EV adoption we continue to have a textbook example of this dynamic. In 2018 and 2019, EV sales stalled just below the 5% market share level. In 2020, with the total market down due to the pandemic, EV finally got over the 5% share hurdle—but not by much. And then with three trailing years stuck near the 5% level, the market took off, reaching 13.4% last year, and on pace to reach over 22% this year.

Adoption curves are mostly produced by three forces. Two of them obvious: the new technology gains, and the old technology hangs on, but starts losing. The less obvious force: overall market compression. Usually in transitions, consumers hold on longer to the old technology, having already decided in their mind to adopt the new one—but just not yet. That delay, which defers demand to the near future, can temporarily reduce overall sales in the total market. While it’s tricky to apply this lens during a period also experiencing disruption from the pandemic, it still likely holds true. We’ve seen the same phenomenon in Europe and the UK. When diesel sales started to collapse in the UK, for example, it didn’t necessarily translate into an offsetting surge in ICE sales for the simple reason that the public was on alert that investing in certain cars, during a period of policy change, might be a bad bet. In China, you can see that since the advent of EV, total vehicle sales have gently drifted downward for five years straight.

Will total sales rise again? Probably. Once demand can be more fully met by EV, annual sales will likely rise again, as China becomes a market fully dominated by electrics. Leaving aside the idiosyncrasies of license-plate distribution domestically, or whether production constraints may appear, China’s vehicle market is on course to flip easily to majority EV before the end of the decade. This year, the path points to a 22% share, but some forecasters actually think EV reach at least 25% by the time 2022 closes out, with EV sales totaling 6 million in a 24 million unit market. The march to 12 million EV in that same market therefore could happen in just 3-4 years. (As always, readers are encouraged to go through the archives to obtain ongoing coverage and data of energy transition issues. See for example the 7 February 2022 Gregor Letter for an explanatory on oil demand displacement from EV adoption.)

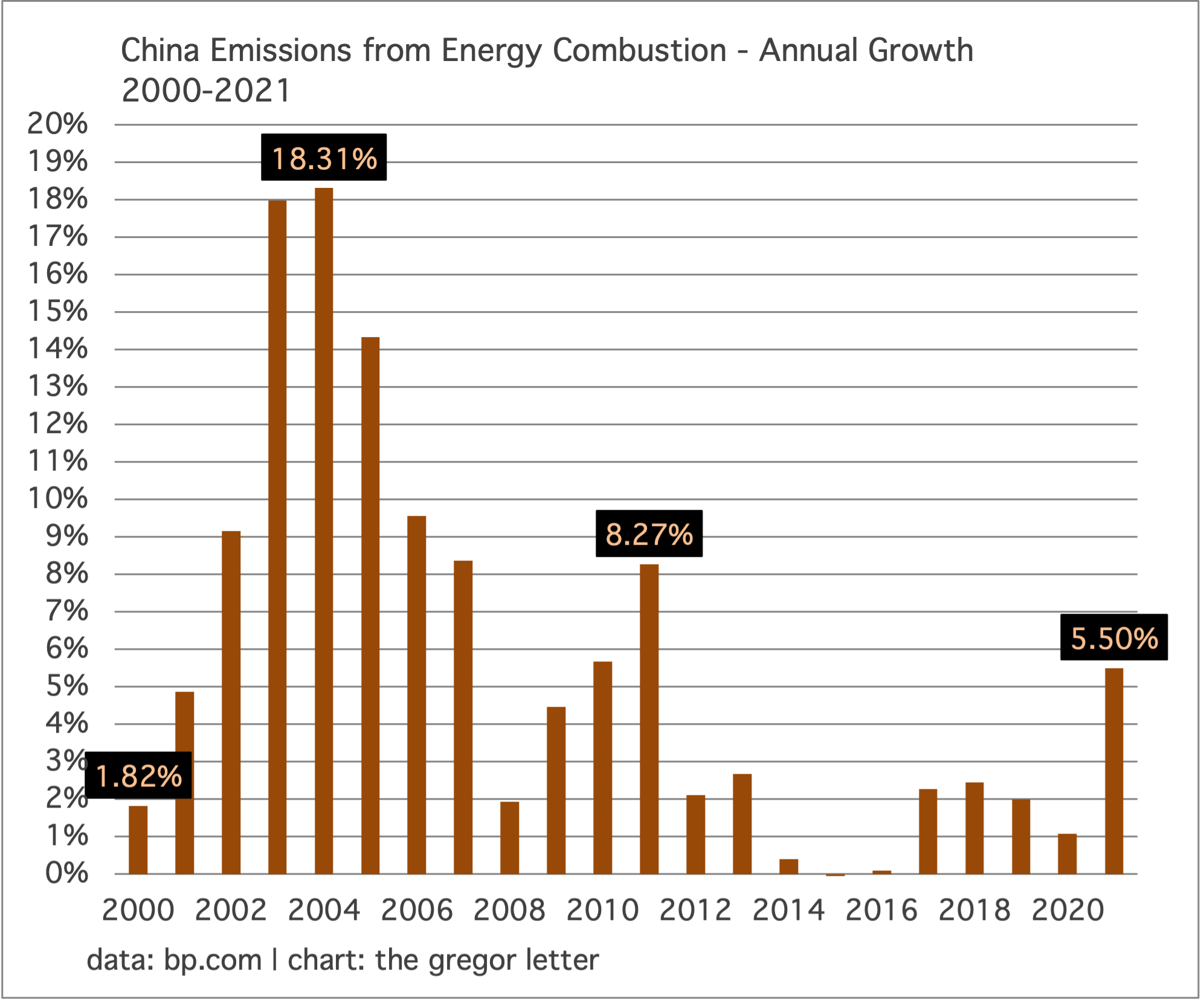

Annual growth of emissions in China has slowed greatly this past decade. While encouraging, this means that emissions have merely stalled at an exceedingly high level. In 2021, the world produced 33884 million tonnes of CO2 from energy combustion. But China accounted for 10523 of those million tonnes, or 31%. (For comparison, the US produced 4701 million tonnes and the EU 2728 million tonnes).

Some analysts are actually entertaining the idea that Chinese emissions will soon peak. Well, if China’s economy was structured like the US, where transportation is the top source of emissions, that idea might be worth pursuing as EV roar and ICE vehicles retreat. But China’s emissions output is largely from its industrial base. And last year, its idle coal capacity was put to work. That’s the 5.5% spike you see on the chart. So, until China starts massively adopting lower emissions techniques to make steel, cement, and other industrial products, we are not near peak emissions, even a little. That said, flattening of growth must occur first before declines can set in. Prospecting for a peak therefore is probably worth the effort.

The American public’s reaction to high petrol prices will deepen the belief among the political class that cars remain a third rail, never to be touched. The Gregor Letter has hit this theme repeatedly, so will refrain from tediously rehashing old material. To be fair, the car enjoys solid cultural protection in much of the world, and the US is not the only domain where tendencies lean hard on the status quo. China maintains a bottleneck on car registrations, especially in its largest cities, but China never really attacked ICE vehicles, preferring instead to incentivize EV while also building a robust EV output capability. Europe has very high petrol prices via taxation—something the US has forgone for decades—but Europe also leads with incentives, rather than penalties. So, this is just to remind that the historic climate bill just passed does not move the policy needle on oil consumption in any new direction. Such is the oil trap. Dependency on oil leads to public eruptions of negativity when petrol prices rise, but any effort to curtail that dependency also would lead to higher costs, in the short term, for ICE owners. That short term reality drives policy, entirely. Notice that US politicians won’t consider higher petrol taxes or congestion charges even when petrol prices are low. If not then, well, never.

Keep your eye on the hydrogen space, as the US climate bill represents a big bang for the sector. Briefly, hydrogen’s biggest promise targets the industrial sector’s dependency on fossil fuels to generate heat, and mainly, high heat. For that to happen, however, a kilogram of hydrogen must be made through electrolysis, using 1. clean electricity that is itself made with wind, solar, nuclear, or hydropower; 2. an electrolyzer whose capital costs must be affordable enough to deliver an economically competitive unit of hydrogen; and 3. a network that can deliver hydrogen to where it’s needed.

The US climate bill concentrates mainly on a tax credit or subsidy that would make clean hydrogen (sometimes referred to as green hydrogen) competitive first with natural-gas produced hydrogen (sometimes referred to as gray hydrogen). The US has plenty of new wind and solar to add to its hydropower and nuclear fleet, so sourcing clean electricity is already not a challenge. Where the hurdles come, however, is in the cost of an electrolyzer and establishing a supply network that locates hydrogen production

Let’s take a live example: Alaska Airlines is currently working with ZeroAvia to retrofit existing Q400 aircraft with hydrogen engines. Without getting into other aspects of this story (for example, the scale of the Q400 and the size of its engines makes a hydrogen retrofit optimal, whereas these designs would not work for a 737) what Alaska Air needs most here is affordable hydrogen. Why? Because at its Seattle hub, Alaska is already in a location where the local grid has a high penetration of clean electricity (hydro, wind, and solar). Accordingly, all Alaska Air needs is a price break on making clean hydrogen, something that would take it down from the $5-6 dollar/kilogram level to the $3 dollar level where natural gas made hydrogen already sits. The climate bill does just that.

Alaska also has another edge in this equation: demand. You see, an electrolyzer is a large and expensive piece of capital equipment. If you run that equipment 60 or 80 hours a week, rather than 20-40 hours a week, your payback on investment is improved. This is a lens to the other challenge in hydrogen: deploying clean hydrogen production capacity means not only sourcing all-renewable energy to drive electrolysis, or a near term subsidy to make it affordable, but requires a strong demand source to make the longer term economics of production work out.

Readers may be interested to know that, based on previous reporting in the hydrogen sector by your editor, the Department of Energy is both keenly aware of and very much focused on the demand factor in hydrogen economics. Accordingly, it’s reasonable to assume that in conjunction with the provisions of the new legislation, the first big forays into clean hydrogen production will arise in locations where demand sources can be relied on to be strong: aviation, petrochemicals, industrial parks.

The megadrought in the US West is simply awful in every way. California hydropower production has collapsed, from a high of 43,303,189 MWh in 2017 to 14,566,394 MWh last year. Here is a time-lapse of Lake Mead, over just the past three years, where levels are the lowest since 1937. Note: we are seeing aerial photography of dried up lakes and rivers now all over the world, from Europe to Asia.

—Gregor Macdonald