Downed Wires

Monday 26 May 2025

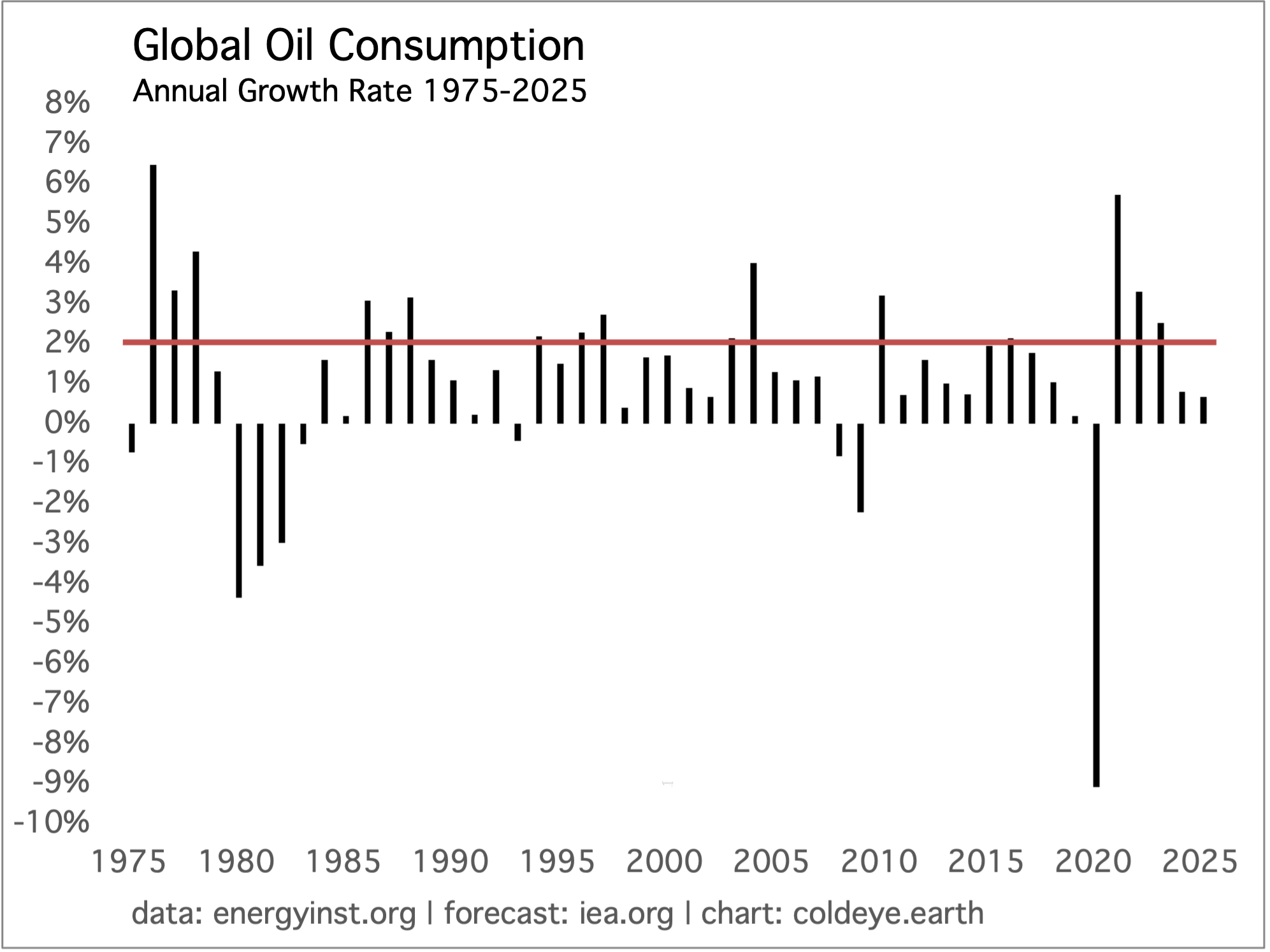

Global adoption of electric vehicles continues to place a steady drag on the growth of oil demand. While this displacement process is slow, due to the constant lengthening of the fleet turnover cycle, total on-road fleet of global EV avoided roughly 1.3 mbpd (million barrels per day) of consumption in 2024, according to a new report from the IEA. Now, 1.3 mbpd of annual consumption savings is small in absolute terms—just a bit more than 1% in a market that consumes around 102 mbpd. But compared to marginal growth, which in recent years has run at a slower annual pace, the savings are quite significant. EV adoption is taking place in an era when annual oil demand growth is already weaker, compared to much of the 20th century. And now, EV adoption itself is adding to the downward pressure. For a long while, it was typical for annual oil demand growth to either reach or exceed 2%. In recent times however, oil demand has either struggled to exceed 2% growth or more often has fallen back to 1.0 - 1.5%.

While global oil demand is now currently around 102 mbpd, the oil market’s price setting mechanism is driven by the 1 -2 mbpd of oscillation of demand that occurs from year to year. Push annual demand growth to 2.00% of more, and prices will strengthen notably. Relax demand growth to 1.00% or below, and market pricing will also relax. After rebounding from the pandemic lows, global oil demand rose only 0.78% last year, and is expected to only grow by 0.67% this year, according to the IEA. That’s just not enough to support oil prices and explains the current weakness, as oil trades in the low 60’s. Just to remind: those are dirt cheap prices on an inflation adjusted basis.

The IEA’s report forecasts that by the year 2030, EV adoption will be displacing 5 mbpd. Progress to be sure, but not exactly revolutionary. The current trajectory of EV adoption, combined with the enormous path dependency of oil, is probably enough to bring demand growth to a sustainable flatline (if we are not there already). But the economics of EV adoption are not aggressive enough to remove economically viable ICE vehicles from the working fleet. EV don’t render existing ICE so worthless that they can be tossed away. This is now a familiar theme to readers of Cold Eye Earth: both in the power sector, and in transportation, wind, solar, batteries, and EV are all superior technologies to the incumbent technologies that run on fossil fuel combustion. But not superior enough to easily render incumbent tech worthless. Value retention is 1. real, 2. a big deal, and 3. is very much in the way. This problem needs far more acknowledgment.

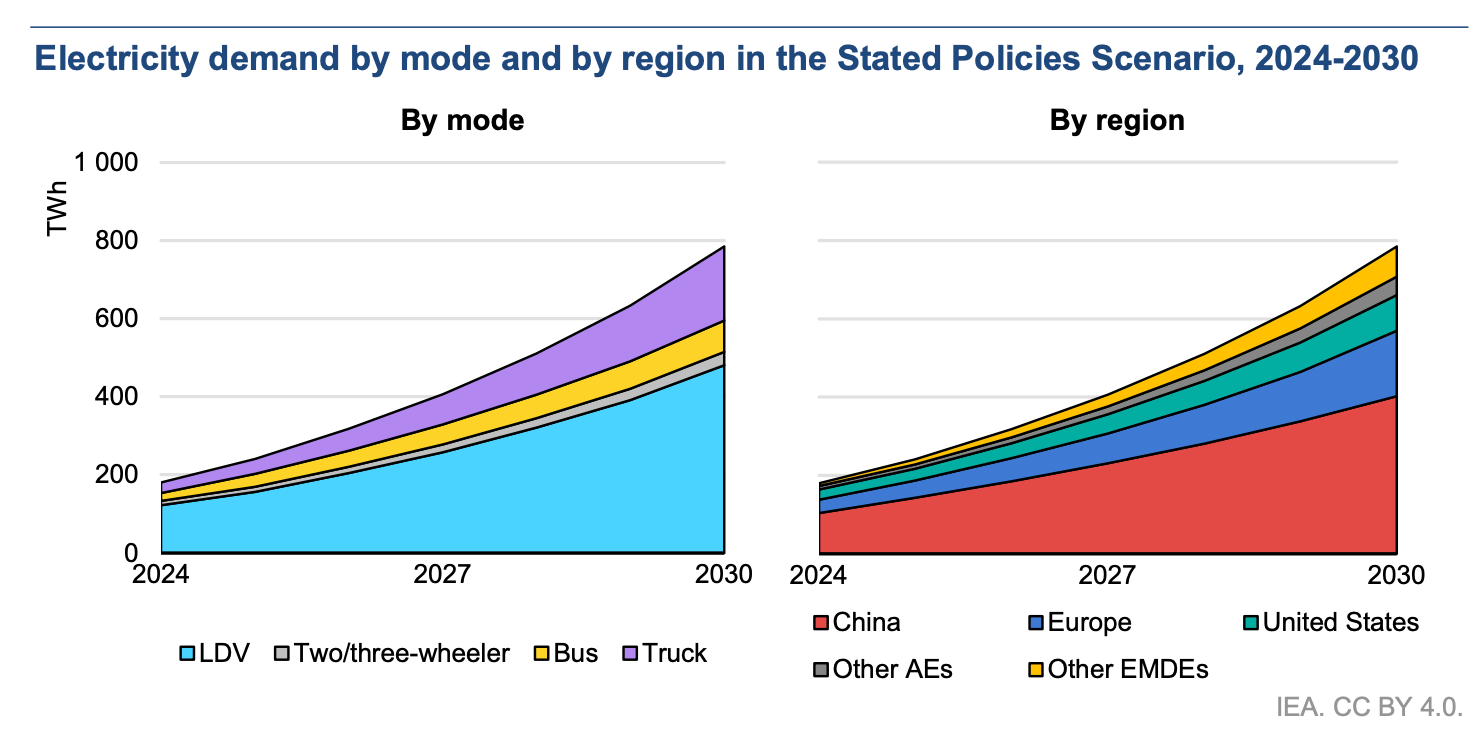

Finally, another way of looking at the slow pace of adoption globally is to note the IEA’s forecast for total electricity demand growth from EV by 2030. While it’s true that an EV uses at least 65% less energy to go one mile than an ICE vehicle, the IEA’s growth forecast is still exceptionally mild, rising only 600 TWh from last year through the end of the decade (200 TWh - 800 TWh). Scale and Proportion check: The world used over 31,000 TWh in total last year; and using a 5 year trailing CAGR is projected to reach nearly 40,000 TWh by 2030. This projection therefore from the IEA for EV driven power growth is so mild, it’s more akin to projections of data center growth, currently at roughly 500 TWh during the same period.

The reconciliation bill just passed by the US House of Representatives appears to be very much in the Reverse Robinhood tradition. As such, the bill would place not upward but downward pressure on the US economy, as capital is channeled towards upper income entities, while the middle class would see, in the aggregate, a contraction in funding for everything from health care to student loans. And that’s in addition to the new 10% tariff layer on all imports, which are leading to higher consumer prices.

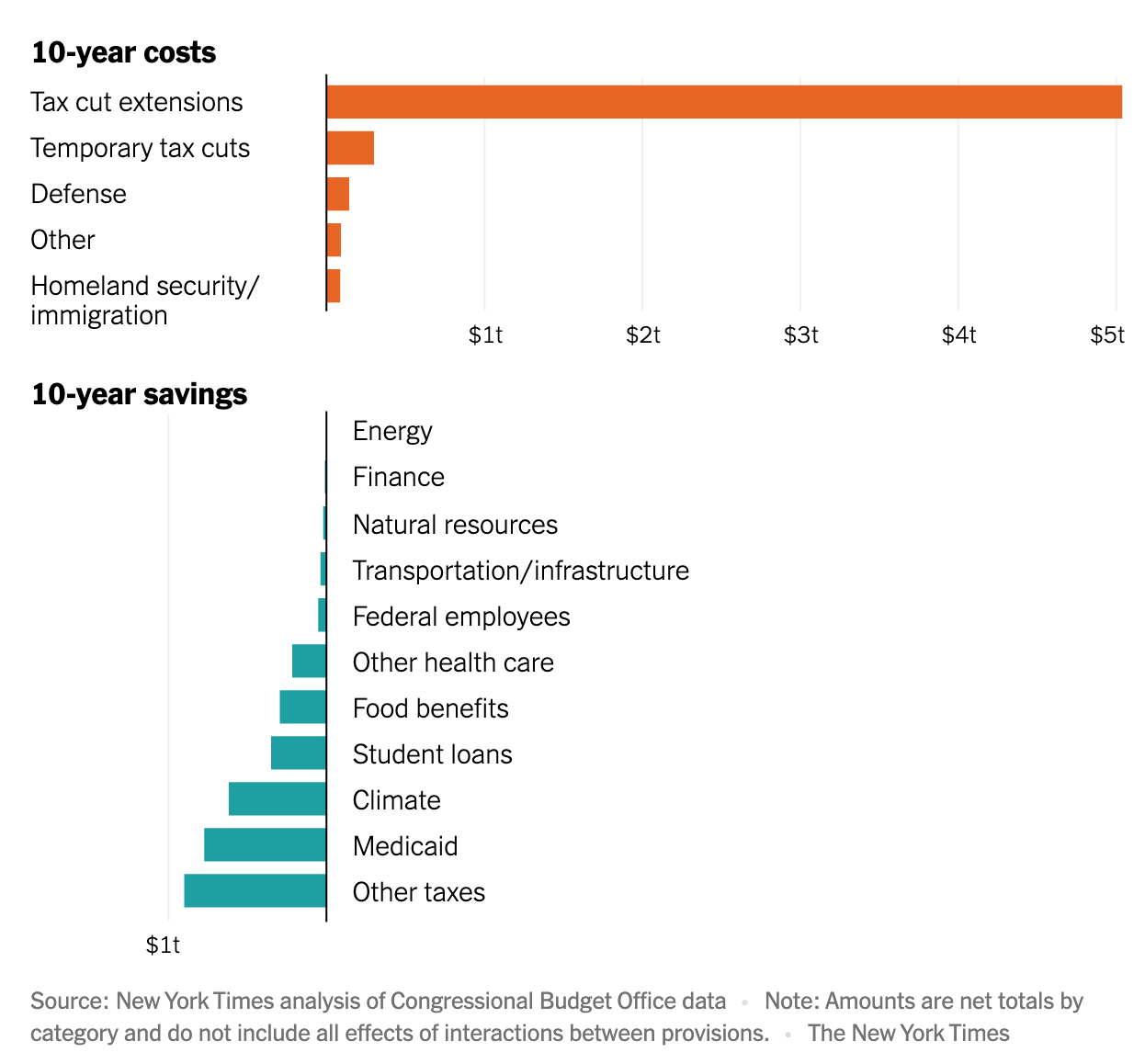

The New York Times published a very good and readable detail of the spending bill’s myriad components. But one doesn’t need to read through the entirely of the laundry list to grok the bottom line as the newspaper also provided a summary chart which pretty much tells the tale:

Notice that the bulk of the bill simply extends the existing tax cut regime that Trump crafted in 2017—which favored corporations and high income earners, of course—and that this extension constitutes the corpus of the price tag. So, there is no incremental stimulus to anyone or the economy from that extension. Those temporary tax cuts you see in the second bar are things like no taxes on tips, and a boost to senior citizens through a larger standard deduction. But these are so very minor. The big swing comes in the “savings” chart, and that’s where the real action takes place here. Notice the four items starting with Food Benefits, and going through Medicaid. Those cuts are all contractionary.

Imagine for example a 40 year old man living in North Carolina who in the past few years obtained work in battery manufacturing as a result of the IRA, and who has a first child about to enter college. Because the cuts to the IRA are so dramatic, he is now at risk of losing his job. Meanwhile, the federal government is about to stop providing subsidized student loans (loans that do not accrue interest) to undergraduates. If the father in this scenario does lose his job, he will have the option to get health care coverage through the marketplace established by “Obamacare” but here too he will run into a set of new hurdles that make qualifying slightly harder, and costs higher.

To give you some sense of how the bill is being sold, the White House Council of Economic Advisors, led by Stephen Miran, laid out a set of spectacular claims recently on Twitter (X) and reactions from economists was almost uniformly negative.

Just to say, your editor has watched the health care debate in this country for nearly 40 years and it’s been clear every step of the way that the US historically devoted way, way too much spending on healthcare as a percentage of GDP. The US has been a bizarre outlier in this regard, compared to the rest of the developed world. Accordingly, the introduction of Obamacare was in every respect a form of progress, as it pointed the way out of the country’s extremely inefficient approach to healthcare. Needless to say, this concept still travels well above the ability of people to understand how increasing participation and government subsidies would lower aggregate costs, but it’s a classic case of a system moving from a dysfunctional state (the high cost to the system of the uninsured) to a smoother running condition. The House bill begins to chip away at those systemic savings.

Matt Klein at The Overshoot goes so far as to call this an austerity budget, and he gathers up a bunch of related facts about the spending plan to support his own view, coming to the same conclusion. (placeholder link is here, to the excerpt below).

The U.S. Austerity Budget

The U.S. Congress is moving forward with a budget plan that would not lower most Americans’ taxes relative to current rates5, but that would meaningfully cut spending on health benefits for the poor (Medicaid), food aid for the poor (SNAP), and subsidies for green energy. The proposed budget is also set to sharply increase the punitive tax imposed on America’s premier research universities in 2017. Combined with the tariffs, which are taxes imposed on Americans, the net effect should be contractionary relative to the current fiscal stance, although the timing of specific provisions may obscure the aggregate impact.

Confusingly, much of the coverage about the proposed budget focuses on how much the federal deficit will rise over the next ten years compared to “current law” and what that will do to the stock of federal debt outstanding. Most estimates of the total “cost” of the proposed legislation start from the absurd baseline that individual and business taxes would have been allowed to rise sharply in 2026 as the 2017 Tax Cuts and Jobs Act (TCJA) expired. That was never particularly likely, especially once the party that explicitly campaigned on extending the TCJA tax regime won Congressional majorities and the presidency.

Notice Klein’s separate and astute observation that the headline news about a soaring deficit derives most of its energy from a classic baseline effect that measures the difference between the proposed extension, and the revenue the government would have taken in had the 2017 tax cuts been allowed to expire. Well, as Matt points out, that was never going to happen. The cuts were not attacked by the Democrats during the Biden administration, and the economy has gotten used to them—no surprise. That’s why the better angle from which to see this reconciliation bill is to toss out that huge, orange histogram bar in the New York Times graphic that reflects the size of the extension—because that represent no change—while concentrating instead on the actual changes to come. When you do, Klein’s austerity framing is quite justified.

Nota bene: The House bill will face some opposition by Senate Republicans, from debt hawks like Rand Paul (KY) and Ron Johnson (WI), and among Senators favorable to the IRA like Collins (ME), Murkowski (AK), and possibly Tillis (NC). Accordingly, we cannot adequately address the full impact of the bill until those changes are incorporated. It’s not the generic extension of the 2017 tax cuts that at risk of change here. Rather, it’s all those other bits that will likely be modified. How much, we shall see.

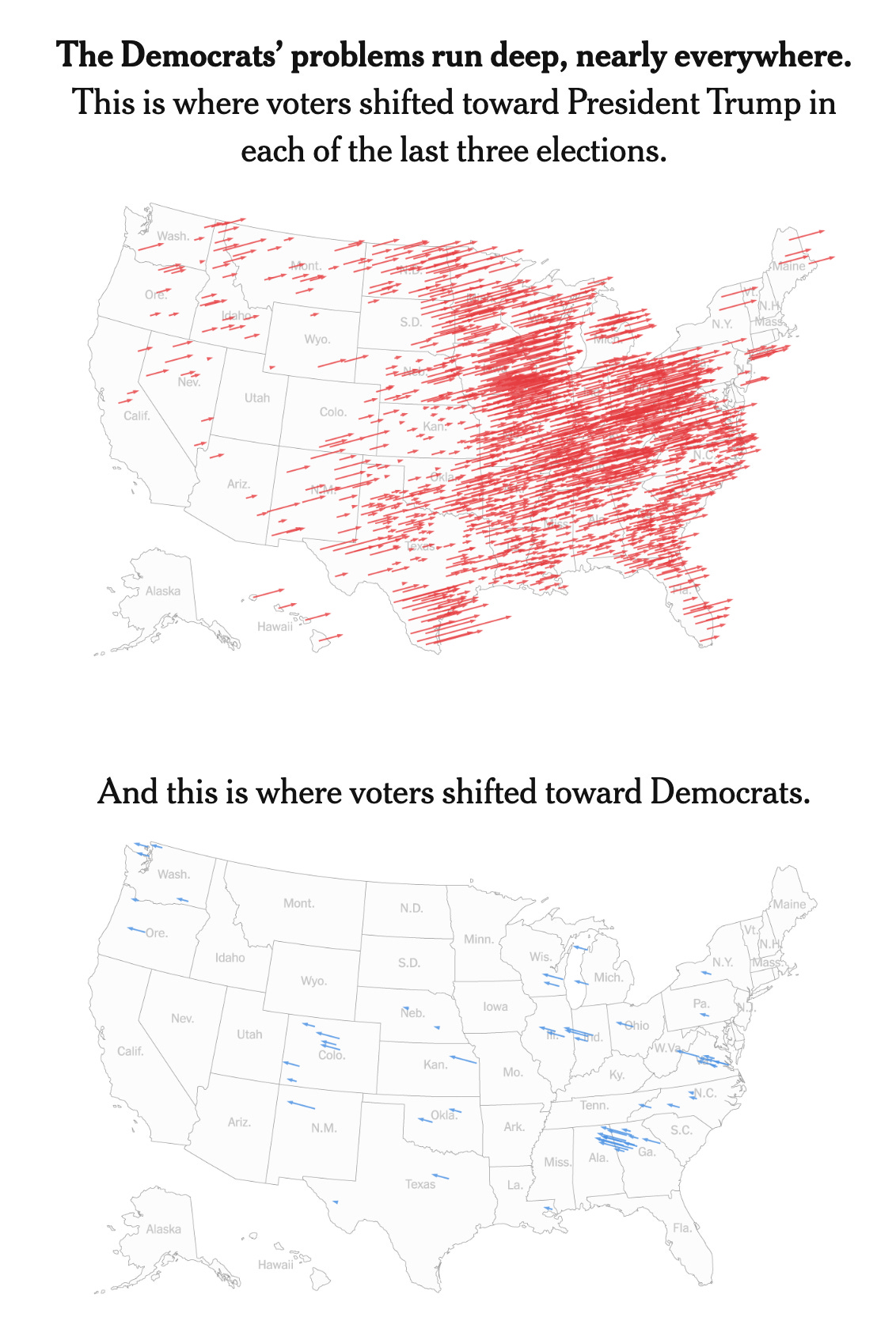

Future, democratic presidential nominees will likely need to spend more time in red states and especially more time thinking about economic solutions that work for red state voters. We have new analysis this week of the aggregate voter shifts over the last three elections, and the results couldn’t be more sobering for the Democratic Party.

On the level of specifics, the Democrats are gaining ground only among the wealthy and the educated. The Republicans meanwhile continue to gather up the poor, the working class, and the less educated. (Given the structure of the Republican budget bill just discussed, which disproportionately disadvantages those who voted Trump, this makes some sort of clash inevitable, to be sure). And obviously one factor here is that the Republicans are absolutely winning the information-space through radio, podcasts, and social media. The dominance is so effective that, collectively, it’s possible to sell the current budget bill as an attractive tax cut package that will create jobs, when that is clearly not the case.

From the NYT article:

By contrast, Democrats have steadily expanded their vote share in those three elections in only 57 of the nation’s 3,100-plus counties.

These counties, which we are calling “triple-trending,” offer a unique and invaluable window into how America has realigned — and still is realigning — in the Trump era. They vividly show, in red and blue, the stark changes in the political coalitions of the two parties.

The scale of Mr. Trump’s expanding support is striking. While roughly 8.1 million Americans of voting age live in triple-trending Democratic counties, about 42.7 million live in Republican ones.

Even more ominous for the Democrats are the demographic and economic characteristics of these counties: The party’s sparse areas of growth are concentrated almost exclusively in America’s wealthiest and most educated pockets.

Yet Mr. Trump has steadily gained steam across a broad swath of the nation, with swelling support not just in white working-class communities but also in counties with sizable Black and Hispanic populations.

As we head into the next election cycle starting next year, Democrats seeking national office may conclude that they need to both sell and explain their policies in detail, and to test the waters of such an approach it may be prudent for candidates to spend more time in Ohio, Pennsylvania, and Wisconsin to make sure they are connecting and closing the sale of their ideas. Let’s make this more explicit: if Democrats believe they have a better set of policy solutions for the poor, the less educated, and the working class, then they need to bring those solutions to stages in the Midwest—and in particular, they need to stop writing off red states. Haven’t won Ohio in the past several elections? Too bad. Doesn’t relieve you of the need to go to Ohio, and make your case.

The time has come to take the under on the US ability to rapidly expand its supply of electricity. While the President pursues photo-ops and White House executive order signing ceremonies—like the one from Friday 23 May, focused on nuclear energy—his administration has damaged the myriad pathways inside of the federal government that actually make achieving such goals possible. We must remember the profound incompetence of this administration when discussing such outcomes because at times it can literally test one’s sanity to accept how dumb and uninformed everyone is around the President. In other words, you must be able to contemplate that it won’t be until sometime later this year, or early next, that the administration discovers that they crippled their own efforts this year, for many goals they wanted to purse next year.

Meanwhile, US total electricity generation is seeing its first notable bump to a higher path, as the US is very much swept up in the global supertrend towards electrification. The chart below shows both total generation and the split between combined wind and solar, and all other sources. Can it continue?

Most observers have assumed the US will be able to add marginal power supply each year as load (demand) increases due to data center growth, and electrification. Cold Eye Earth is not so sure. The liklihood that this administration understands, for example, the necessity for transmission, with all its complexity, is highly doubtful. And let’s consider how much difficulty was endured even by the Biden administration in its efforts to surmount various technical and regulatory hurdles for the sake of their own legislation.

Most global forecasters have been assuming the bulk of data center growth (and therefore power supply growth) would occur in the US the next 3-5 years. But notice that while a company like OpenAI is indeed building a large data center in Texas, where did the recent Big Tent meeting occur, with most of the big AI players? In Dubai, where the hurdles to building new power capacity are few if non-existent. Do all the big AI players need to have their cloud fleets sited in the US? No, they don’t. Remember, we are dealing with an administration that still doesn’t understand that wind and solar are crucial to marginal growth of power supply, and are ready to hurt those technologies to prove out their ignorance.

—Gregor Macdonald