Emissions Rising

25 November 2024

Peak emissions cannot be forecasted by tracking the growth of clean energy. For a number of years now, however, that appears to have been the game many were playing. Worse, some have attempted to call peak emissions in real time, and while that can’t be done either, it must be said that doing so is quite foolish. The challenging variable in all these attempts of course is not renewables growth, or fossil fuel growth, but economic growth itself. As a result, we will only know when emissions have peaked in retrospect, when their downward trend is sustained. Everything else is just throwing darts, and using hope as a strategy.

Incentives for making peak emissions forecasts are many. Think-tanks want to demonstrate they have a competitive edge with the data, the audience wants to hear good news, and journalists are understandably eager to report that progress is being made. Indeed, one way to describe our current moment is that the storyline of amazing growth in renewables has overshot actual emissions progress on the ground. This divergence can be explained pretty easily, at least on one level: peak emissions forecasters get renewables growth right, but get economic growth—and the demand it represents—wrong. If you’re a think-tank that has forecasted for a couple years now that global power sector emissions have peaked, or that China emissions have peaked, or that the US is still on track to hit emissions targets by 2030, some advice: stop doing that. Don’t put out those forecasts anymore. The repetition of failed attempts (revealing the lack of a sound method) has become embarrassing. Also, if you’re a publication covering this area, try being less credulous.

Some well needed sobriety on this subject was delivered last week, however, by Umair Irfan, writing for Vox, with a very on-point headline: We were supposed to hit peak emissions. Why won’t they stop rising? The article keys off the latest assessment from the University of Exeter, and its Global Carbon Project science team, showing that emissions rose again this year, this time by 0.8%. This is a touch better than 2023 growth, which saw emissions rise by roughly 1.1%. And we are becoming more successful, it must be said, at lowering the growth rate.

But peak emissions forecasting has another problem to contend with: reaching the peak offers no promise or even likelihood of declines. That declines follow peak is a human intuition, not how the reality of fossil fuel consumption actually plays out. More often than not, consumption plateaus, often for years, and we should expect the same when emissions finally stop growing.

Energy transition may have a modeling problem, when it comes to the displacement of legacy energy sources. Consider the following statement:

We'll build so much wind, solar, and storage that we'll cut into fossil fuel in global power, sending emissions into decline.

This has been a reasonable expectation for over a decade, but the thesis has run into a hurdle. The statement needs to be adjusted.

We'll build so much wind, solar, and storage that we'll start covering all marginal growth in global power. But then we’ll settle into a pattern where legacy fossil-fuel power generation takes an overly long time to retire.

How did we get from the first statement to the second? One explanation may seem like a paradox, though it’s quite straightforward and not exactly a surprise: we’ve been very busy retiring the oldest fossil fuel assets first, which over time has made the remaining assets far younger as a group. And that may be why a standoff has developed between the new, and the old. Over the past 15 years, the US for example has closed down a bunch of ancient dams in hydropower, older natural gas plants, and very old coal plants. These types of older plants were barely economic, or worse, entirely uneconomic. Only a few incentives were required to tip them over the line into closure.

The result is that the US power generation fleet is now considerably younger, on average, than a decade ago and today stands at a capacity-weighted average of 28 years. Needless to say, Cold Eye Earth has hardly been alone in observing that the US rapidly retired old coal in the past 10-15 years and replaced at least half of the lost capacity with fresh, young, natural gas capacity. Unsurprisingly, retirements are now slowing.

When we look at the history of how wind and solar have been deployed in the US, rapidly taking up market share, we see a pattern that has formed over the past five years, starting in 2020. Essentially, the US grows its new wind and solar generation each year right up to the point where it would start to cut into the fossil fuel underlayer. And then, stops.

Generation in the US powermix ex-wind+solar has been effectively held right around the 3600 TWh level for five years now. Even more revealing is that from 2010 to 2020, new wind and solar initially started to work its way through the stock of other energy sources. That trend was enabled however by the very old age of many US powerplants, coal especially, but also old natural gas and some old hydro.

Could something like this be unfolding on the global level too? Indeed it could. On the global level, we still have the simpler problem that total annual demand growth for electricity continues to outpace the growth of renewables. Red flags should go up every time you see a think-tank claim that global power emissions just peaked. As usual, these think-tanks engage in a kind of moribund accounting of new renewable capacity, but don’t have a method to forecast GDP or industrial growth with any accuracy. The result: a “maybe next year” doom-loop of Wrong.

Just to say, it certainly was not anyone’s goal, and Cold Eye Earth is unaware of any forecast, that renewables would run into a temporarily insurmountable hard wall of legacy capacity. But that’s where we are. And the problem is clearly not fossil fuel legacy capacity per se, because it’s not actually hard to retire the very old units. Rather, it’s the period after we’ve aggressively retired the old units that presents the challenge.

If you want new energy technology, renewables, and electric vehicles to start meaningfully cutting into the fossil fuel base, then you will need to come up with a plan to retire or destroy young, economically viable power plants, and petrol-based vehicles. Otherwise, you will have to wait for the ploddingly slow nature of fleet-turnover to take its course.

Markets will be pleased initially at the nomination of Scott Bessent to head up the US Treasury Department. He’s had a long career in the hedge fund industry, and that’s a signal to the global finance community that Bessent is neither an ideologue, nor is he inexperienced. But the test will come when Bessent is asked to preside over policy initiatives with which he’s likely to disagree. One of the jobs of Treasury secretary, along with the Federal Reserve, is to handle recessions, crises, and other risks that pose threats to the system. In other words, Treasury secretaries are not inclined to knowingly undertake actions that would be bad for markets, and frankly that includes the job market too, and the wider economy.

As many have pointed out, and quite correctly so, the incoming administration already has a built-in tension within its myriad economic policy plans because tariffs are not friendly to interest rates, mass deportation is not friendly to the economy, and debt reduction is not friendly to growth. Put another way, one of the reasons markets will initially like Bessent is that his nomination signals that while many crazy voices may be at the table during the next administration, at Treasury at least, a voice of sanity will be in control.

However, we also know that the hedge fund industry has a record of producing overly confident characters who are certain they know more about macroeconomics than they actually do. Indeed, since the great recession, the collective, American hedge fund community has been absolutely obsessed with US debt levels. The tedious flogging of this issue by every hedge fund guest that comes on financial TV has frankly grown tiresome. The industry also tends to attract highly intelligent, highly educated people who love to reduce complex problems to shorthand, with a puff of smoke as a flourish. We may have gotten a taste of that already with Bessent, as we learn that he’s been offering easy, shorthand metrics to the incoming president. From the New York Times:

Last spring, when many business leaders were hesitant to back Mr. Trump publicly as his legal troubles mounted, Mr. Bessent took a different view. He saw Mr. Trump as a “stock that goes up on bad news,” as he explained it to the political analyst Mark Halperin last month, because every apparent setback appeared to strengthen his candidacy.

Concerned about the exploding national debt and the need to make changes to the international trading system, Mr. Bessent set up a meeting with Mr. Trump and started exchanging economic policy ideas.

In recent months, Mr. Bessent has pitched a “3-3-3” plan that would aim for 3 percent economic growth, reduce the budget deficit to 3 percent of gross domestic product and increase domestic oil production by 3 million barrels per day. He also came up with an idea that would allow the president to essentially sideline the chair of the Federal Reserve, although he has backed down from that proposal in the face of opposition.

Let’s talk about that 3-3-3 plan. First, it is not easy to sustain 3% GDP if you are at the same time engaged in deficit reduction. Government spending is someone else’s income, regardless of your views on government spending. If you believe that reducing government spending will somehow free up a larger piece of territory for private, free-enterprise you are welcome to have that view too—but markets in the short to near term are not likely to see it that way, nor is there anything magic or automatic about reductions in government spending leading to a sudden starburst of fresh capitalist activity.

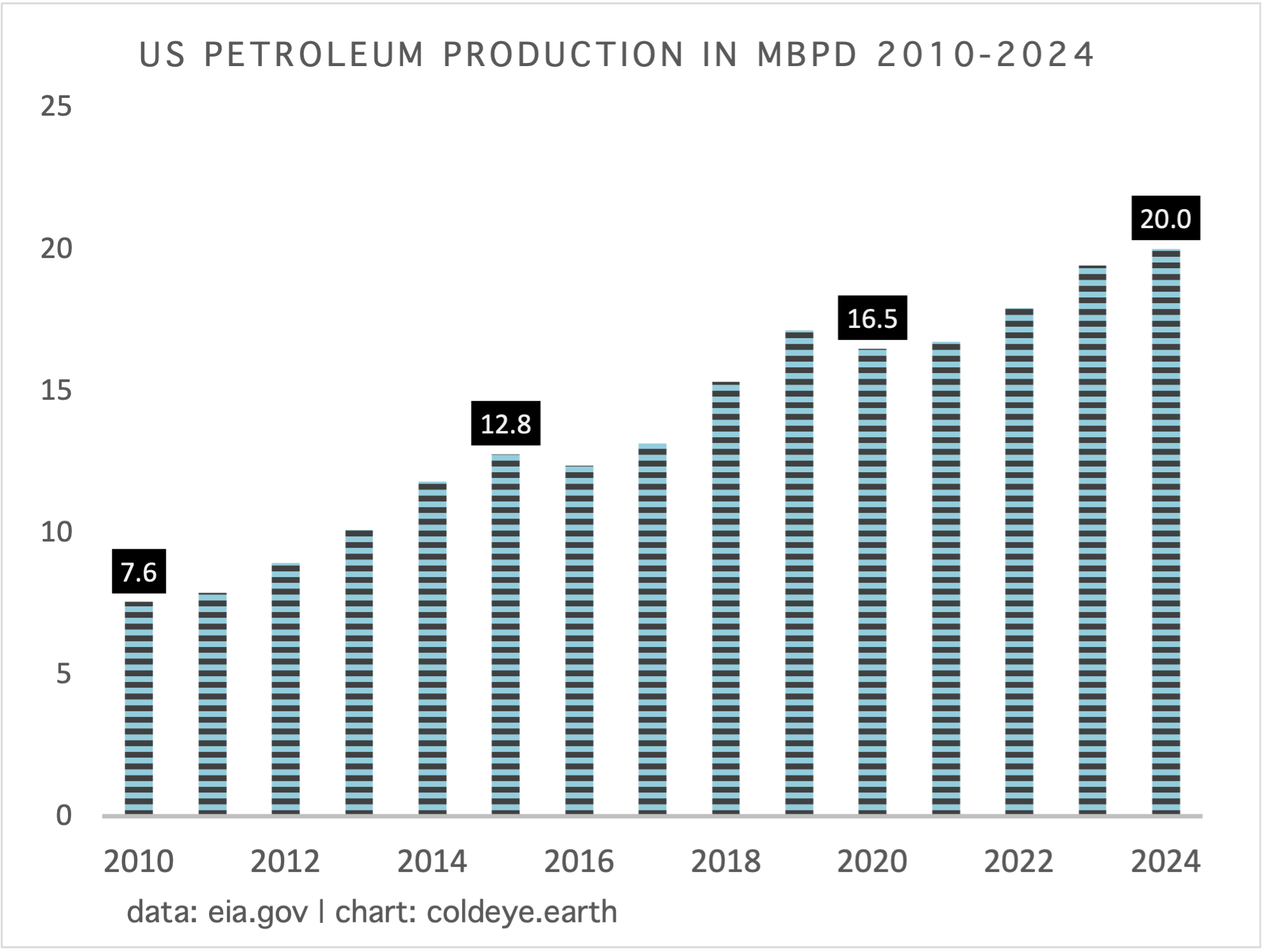

The curious item on this list is of course the desire to take US oil production to even higher levels. Cold Eye Earth has already weighed in on the incoherence of lifting US supply further, because surely it will be met with an even bigger increase in OPEC spare capacity, as that group dials back production further. Needless to say, this would all weigh heavily on price and, as suggested in the last issue, the administration could bend itself into pretzel-like shapes—perhaps even going so far as to buy some of this surplus oil to fill the reserve. The salient point however is that Bessent may be far more rational than the average nominee to this administration’s cabinet. But, it’s relative.

Just to remind, here is a chart of US petroleum production:

Combined wind and solar have once again grown strongly in 2024, but they won’t be able to catch global, marginal growth in power. Cold Eye Earth estimates that generation from wind and solar globally will advance from 3967 TWh in 2023 to 4622 TWh this year, a very impressive gain of 655 TWh of new, clean, renewable power. However, given the expectation that total global power demand rises by an above-average 4% this year (IEA), this means demand will rise from 29925 TWh to 31122 TWh, or a rise of 1197 TWh. Perhaps when the data is all settled, generation from wind and solar comes in a touch higher? Or perhaps total growth comes in a touch lower? Even if both of those outcomes do unfold, you can see we are still not even covering marginal growth of power, with wind and solar.

Let’s return now to that just released global emissions report from the University of Exeter, because it’s instructive to see where last year’s gains came from. Here’s a good one: according to the IEA, global oil consumption growth slowed this year, and will only rise about 0.8% and the science team at the Global Carbon Project estimates that oil emissions this year rose by 0.9%. Here’s another: as we know, coal both in the US and around the world is being replaced by a combination of wind+solar, plus natural gas. Well, this year it’s estimated that emissions from natural gas rose by 2.4% vs coal’s increase of just 0.2%. Once again, we have diluted the emissions in coal yet another new round of natural gas adoption.

What particularly concerns Cold Eye Earth is that the next four years could see a stalling out of emissions gains in the US, largely through either new policy, or, curbs on old policy. To put this in clear terms, the US no longer has a significant coal problem and no one can rescue coal from its fate. Moreover, we are going to continue deploying wind and solar in the US, which is good news. However, there is risk that natural gas use could rise even more strongly than it has already, under a new administration. But the main concern is oil. The US hasn’t added to global oil demand in many years. But the US hasn’t done much to reduce its demand either. Without the US reducing oil demand, without the US placing an actual drag on demand growth (the way the EU places a drag, for example), the risk is that global total demand has a chance to rise. It should be clear that, despite oil’s reduced share of global energy demand from all sources, its oscillation, up or down, is very controlling of emissions. And the prospect that the US “gets its oil consumption under better control” over the next few years is dim, to put it mildly.

—Gregor Macdonald