Globalization is Fine

Monday 5 September 2022

Batts, chips, and panel production are all coming to the United States as friendly manufacturing policies start to gain traction. Japan’s Honda Motor Company and South Korea’s LG Energy Solutions are just the latest among domestic and international groups, or partnerships, announcing inward investment plans. Honda and LG will house a new battery factory on existing Honda properties in the state of Ohio. This follows similar plans recently unveiled by Hyundai, Panasonic, and others to conform to sourcing guidelines in the new US climate legislation. To enjoy tax incentives, US EV will need to have more substantial portions of their drivetrain built domestically.

A new approach to US industrial policy has been brewing for years, one that responds to legitimate concerns about US dependency on global supply chains. Now come the results. The flurry of battery plans is tracking alongside separate initiatives to kickstart US semiconductor and solar output. Intel, Micron and First Solar will also be expanding in the US. Indeed, some analysts have noted for years that polysilicon manufacturing costs are mostly a function of electricity prices. And now that power prices globally have been converging, US electricity rates are pretty competitive.

More broadly, it’s intriguing to consider the new buzzword, deglobalization, in the context of this re-ordering of supply chains. One wonders that the term—which now peppers the writings of analysts, online and TV commentary, and corporate conference calls—is either hollow, or perhaps just plainly US centric. Globalization is a phenomenon thousands of years old. Humans are globalists: travelers, traders, colonists. If you define interdependency exclusively through a US lens however, a more attractive home terrain for global manufacturing could indeed appear, at first glance, like a pullback from the post-war offshoring supertrend. But a flowering of new manufacturing capacity in the US, spearheaded by multinationals, is hardly contrary to globalization. Rearranging the volume does not change the mass. If the global economy sources more of its batts, chips, and panels from the US, that is not a reduction of globalization, but a continuation.

The cyclical bull market in oil, sustained by an ongoing geopolitical event, has revived faith in fossil fuels and doubts about energy transition. The temptation to convert short term developments into long term trends is universal, and now that fossil fuel prices have been so firm, many are backtracking on views held just 2-3 years ago. While the oil industry has certainly curtailed itself—newly reluctant to reach for the stars or plan for much demand growth—that has not changed views much about the prospects for energy transition. In a speech last week, the CEO of a Colorado oil and gas services firm asserted flatly, “The energy transition is not happening. The drumbeat is crazy!” That is very amusing.

Perhaps it would be timely, therefore, to check in on Colorado’s energy transition. The state is known for having abundant wind and solar resources. (Denver has one of the highest levels of annual sunshine hours of any city in the US, and ranks alongside Los Angeles). Moreover, like Massachusetts, Oregon, California, and Washington, Colorado has an aggressive EV tax incentive program—though, like the rest of the country ex-California, adoption is coming up from a low base.

At the moment, there are currently 10.9 EV on the road in Colorado for every 1000 people, according to the state’s new EV dashboard. That may not sound like much, even though state population is modest at 5.9 million. But the leading edge EV state, California, has 21.1 on-road EV for every 1000 people, which is really a world class level of penetration. So Colorado is well on its way. What will those EV run on, in Colorado? Increasingly, the state’s power mix is migrating (yes, transitioning!) to wind and solar. Indeed, the state’s power mix is right up there with California and other high renewable domains like the UK, and Europe more generally.

Cleaned up cars. Cleaned up grids. Both working together to further reduce emissions. As readers know, when an EV travels in a region with high renewable share, the positive systemic impact is not just on emissions, but on improved well-to-wheel efficiency.

Argonne National Lab will soon update its GREET model, which provides impressively comprehensive data on EV efficiency. Argonne models assess energy inputs for all types of vehicles, and lay out the results in comprehensive data sheets. Their advanced contribution, however, comes in the systemic analysis of the energy required to propel either an EV or ICE vehicle one mile, also known as a well-to-wheel measurement. Through this wider boundary approach, they attempt to capture not just the energy needed to supply the vehicle from the pump, but the entire supply chain from the oil wellhead or the battery production sequence, for EV.

Let’s begin however with the narrower boundary measurement: pump-to-wheel, which measures only the energy from gas pump or charging station to the vehicle. According to Argonne’s 2021 update, here is the comparison of the energy needed from a pump, or charging station, to drive an average ICE vehicle and an average EV one mile, in the United States.

4,289 btu/mile: ICE (gasoline) car.

1,283 btu/mile: EV car.

That 70% difference between the legacy technology and the new may seem like an inconvenient truth, but for society and the economy, it’s not inconvenient at all. In the history of energy transitions, no matter how hard or disruptive it was to migrate from the incumbent technology, the cost savings worked away at the problem, like ocean waves forever pounding their way through a barrier.

As readers are aware however, one of the more common retorts against EV goes something like this:

Oh sure. An EV requires 70% less energy than an ICE car to travel any distance. Fine. Now add in all those wider costs to make the battery, and then we’ll see how your precious EV looks then, OK?

Challenge accepted. In the wider boundary analysis—known as well-to-wheel analysis—the whole-system energy needed to propel that EV does rise substantially. But wait. The ICE vehicle also sees a major increase:

5,461 btu/mile: ICE (gasoline) car.

2,606 btu/mile: EV car.

Fair is fair. The well-to-wheel assessment causes the EV’s total system energy requirements to more than double, from 1,283 to 2,606 btu/mile. No argument. The powerplant on an EV is material-intensive, far more so than a simple gas tank. And electricity does degrade, over transmission lines. But well-to-wheel also moved the ICE vehicle’s requirements up by 27%, from 4,289 to 5,461 btu/mile. That difference in the ICE analysis is a pretty good proxy for the energy costs needed to bring oil up from the depths, and to ship it, refine it, and deliver it to a petrol station.

But there’s one more assessment we need to consider. What if we compare well-to-wheel ICE not with your average EV running in a typical US powergrid mix that’s heavy on natural gas and coal, but your average EV in a state where renewable penetration is very high? In California, when you charge your EV, you are getting power that’s at least 25% composed of wind and solar. Not true in most other states, like Kentucky, for example. Here is well-to-wheel for an EV that lives in San Diego:

2,241 btu/mile: EV car in California.

Remember, an EV driven one mile in Louisville, Kentucky is exactly as efficient as the same model EV in San Diego, at the level of the motor—the definition of pump-to-wheel analysis. But. When you take in the whole system view, well-to-wheel analysis, the EV charging and driving every week in San Diego is 59% more efficient than the same EV charging and driving in Louisville.

Conclusion: EV require electricity, and an expensive, material-intensive battery. And power erodes over transmission lines. However, from an all-in energy cost point of view, an EV driving and charging in a high renewables domain, like California, beats the ICE vehicle handily at a nearly 60% energy savings. And as powergrids get even cleaner, taking into account not just wind and solar but nuclear and hydropower, the efficiency gains will keep pressing forward. While upfront investment costs for the energy transition are high, the lifecycle returns are juicy because the savings accrue over time. Energy transition is ultimately deflationary.

Crises and panics produce new era thinking, and the grandiose claims emerging in the post-pandemic period are no different. There are good reasons to be skeptical of this type of capital letter naming exercise for small, nascent trends that nearly always turn out to be short-lived. The New Normal, popular in the aftermath of the great recession, turned out to be alot like the era interrupted by the Iraq War: low interest rates, technology dominance, and not very good wage growth. This time around, there are bold claims and forecasts that 1. labor has entered a new regime of stronger pricing power, 2. inflation is here to stay and the deflationary era has finally ended, 3. the multi-decade decline in interest rates is over, and 4. fossil fuels will take their revenge for years to come. The Gregor Letter is not convinced of any of these, for they all arrive in a kind of naive package that bears no markings of a 100 year pandemic.

But there is one trend that was nascent before the pandemic that really does seem to have taken hold: work from home. Turns out, there’s an entire project at Stanford dedicated to tracking this phenomenon, Work From Home Research. According to Nick Bloom, one of the project’s team members and a professor of economics at Stanford, work from home (WFH) has fallen from a spike high as expected, but is stabilizing at a new, elevated level. The implications for commercial real estate, downtown central business district activity, and transportation demand around commuting are profound if this trend is sustained.

California is once again refreshing its brand as a leading-edge state, with a flood of new legislation impacting car ownership, energy supply, and urban density. To the surprise of many, California voted to extend the life of the Diablo Canyon nuclear plant, whose closure would have opened a fresh hole in the state’s clean energy mix had it shuttered. Next, after many years of internecine conflict over housing density within the political left, California came down resoundingly in favor of a ban on parking requirements for new housing built near public transit. My public comment:

Think of this as a kind of legacy parking-lot-protection-act, now being flushed down the drain. Going forward, California developers can build housing with no parking at all. Finally, in what is perhaps the most eye-opening action of all, California will finally hit car ownership itself with a disincentive program. From this point forward, lower income residents will qualify for a $1000 tax credit for not owning a car.

The bigger news item to emerge from California this past month was the intent to ban all ICE sales, by 2035. The public is far more attuned to splashy news of this kind, overlooking or even discounting building code changes like the end of mandated parking. Two enduring points need to be made, however. One, California is already on course for very few ICE sales by 2035. EV market share is soaring, now on course to reach 20% sometime later this year, or early next. Second, is that policy goals like this surprisingly do have an impact. We saw this in Britain, with the future banning of diesel cars. So the ICE sales ban—even though it’s far away—will weigh on consumer decision making. In other words, the announcement probably ensures that ICE sales are not disruptively, but rather more smoothly, phased out of the new car market over the next 12 years.

In a classic example of timing, the ICE sales announcement arrived just as California faced late summer heatwaves, placing pressure on the powergrid. This led to the tedious and familiar panic that we won’t have enough electricity to charge EV. The critical reactions were given a boost, too, when the state power authority began to issue requests that EV owners refrain from charging their cars at certain times, during the day. OK. So, a couple of things here. First, brownouts and blackouts have been a feature, not a bug, of the US powergrid since forever. There’s even a list of American films that use such events to ply their drama. Second, California is notorious for these blackouts (now joined by Texas, ahem) with a long history that largely derives from the massive heatwaves that spike air conditioning in late summer. (Feel free to re-watch the story of Enron and California in The Smartest Guys in the Room).

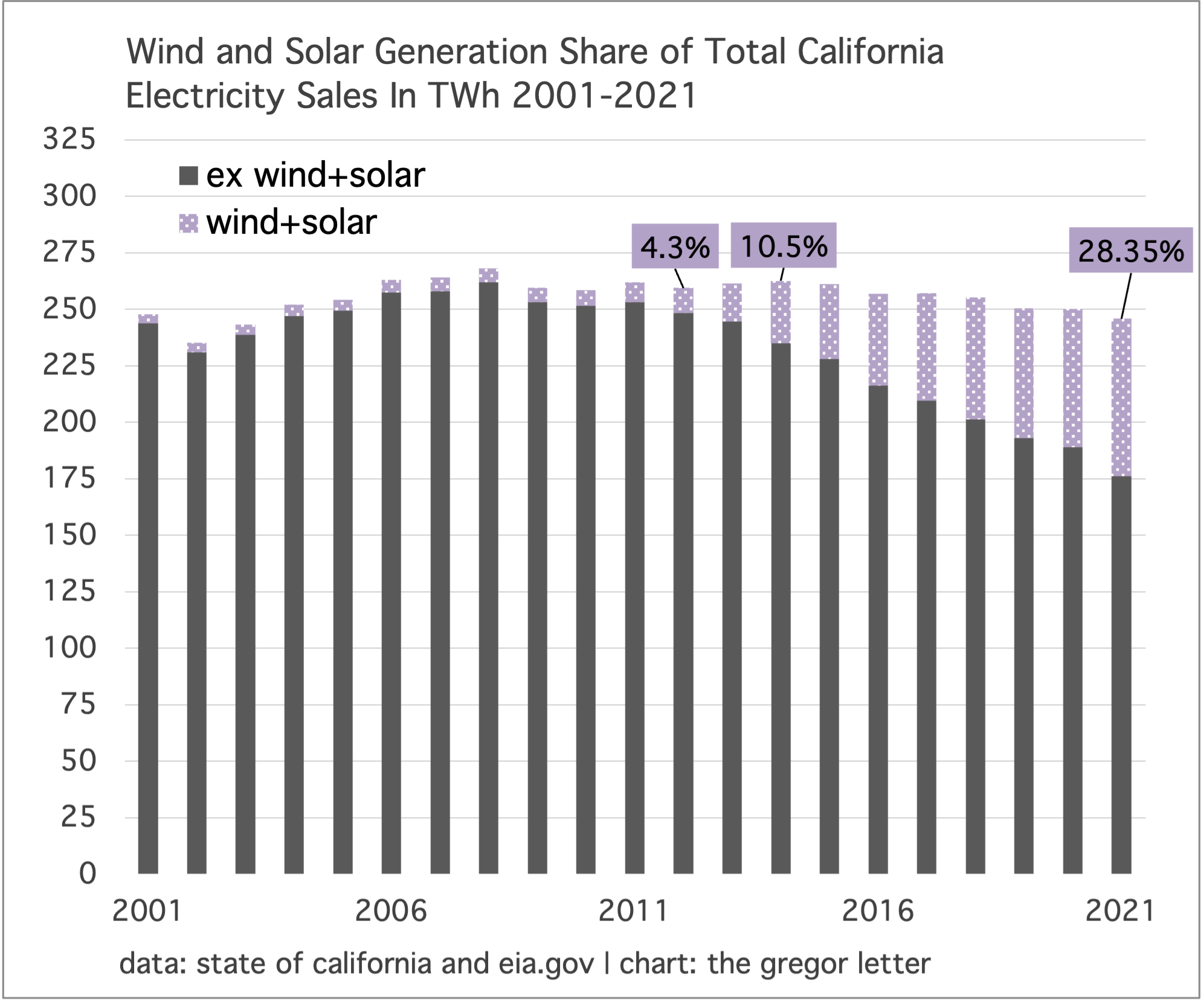

What ails California currently is the sudden decline in hydropower, due to a massive 1000 year drought squatting over the entire US West. The contribution from hydropower collapsed last year to 14,567 GWh, according to the State of California’s Energy Commission. How bad is that? As recently as 2017, total hydro provided 43,304 GWh of electricity, according to historical data also from the energy commission. Meanwhile, solar and wind growth has been a powerful force, adding hugely each year to California’s in-state generation.

Now for the numbers. California put 237,618 new EV on the road last year. Using the standard measure to estimate annual power demand for an American EV of 4000 kWh, this represents nearly 1 new TWh of electricity demand needed (237,618*4000 kWh = 0.9504 TWh). And that’s a cautious demand figure, meaning it’s probably lower, because a portion of those EV are plug-in hybrids. (Data note: The Gregor Letter in all analysis and charts entirely discludes non-plug-in hybrids). But wait. How much newly created electricity last year in California came from wind+solar alone? Yes, just to be clear, how much new electricity supply, created in the state of California, that didn’t exist in the year 2020, came online last year just from wind and solar? Answer: 8.45 TWh. Wind and solar generation grew from 61.263 TWh in 2020 to 69.713 TWh in 2021.

No one is arguing that we won’t need an expansion of power supply to run electric vehicles. We are also going to need some new nuclear. But one must admit that even now, long before 2035, the state of California is positively drowning any marginal new demand from EV with new generation from wind and solar.

—Gregor Macdonald