Hopes for China

Monday 1 September 2025

China’s industrial revolution has largely been defined by the relentless growth of its electricity generation over the past three decades, as the nation transformed itself into the world’s workshop. The recent tendency to declare that China is now becoming an electrostate is a bit odd in this context, because the term is either too slippery to have reliable meaning, or succumbs to newcomer bias: when was China ever not an electrostate? Unlike the U.S., China did not grow its economy on the back of oil. Indeed, it wasn’t until this century that Chinese incomes were large enough and growing sufficiently to start adding domestic consumer demand for petroleum. China had to go through a build up of its cities first, as poor workers poured in from the countryside to take part in the manufacturing boom (Lewis turning point). The U.S. by contrast entered the era of consumer consumption much earlier, immediately after WW II, kicking off the long ascent of its lifestyle and consumer driven demand for gasoline.

In my 2018 series Oil Fall, my chapter on China addressed the divergence between the two countries:

It’s also important to understand that China is a nation that runs primarily on electricity. China is not an oil nation. It’s a power nation, a testament to its strong manufacturing identity. In 2017, China consumed 3132 Mtoe of energy from all sources, but only 608 Mtoe of that total was provided by oil. Oil provides just under 20% of China’s total energy demand. Compare this to the United States, whose total consumption of energy from all sources in 2017 was 2235 Mtoe, of which oil provided 913 Mtoe. The United States, by contrast, is still very much an oil nation, where oil provides nearly 41% of its energy.

Indeed, one of the reasons China has had such an easy time integrating fast growing wind and solar power—without the bottlenecks that appear in other domains—is that unlike the U.S. it has been working on expansion of its powergrid for many decades, primarily led by coal. If we use the starting point of 1990, which most researchers identify as the start of its modern industrial revolution, the data shows that China’s growth of electricity generation grew an astounding 1500%, from 621 TWh in 1990 to 10087 TWh last year. For context, China started 1990 generating less power than Japan (882 TWh) and wound up over 30 years later generating 10X the power of Japan (1016 TWh). This is not the record of a nation just now emerging as an electrostate.

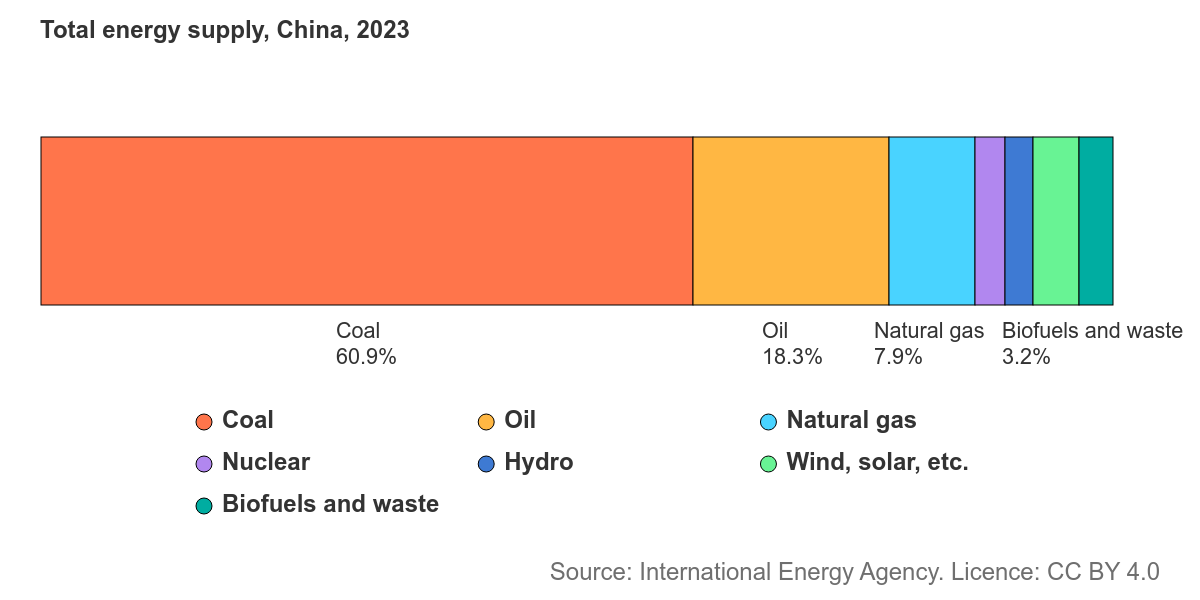

Here is a nice graphic through 2023, showing the composition of China’s total energy use. While there’s certainly alot of metallurgical coal used in China for steelmaking, you can pretty much read the coal category in the chart below from the IEA as a decent proxy for electricity.

Clearly one of the intents behind this new-ish jargon is to paint a contrast between China, which has developed on the back of coal, and the U.S., which not only remains far more car-dependent, but has become a giant of oil production and petroleum refining, or, as they say, a petrostate. As long as we avoid the error of thinking the divergence between the two countries is recent, that’s fair. But even here, there are recent trends that bear watching.

• What do we say about the fact that U.S. oil consumption peaked twenty years ago? And relatedly, that U.S. electricity generation has broken out of a two decade flatline around 4000 TWh and is heading towards 4500 TWh, rapidly. What bars the U.S. from becoming, eventually, an electrostate?

• Although China’s oil demand grew by far less over the past three decades, a 600% increase, its oil demand growth in the last decade has picked up the pace. To be sure, this growth is now running into a wall formed by the titanic adoption of EV cars, buses, and trucks in China: oil growth will eventually be halted. That said, China’s oil demand now sits barely 10% below U.S. levels. So, electrostate is a rather grandiose term for the second largest oil consumer in the world.

Cold Eye Earth has an allergy to geo-political concepts. Terms like petrostate inevitably function as a kind of Christmas tree that can be decorated with every unfalsifiable concept imaginable, and these themes inevitably spill into other suspicions around the dollar, the petrodollar, spheres of influence and so forth. To be honest, events and developments in recent world history seem more often to be breaking out of long-held patterns, than adhering to them. In such a world, the value of labels can crumble quickly.

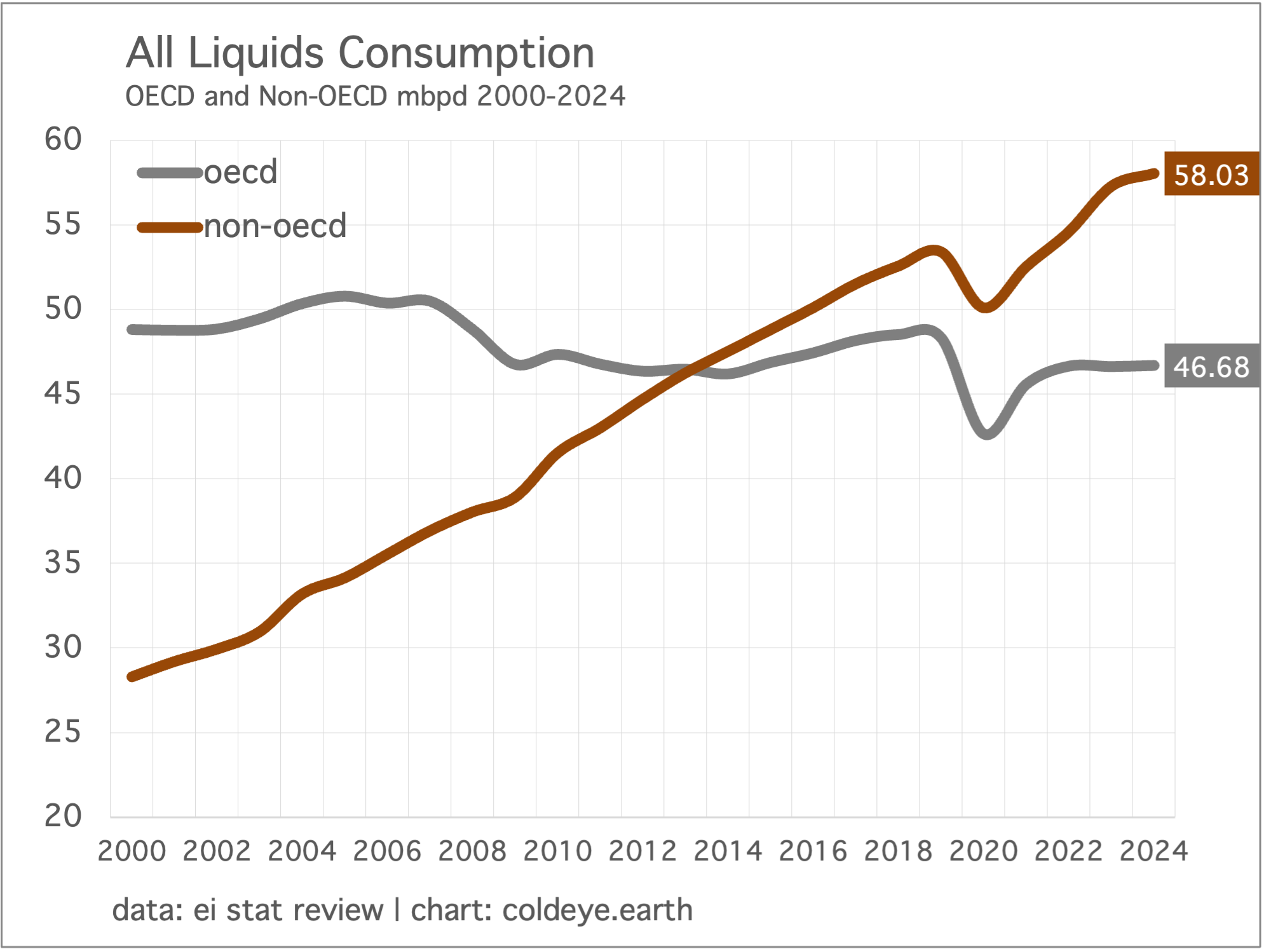

Since 2005 when OECD demand peaked the oil industry has had to entirely rely on the Non-OECD for growth, which of course is mostly driven by China. So we’ve all been quite aware during this time that once China’s oil demand peaks, global oil demand will peak. Based on recent trends, and especially China’s historic growth of electrified transport, we are closer than ever before to a peak—but with a couple of cautionary notes.

First, we must remember that peak does not equal decline. That’s a common intuition, but it just isn’t true. U.S. oil consumption has been on a plateau for twenty years, for example. Second, we must remember there’s a bolus of hard-to-abate industrial processes, mostly having to do with creating heat, that the world has barely begun to decarbonize. In addition to China adopting electricity as its major growth platform, the country has also taken charge of alot of that exact industrial production that relies on oil, natural gas, and coal for which there’s still no clean energy remedy (certainly none that are ready scale, that’s for sure.) This lump of unabated fossil fuel demand is going to press onward, and if China doesn’t perform that work, some other country will.

All this said, China has decidedly avoided the most severe storyline that usually accompanies oil dependence, by veering away from a future dominated entirely by petrol-based transport. Instead, it will be the ongoing industrial demand for oil that is likely to make the country’s overall oil demand resistant to any outright decline, at least for a while. The EI Statistical Review shows that China’s oil demand actually fell last year by 1.7%. You would be wise to read that not as the start of decline, but perhaps a more extended period where China’s oil demand growth levels off, rising and falling by smaller amounts from year to year.

We shouldn’t be overly surprised that global oil demand growth may finally be ready to flatten out. British Petroleum first raised the year 2025 as a likely peak year back in 2019, saying in effect that only a trace amount of growth could be expected after this year. In my Oil Fall series, published serially between 2018 and 2020, I originally tipped the 2020-2022 period as the window in which electrified transport would finally start to bear down on oil demand growth, opening the path to a peak. As always, global oil demand declines are still off the table. Oil in particular is likely to adhere to the additive model of energy transition, in which demand is transformed into a long-standing contest of minor skirmishes with supply. And just to remind, energy transition itself is exceedingly reliant on all the hard-to-abate industrial sectors that produce the infrastructure needed to create and deploy renewable technology.

What is indeed surprising is that oil now has a better near term prospect for conversion to a demand plateau than coal. Because global electricity demand continues to grow far, far, faster than global oil demand, coal has increasingly become the back-up fuel that countries call upon during severe weather (heat and cold) and which serves also a back-up to growth. Here we must remember that China’s coal overcapacity works two ways: yes, it’s confirmation that coal growth in China is slowing, and that part of this slowing is caused by the rise of renewables. However, the surprising spikes we’ve seen in global coal usage the past few years flow directly from this vast inventory of spare capacity which can be cranked up easily, and at any time.

We’re not seeing this dynamic however in oil. While global demand is still growing, it’s been awfully slow in recent years and is expected to advance by only a half a percent this year, 2025. Another factor is that the call on oil is nothing like the call on coal. Whereas nations in a pinch dig into spare capacity in coal-fired power generation (not just China, it has happened here in the U.S. and Europe too) such a mechanism doesn’t really exist with oil. And of course outside of industrial applications, oil is mostly a consumer product in transportation and air travel humming to the beat of the global economy, and consumers now have a number of ways globally to reduce their oil footprint.

Two helpful reminders in the matter of oil and peak consumption.

We will never be sure of peak until well after the fact. Years will need to pass.

Entirely separate in your mind the phenomenon of declines, from peak. Treat peak as its own event, one that marks the end of growth only, and nothing more.

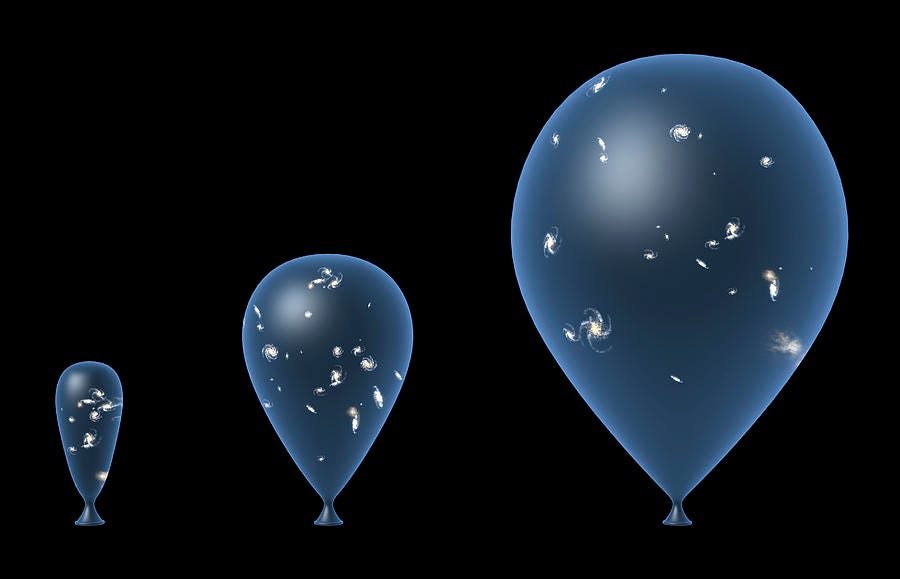

The additive model of energy transition suggests that a peak in global emissions remains far away. Here, it’s helpful to imagine the earth as a slowly expanding balloon that adds just a touch of new energy demand each year, even as fossil fuel demand growth flattens or declines, in some countries. The mixture of factors which keep this slow but steady expansion in play are economic growth, population growth, the bolus of hard-to-abate industrial demand, and the presence of energy sources that are so cheap they actually wind up fostering further economic growth. Right now, for example, natural gas remains dirt cheap and its never a mystery as to how civilization will exploit cheap energy. Indeed, natural gas consumption globally continues to rip higher, growing 2.5% last year, and a steady 2.0% per year for the past decade.

As usual, the climate community continues to overfocus on renewables, asking or depending on them to do it all: covering all marginal growth, disrupting legacy energy pathways, and forcing emissions into decline. Renewables can help with all those goals, but they cannot as yet bear the entirety of those burdens. Cold Eye Earth remains astonished that academics are willing to commit in print to the claim that we will largely be in an all renewable world by mid-century, as Eric Beinhocker and J. Doyne Farmer claimed in their March 2025 Wall Street Journal op-ed:

Still, based on historical growth and its likely S-curve pattern, we can predict that renewables, along with pre-existing hydropower and nuclear power, will largely displace fossil fuels by about 2050.

As anyone who recalls the past 25 years understands, the road from falling costs and tech breakthroughs to disruptive outcomes is a lengthy one in the physical world. This is not software. Cheap wind and solar and their transmission lines and their batteries cannot be distributed overnight to a billion users. While the prospect for getting global emissions into decline after year 2030 looks plausible in power generation, that leaves broad swaths of the global economy still reliant on fossil fuels—and that’s even if you imagine a largely electrified fleet of global vehicles.

In the children’s book Mike Mulligan and His Steam Shovel, a very tidy story of energy transition is told through the retirement of a beloved and personified steamshovel that runs on coal, as the oil-based construction machines arrive and replace all the coal-burning diggers. Mike’s coal based steam shovel winds up as the heating boiler in the basement of a new town hall, and voila—the oil age has begun!

The additive model of energy transition avoids the common zeal however for revolutionary transformation, and takes time to consider all that unfolds at a slower pace, along the way. We will have our renewables revolution in powergrids but the balloon of global energy use will continue to expand until we come up with new tactics.

—Gregor Macdonald