In a Golden State

Monday 15 July 2019

Data reporting for China’s vehicle market has now completed for 1H 2019, confirming that a major economic slowdown is underway. Despite heavy seller discounting in June, China’s total market remains down -12.4% compared to 1H 2018, as ICE cars crumble and EV sales continue to soar. EV are on course to take 7.4% of the market this year, and more than 10% next year.

Sales of Oil Fall have picked up again in the wake of the mid-year update. The Gregor Letter also has enjoyed another wave of new subscribers. You are encouraged to review both Oil Fall at Mid Year, and the single book itself, Oil Fall.

The EIA lowered its 2019 global oil demand for the sixth straight month. But 1.1 mbpd of global growth is still too optimistic. Why? because data now shows 1H 2019 demand growth is running at half those levels. OPEC is also currently forecasting 1.1 mbpd growth while IEA, the laggard agency, has lowered its own forecast to 1.2 from 1.4 mbpd. The Gregor Letter forecast, released in February, is maintained however: full year growth will come in below 1.0 mpbd, and is likely to be as low as just 0.7 mbpd for the year. It’s particularly frustrating to see IEA, in its just released July report, acknowledge that 1H 2019 demand growth has now come in at a significantly lower level than IEA had forecasted, just 0.56 mbpd, while stubbornly clinging to their view full year growth will still hit 1.2 mbpd. Sorry, but it’s frankly embarrassing to be calling for a massive acceleration of global demand growth in 2H 2019, requiring demand to average 1.64 mbpd over the next 6 months, in the face of a major economic slowdown that’s clearly affecting Asian demand. The kicker: EIA has now also had to revise down its estimate of last year’s demand growth, writing “oil demand growth for 2018 was therefore revised down to 1.1 mb/d, the lowest figure since 2011.”

Gasoline taxes are on the rise in the United States. This summer has seen a number of states, from Ohio to Illinois, significantly increase petrol taxes for the first time in many years while in other states like California, staged increases continue. In most cases, the tax increases come after a long period of road infrastructure underinvestment. I wrote about the impending increases in June for Petroleum Economist.

Why didn’t OPEC cuts work? Oil prices did not respond positively to the maintenance of multi-year production constraints, announced by OPEC (and Russia) at the end of June. Worse, when OPEC released its monthly oil market report late last week, the downward revisions to the call on OPEC in 2020 are now forecasted to be 1.34 mbpd lower than this year. The demand growth slowdown—combined with prices that are low enough to cause concern but high enough to maintain US shale production—has escaped OPEC’s grasp. Like a central bank, OPEC is behind the curve.

One explanation: OPEC supply cuts worked better in the second half the 20th century, when the rate of oil adoption was both higher and more durable. Post-war oil demand growth was highly correlated with economic development in the West, with each new unit of GDP growth far more dependent on new units of oil consumption. But around the start the new millennium, OECD demand growth began to peak. While Asia and the non-OECD are now the sole growth centers for oil, it’s not really sufficient as half the world is past peak demand. Counterintuitively, OPEC should increase supply and drive oil prices down towards $40 in an effort to locate better demand. The current approach has not worked for years, and will undermine itself every day oil prices remain at current levels.

David Ricardo had an insight in the 19th century, now being ignored in the 21st century. When countries trade with each other, the efficiency gains to trade allow production advantages to be shared across newly created common markets. But Ricardo’s greater insight is that optimization of local resources leads not only to higher worker wages in both trading partners, but an expansion in the size of total addressable markets. Gains to trade are therefore dynamic. Accordingly, if you start gumming up the works of those trade relationships, you may find you’ve now disrupted gains across the entire ecosystem.

Two reports this week helpfully explain how negative impacts to the Chinese economy are rippling outwards, as uncertainty and disruption has landed on worker purchasing power in China. The first, by John Kemp at Reuters, explains how hits to growth elsewhere will eventually work their way through “the dense network of trades and investment links across Europe and Asia.” The second piece, at Bloomberg, explains why you shouldn’t celebrate the closure of Chinese factories, and the impact this has on worker wages. “Nobody’s investing, nobody’s buying. The trade war is causing people to stop investment because they don’t know where to put the money.”

In my opinion, the hits to China’s economy are driving a new deflationary wave across the global economy, pulling interest rates, trade volumes, commodity prices, and industrial growth downward. Crucially, interest-rate cuts in the OECD will eventually, if not quickly, be disproven as a cure.

California is America’s edge economy. Recent data confirms the Golden State’s inexorable march towards electric vehicles, wind and solar, and battery storage.

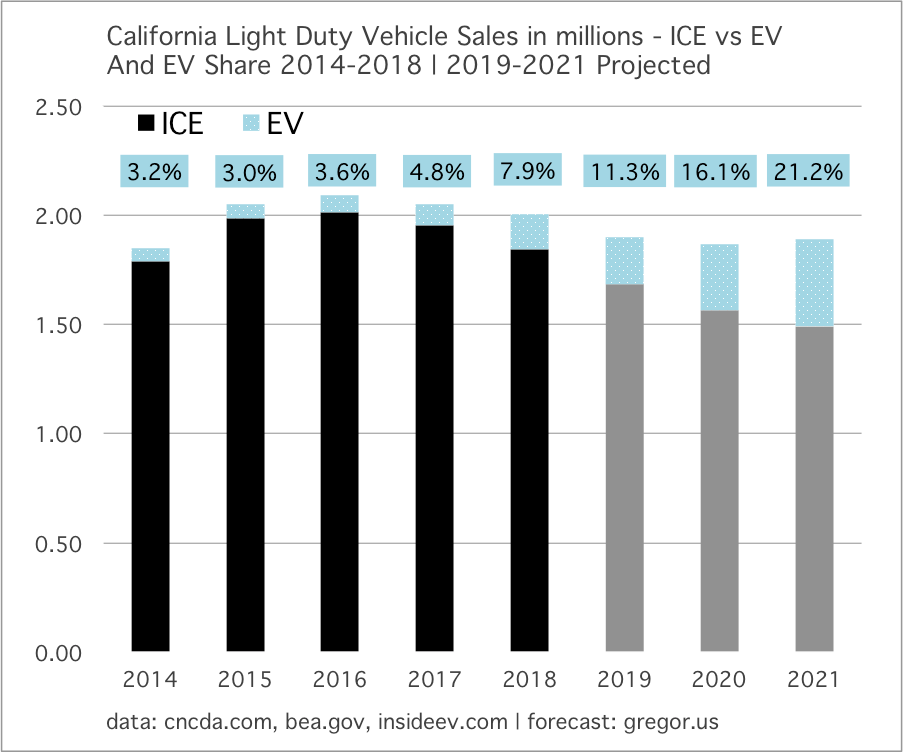

Vehicle sales in California fell by a hefty -5.3% in Q1 2019 compared to Q1 2018, exceeding the national decline. As highlighted in the last letter, EV are therefore on course to reach over 11% of market share this year.

{kind=link}

As important, Q1 gasoline demand data have now completed and show the continuation of a meaningful decline at -1.52%, matching the decline of full year 2018. It is not a coincidence that sales of ICE vehicles and gasoline demand peaked in the same year, 2016, at 2.013 million units and 15.58 billion gallons respectively. ICE sales this year are on course to fall to 1.685 million units, and gasoline consumed at 15.11 billion gallons. And that’s during a three year period when California population will have grown by at least 350,000.

Let's do some math. Using the same metrics offered up and explained in Oil Fall, California sold 157,659 EV last year (pure BEV+PHEV) thus placing a new annual call on state electricity supply of 0.631 TWh. (157,659 * 4000 kWh = 630,636,000 kWh/1,000,000,000 = 0.631 TWh). Question: how much new electricity did California create during the same period, exclusively from new wind and solar? Answer: 5.87 TWh, about 9 X new demand from EV.

For fun, let’s make the matching demands between new EV and new power supply even steeper. As of last year, California had a cumulative fleet of EV on its road estimated at 506,000 units. That represents an estimated annual call on electricity of 2.025 TWh. Again, California in a single year created nearly three times that amount of demand, just from new wind and solar alone. The Oil Fall thesis stands: all new electricity demand from EV in California will be met, and met easily, by the deployment of new wind and solar. Even when annual sales start reaching half a million, or 25% of the total market. And, higher.

These very simple calculations also illustrate how woefully out of step the public remains on the extraordinary energy advantage of EV, and, the threat this poses to oil’s monopoly on transportation. Remember, the relevant metric is not how much existing oil demand is replaced by EV, but how much future oil demand growth is blunted, pinched, or killed entirely by the rollout EV.

Below is a chart showing the comparison between the new demand for electricity created each year by California EV sales, and, the marginal growth of new power from wind and solar alone. The common unit of account here is the TWh—the terawatt hour.

California’s growth of new electricity from wind and solar is currently in a slowdown, as the first great wave of utility scale solar deployment, which started in 2012, is now behind us. The next wave, which relies on expansion of existing facilities, greater deployment of commercial rooftop solar, and a fresh round of utility grade projects, is now getting underway.

The point is that even next year, when California EV sales could reach as high as 400,000 new units, new on-road EV would represent (at best) 1.6 TWh of new electricity demand. But new electricity supply, from new wind and solar deployed next year, will easily cover this new demand.

California’s energy transition is now in a kind of golden state, with a base of fresh wind and solar supply that has run well ahead of state electricity demand growth. As Oil Fall explains, electricity from wind and solar has now broken free and is entering the transportation system.

US utility scale battery storage is set for fast growth in the years ahead, with California in the lead. It’s critical however, to understand that storage will be deployed in several ways, attacking the problem of intermittent electricity from several angles, in addition to new fixed-site storage. Readers are encouraged to review the January 2019 letter, Something About Storage to understand better that fleets of electric cars (and other devices, including water heaters) will be increasingly marshaled into the role of storage.

According to the EIA, solid annual growth in 2019 and 2020 will be followed by a disruptive high growth year in 2021, followed by a resumption of much lower growth in years 2022 and 2023. We shall see. As wind and solar costs continue to fall, that makes the cost of whole-system projects fall entirely, even if cost decline rates for storage are lagging. Moreover, utilities from Arizona to Florida are deciding that not only does it not make sense to build new natural gas generation, but in some cases it now makes sense to build storage, instead of new wind and solar. Why? Because everyone else is already busy deploying new wind and solar: so why not be a market-maker in electricity supply via storage-capacity versatility, in addition to being an electricity generator? In order to have exposure to everything coming in the grid ecosystem, utilities have discovered there’s not only a new profit center to exploit around storage, but storage itself is the gateway to surviving a very disruptive transition.

The public continues to fret about the buildout of charging infrastructure for EV. But really, is there anything more trivial than the buildout of charging capacity? Installation of charging stations is about as technically challenging as the deployment of ATM machines. Every existing petrol station, shopping mall, library, school, and workplace will want to install charging stations; will install charging stations; and are installing charging stations. C’mon people. Among the universe of high hurdles that face energy transition, this just doesn’t rate. You can keep up with the progress of US charging station growth by taking the weekly newsletter update from the Department of Energy’s Vehicle Technologies Office.

—Gregor Macdonald, editor of The Gregor Letter, and Gregor.us

The Gregor Letter is a companion to TerraJoule Publishing, whose current release is Oil Fall. If you've not had a chance to read the Oil Fall series, the single title just published in December and you are strongly encouraged to read it. Just hit the picture below.