Key States

Monday 24 February 2020

California sales of plug-ins fell by 7.48% last year, after growing by 60% in 2018. The weaker sales performance, which mostly tracked the national plug-in sales decline of 8.8%, did not negatively impact EV market share, however. California’s total vehicle market fell by 5.46% last year, enabling plug-ins to maintain their market share first notched in 2018, around 7.75%. In substitution curves a 5% share typically marks a turning point. California is one of several EV markets now crossing that threshold.

Some of the underlying details are also interesting. Pure 100% electrics continued to far outpace sales of plug-in hybrids, mostly because of soaring deliveries of the Tesla Model 3. However, the overdependence on Tesla to achieve US plug-in growth further confirms that unlike both the European and Chinese markets, the factor holding back broader EV sales growth in the US market is lack of consumer choice. We can now rightfully claim that internal combustion engine vehicle sales have peaked in China, in Europe, and also in the sub-markets of the United Kingdom and California. But, if a wider variety of EV models don’t land soon enough in the US market, then the Osborne effect—the consumer’s deferral of a new car purchase for the sake of obtaining an EV—could lose its influence, and EV could proportionally miss out during the next car market rebound.

IEA, OPEC, and EIA are all furiously dialing back their 2020 oil demand growth estimates in light of the coronavirus pandemic. The lowered forecasts arrive as annual global oil demand growth is starting to slump more consistently below 1.00%. Overall, the recognition phase of the oil industry’s dim future seems to be taking hold as institutional investors give up on the sector. For a very good summation of how the market is beginning to price these outcomes, please see Christian Roselund’s piece from this past week, in Energy Transition Magazine:

Were it a standalone country, the state of Pennsylvania would now rank as the 9th largest producer of natural gas in the world. The heady production growth, which has risen over the past decade by 30X, is a kind of resurrection for a state whose historical role as first oil producer goes back to 1859. Yes, the Pennsylvania oil rush was a thing. Today, the state forms about 19% of US natural gas production and, along with Texas which accounts for 24%, has led the US to become the largest producer of natural gas in the world. In the chart below, the US ranking is charted ex-Texas and ex-Pennsylvania which are both broken out for comparison.

The state needs to be included, therefore, in any prospective discussion as to how oil and gas prices, and fossil fuel policies, will affect the US election this November. Roughly speaking, the US contains both oil and gas producing states, and also, oil and gas industry servicing states—with a fair amount of overlap. A basic list of the former type would highlight Wyoming, Oklahoma, Louisiana, Texas, and West Virginia. These are states where the Democratic presidential nominee will have almost no chance of winning the majority required to harvest electoral college votes. But there are also states where engineering, manufacturing, and equipment companies serve the oil and gas industry. Ohio, Michigan, and also Pennsylvania are states where the associated industry supply chain expanded greatly as tight oil and gas (fracking) arose at the start of the decade. And in these states, electoral votes are more competitive.

Here’s why that matters. In the last letter, I mentioned that a long-term weakening of global oil demand, currently accentuated by the China slowdown, was the kind of trend that could hurt fossil fuel prices and affect the energy producing states in the US as we head into the election. And in particular, the oil and gas servicing states too. In other words, current trends—over which no US politician or candidate has much control in the near term—put the incumbent President at risk in the upper Midwest. Especially in the two states where thin margins led to Democratic defeats in 2016: Michigan, and Pennsylvania.

However, the Democratic nominee could make a strategic political mistake were they to advertise a leading-edge idea to outright ban fossil fuel production. It would be a campaign position that would yield no advantage.

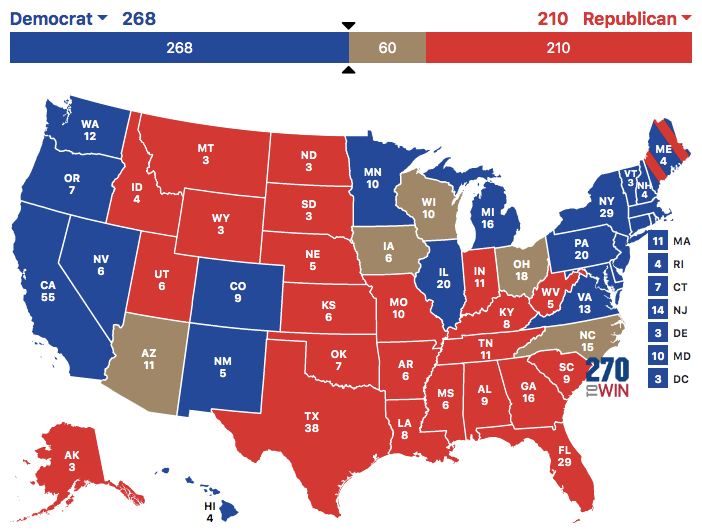

A good place to set any discussion of this type is the electoral college map, and a reasonable estimate of the electoral baseline. I’ll offer mine: we are heading into the 2020 election based on the 2016 result, with Michigan and Pennsylvania automatically awarded back to the Democratic nominee. If such a baseline is wrong, then it’s going to be wrong in Michigan and Pennsylvania outside of the thin margins by which they were snatched away from the Democrats in 2016. In other words, one of the nominees is going to win each state more decisively this time around.

As you can see in this projection, the Democratic nominee easily gets to 268 electoral votes. The road gets harder from there, however. And it’s tantalizing: any single state will get the nominee over the 270 threshold, but, none of these states are easy to win.

The baseline is radically altered however if the Democratic nominee loses Pennsylvania. Proposed, or announced, or even just signaled bans on fracking from the national Democratic party already have in-state Democratic officials concerned in Pennsylvania. And here is the irony: coal is now in its collapse phase in the US. Natural gas, which has been on a huge decade long run of adoption, is increasingly countered by wind and solar. I’ve made this point before: wind and solar will increasingly hurt then crush natural gas in similar fashion to how natural gas crushed coal. So the return on political investment of staking out a bold plan to halt or ban natural gas production would be low, if not negative. A global slowdown, the competitive prices of wind and solar, and receding demand growth for oil and natural gas are all working in favor of the Democrats. But once you stake your name on fossil fuel bans, then you start to own those trends. The upper Midwest has already seen a slowdown due to the failed and ill-conceived agricultural tariffs. It would be tragic, to say the least, to put electoral votes at risk for the sake of an announced policy that may never come to pass and, worse, may be obviated by demand declines already in store.

Incentives are better than edicts. And transportation is a sector where myriad incentive schemes are quite possible, but have yet to be tried. How about this: Los Angeles is exploring an incentive scheme to provide faster security check-ins for travellers arriving at LAX by public transport. According to SmartCitiesDive, a similar scheme went into effect last year in Boston. For those of you who’ve not travelled to L.A. recently, the city has greatly improved transit to the airport through rail, and dedicated fast buses. (I’ve used both as recently as 2018 and they were excellent, though, the rail portion still has some gaps).

What remains disappointing however is that Los Angeles still seems unable, politically and culturally, to adopt congestion pricing. Indeed, for a second time in as many years, Mayor Garcetti has unveiled a sweeping climate and transportation plan—yet one that hopes to curb car use and growth through ancillary, rather than direct means. “LA’s Green New Deal: Leading by Example” will no doubt undertake important projects, greatly increasing clean energy and improving streetscapes. But the congestion pricing features are soft—a plan, as they say, to develop a plan. Politically, it signals that cars are still the third rail of policy in many US cities, especially Los Angeles.

A supplemental update to Oil Fall will be published this April, and all readers of Oil Fall will receive the update for free. Whether you read Oil Fall originally as a single title, or all three parts separately, you will automatically receive an update this coming April as I look ahead to the next five years. Needless to say, visibility continues to improve on the future course of car markets, the widening impact of cheap wind and solar, and the grim future now coming into view for the oil industry. As the first edition of Oil Fall anticipates, the pillars of future oil demand growth continue to erode and some special attention will be paid in the update to two areas not previously addressed: the rise of the electrics, and, the looming assault on plastics.

The supplemental update will be appended to the original edition for all readers.

If you’d like to get started reading today, click on the bike:

China’s economy is under severe pressure and its car market is currently in collapse. Obviously this will eventually pass but Chinese vehicle sales, after falling 18% year-over-year in January 2020, kicked off February by falling over 90%. Forecasting how the market will recover (or not recover) this year has just become nigh impossible. What we do know, however, is that in this market especially, the rebound will proportionally favor EV because EV are already the best economic choice for consumers.

British Petroleum announced a climate plan to become net-zero by 2050, but the effort was widely panned. Rather than criticizing BP however I would pose a question: what is the actual, operational prospect that oil and gas companies can transition away from oil and gas? Observe how difficult it has been, for example, for existing automakers to transition drivetrains from ICE to EV. Simply put, I really don’t know what the public expects supermajors like BP and Exxon to do. Moreover, I don’t understand the obsessive focus on oil companies as a transmission mechanism to conduct or pursue climate policy. BP pumps around 2% of global crude oil each day. And, as demand growth heads towards zero, with a long-term downward pressure on price, the universe of economically recoverable oil will increasingly shrink, favoring the ultra-cheap supply not from BP or Chevron, but instead from state-run oil companies.

At best, it would seem, oil companies could halt their dividends and invest that income stream into the ownership of wind, solar, storage, and related powergrid technology. Supermajors could therefore announce a long-term reduction in reinvestment in existing fossil fuel reserves, and use that capital instead to build a new business around investment in new energy. Yes, the innovator’s dilemma is real. But if Amazon and Google can experiment in the energy sector, there’s no reason why the large oil companies can’t develop as green banks, hiring the necessary personnel to deploy investment capital.

—Gregor Macdonald, editor of The Gregor Letter, and Gregor.us

The Gregor Letter is a companion to TerraJoule Publishing, whose current release is Oil Fall. If you've not had a chance to read the Oil Fall series, the single title just published in December and you are strongly encouraged to read it. Just hit the picture below.