Leap Year

Monday 23 January 2023

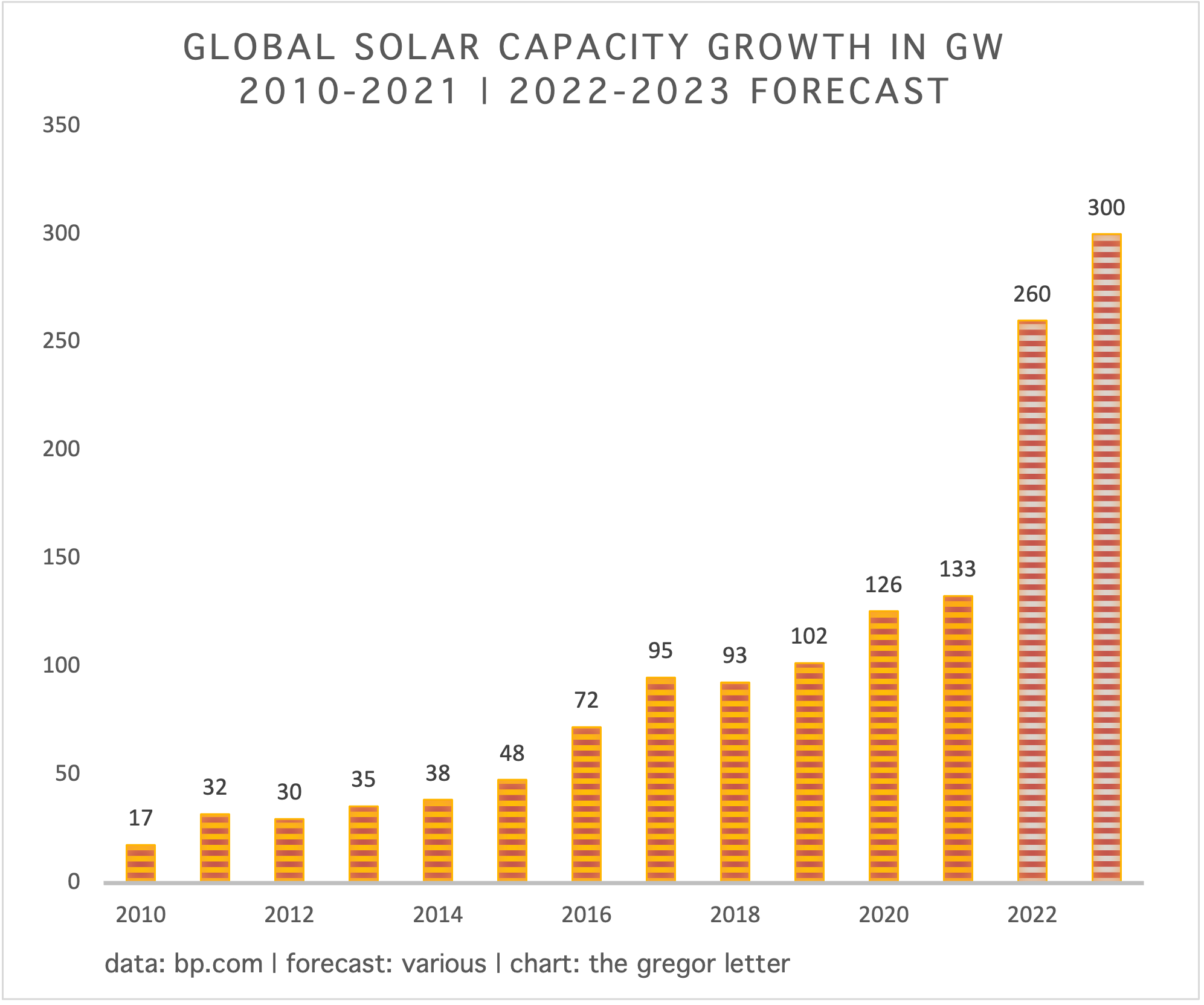

Global solar growth is again leaping higher. After a five year period in which global solar capacity grew in a range of 100-130 GW per year, last year saw a big breakout as growth doubled to roughly 260 GW. Because solar is infrastructure—physical, heavy, requiring steel in the ground—that’s surprising.

One way to explain the aggregate solar market’s ability to still be growing quickly is that it’s not just one market. At one end of the spectrum you have China which entered the year sitting on 306 GW of capacity, the most of any nation. Last year, while the global market in total expanded 100%, by 260 GW, China’s own market is estimated to have grown by 87 GW and now sits just below 400 GW of capacity, providing a third of the growth the world would need to achieve its stellar performance.*** At the other end of the spectrum, solar is thriving in domains where deployment is just getting started, where the base is tiny. Much smaller countries across the rest of Asia are like fireflies, darting skyward.

This also describes a kind of symbiosis in the distribution of solar costs. The big countries drive prices lower through the learning rate from their much higher base, which then transfers a benefit to hundreds of smaller countries now growing quickly. Remember, the cost of solar is not restricted to the level of the panel. The wider universe of parts and equipment can really be thought of as its own category, and significant cost progress has been achieved there as well. The small countries return these benefits by acting as frontiers for the market’s forward progress.

Keep reading with a 7-day free trial

Subscribe to Cold Eye Earth to keep reading this post and get 7 days of free access to the full post archives.