Long Day's Journey

Monday 27 April 2020

COVID-19 is a more deadly, persistent, and damaging disease than the world presumed just 90 days ago. Ultimately, we will likely conduct an accounting of its mortality that uses not only established case statistics, but excess-death statistics. More correct, this method will also be more sobering and will eventually have an impact on policy—especially if you now understand COVID-19 is not a problem that will be solved anytime soon. The Financial Times of London is just one group now examining excess-death statistics, and on Sunday they published their main finding: deaths due to the disease could be 60% higher than reported. What’s compelling is the uniformity—not in the size of excess deaths across all domains, but that all domains see a gap between reported and excess deaths. You can read a discussion from one of the participating FT journalists here:

A University of California study concludes the state is saving $40 million per day, or $1 billion in total so far, due to the sharp reduction in vehicle accidents. The study further claims that traffic flow on some California highways has fallen by as much as 55%. A thought: if we pair the reduced mortality from normal course accidents during the lockdown, with the excess mortality data now coming to light, we should probably conclude excess deaths are even higher. The Gregor Letter previously estimated that gasoline consumption in California would decline by half in the current quarter, a lower level than the rest of the country, because the lockdown in the Golden State came early, and has seen strong participation. Hat tip to Morgan, an avid cyclist and financial market expert, for flagging the UC Davis study.

This coming Thursday I’ll be in conversation with Azeem Azhar, editor of Exponential View. We’ll be getting underway at 5:00 PM London time. (12:00 PM New York, 9:00 AM Los Angeles, 6:00 AM on Auckland’s Friday and 4:00 AM on Sydney’s Friday). I will try my best to put into words the tricky outlook from here, as the oil industry entirely loses its grip on the future, oil dependency rolls onward, and a time gap opens up giving technology a chance to work its magic, moving energy transition forward. This is a Crowdcast event.

Corn prices are falling rapidly as the massive hit to gasoline demand spreads through the American ethanol complex. Grain prices were already under pressure due to the pointless and destructive tariffs, introduced last year by the US administration. While the current cash price doesn’t yet take the market back to the terrible late 1980’s, it’s a reminder that once ethanol was formalized into the US petrol system last decade, corn became structurally dependent on miles travelled by car. Archer Daniels Midland (ADM) announced last week it would idle production at two giant plants, one in Nebraska and another in Iowa, that were each capable of producing 300 million gallons annually. These outcomes are a reminder that deflation, just like inflation, flows like water, finding its way into every corner of the economic system. For a historic table of corn cash prices, please see the monthly updating page at the Ag Decision Maker, from Iowa State University. Corn futures ended the week at 323 cents per bushel.

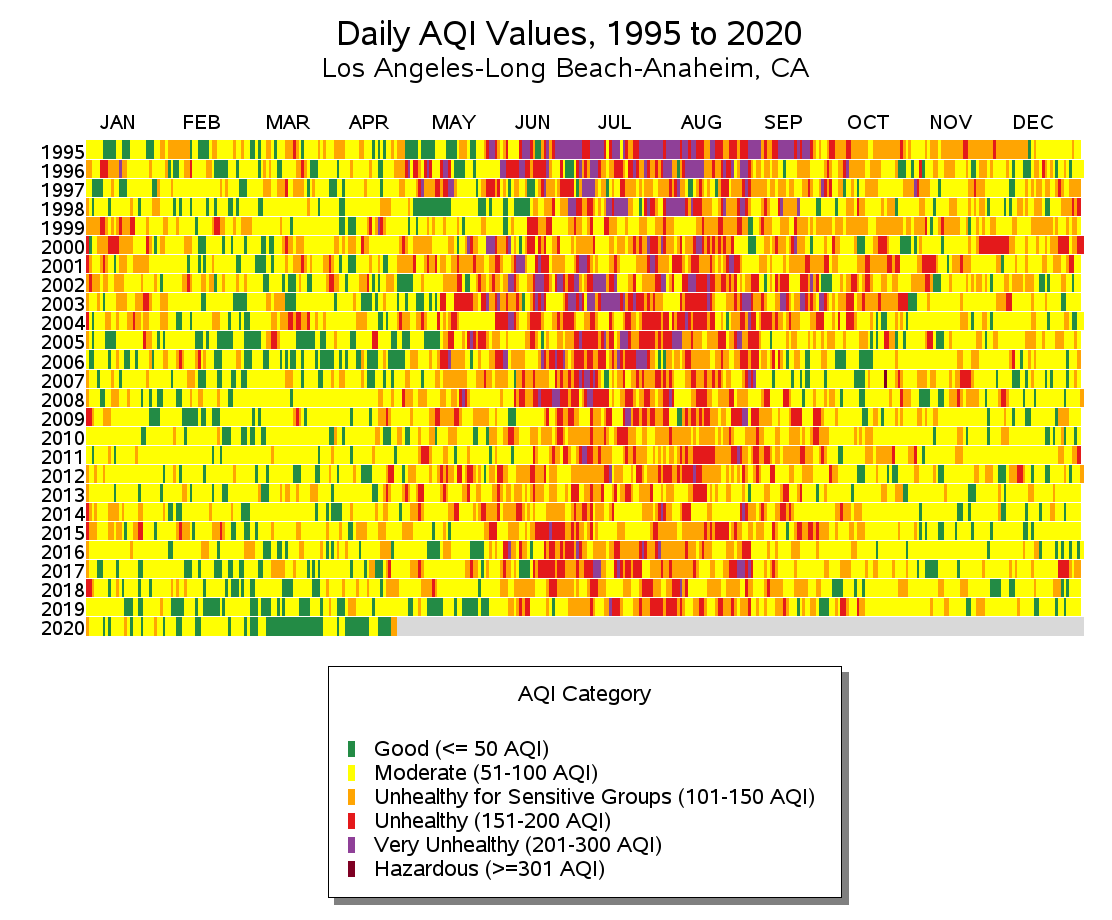

Environmental Protection Agency data indicates that March and April saw the cleanest air in twenty-five years, in the Los Angeles Basin. Examine the bottom row to see the extended block of green, starting in March of 2020. If you are so inclined, you can produce your own chart, like the one below, at the EPA website—for Los Angeles, or many other US cities. Hat tip to Cody Hill, a solar infrastructure professional, for flagging the data.

On the authority-expertise spectrum, the US is very clearly a culture that focuses on the opinions of the famous and the wealthy. Other cultures meanwhile lean more towards expertise. In the US we focus on who is making the argument. In other cultures, the quality of the argument itself carries more weight. You will have noticed for example the successful leadership, and the growing recognition of such, emanating from the Prime Ministership of New Zealand’s Jacinda Ardern. For her handling of the crisis the Atlantic just declared her the most effective leader on the planet. New Zealand culture however is very clearly less susceptible to mass delusion, a quality that has plagued the United States for many decades, especially in the post war era. Accordingly, it’s easier for a New Zealand leader to align with the culture, and roll out policy decisions based on science and reason. Ardern did so after the Christchurch gun massacre, and she has done so again, during COVID. It would be highly unlikely, for example, to see the following public statement as part of a national election discourse, in New Zealand.

It should be said that selecting for authority is a universal human tendency, one that emerged in the course of our evolution. Humans have spent the majority of their time on earth in the period preceding the scientific revolution. During that long span of time, it would have been quite useful if not necessary to follow authority—bereft, as we were, of better tools to establish grounded, opposing views. If you are an optimist, however, you might take some interest in the following possibility: a global health crisis may be the very thing that bends currently regressive cultures, like the US, back towards a higher quality of argumentation, and evidence.

Liquidationists lost the policy argument 90 years ago during the great depression, but that doesn’t keep them from trying. Each crisis tends to bring forth lengthy letters of opinion about the state of the nation’s debt levels from the financial star chamber, and this crisis is no different. In 2010, one such group wrote an open letter to Fed Chairman Bernanke in the WSJ warning about deficits, and inflation in particular, as a result of policy efforts meant to prevent a second great depression. Perhaps, just perhaps, if one repeatedly miscalculates the risk of deflation, one might pause and reflect that the analytical tools required to judge inflation risk are similarly impaired.

Generally speaking, Americas’ celebrity fund managers and financial stars don’t, in addition, understand energy economics, and are very much part of the country’s ongoing disability: the failure to make crucial public investments. Long, long overdue public investments. Turns out, the expertise required to consistently make profits for investors—a hard skill to acquire and one that admittedly reflects genuine talent—does not confer similar expertise in crisis management on a national policy level, nor insightful views on the prospective returns on public investment. In short, the majority of America’s financial celebrities unwittingly volunteer in every public appearance that they fully embrace the household fallacy of the nation’s finances. Needless to say, if one subscribes to the household fallacy, it becomes exceedingly difficult to invest in needed infrastructure, or run a national health care program. Europe has long since surmounted such objections, not only by showing that higher levels of taxation do not salt the fields of capitalism, but in particular, by showing the correct investments pay out to the economy. The losses currently being taken on board in the US, for example, for foolishly trying to run a private health care system in a pandemic are a retort to the American austerity impulse, to put it mildly.

So I read with interest the latest 14 page letter from Paul Singer, of Elliott Management. Unsurprisingly, he recapitulates through tedious innuendo many of the old concerns about inflation risk and debt, while also making a number of unsupported claims about ongoing debasement of the currency. You see, claims Singer, the currency was in fact debased in 2008 but you didn’t notice because other technological and efficiency gains countered the policy mistake. Hoo-boy. Unsurprisingly, Singer is also signatory to the common myth that the Fed, in its all encompassing wizardry, has kept interest rates artificially low. But as with all other signatories to this view, he signals no intellectual curiosity in how the global interest rate market itself began to reflect a strong deflationary pulse starting over 20 years ago.

Since completing my little ebook, Oil Fall, much of my journalism work has focused not on theorizing but actually reporting on the expanding number of companies choosing to construct, or partake, in wind and solar power. Not because of policy, but because of price. Solar and wind are now the cheapest new forms of power generation on the planet. Most astonishing is the cost crash in offshore wind. Most renewable observers, including myself, absolutely did not anticipate that the learning rate would have a major second phase, thus allowing societies to capture the tantalizing energy supply, economically, among the world’s oceans. That’s now happened.

So it was with even more amusement that at the tail end of the Paul Singer letter, he decries that the recent unleashing of capital will be deployed “Not in productive ways, not in the building of useful infrastructure, not doing a better job of educating our workforce so we can grow like crazy…” That’s revealing. Because only last year, Singer was also dumping all over the New Green Deal which, despite having various versions floating around (some bloated, to be sure), is everywhere and at all times an infrastructure proposal. Transit, powergrid, solar, wind, urban development that capitalizes on trains and other efficiencies, and all the jobs that would go along with those investments. But this isn’t about Paul Singer. This is about an entire class of professionals who, having legitimately gained expertise in one area, advertise every day through their pontifications an unexamined assumption this grants expertise in all other areas.

As we conclude the month long sketchbook of the coming Oil Fall update, I can report there is not much to update about Part III, Waste Crash. The price points of new clean energy have moved so much further to the downside that it is now making battery storage economic, in whole system analysis. The free market has now voted. As I wrote last year in my Buzzfeed editorial—fashioned for a general audience—the New Green Deal is already happening. Smart public investments pay for themselves.

—Gregor Macdonald, editor of The Gregor Letter, and Gregor.us

Photos: 1. Cooper Union Building, with event truck in foreground, New York City, 2018, Gregor Macdonald. 2. South Bronx, circa late 1960’s, photographer unknown.

The Gregor Letter is a companion to TerraJoule Publishing, whose current release is Oil Fall. If you've not had a chance to read the Oil Fall series, the single title just published in December and you are strongly encouraged to read it. Just hit the picture below.