Making Copies

Monday 13 December 2021

Ford halted reservations for its new F-150 Lightning electric truck as demand overwhelmed future supply capacity. In this one example can be found a preview of energy transition in 2022. Reports and data from every facet of the clean energy sector indicate that growth of EV, wind and solar power, and mounting demand for lithium-ion batteries is surging. Ford’s future bookings have now been limited to 200,000 deliveries, and comes as GM announced they would electrify their own truck, the Silverado. The truck theme remains very dominant, if it’s not already obvious, and expresses beautifully the American preference for utility vehicles, over sedans. Actually, that observation could be stronger: sedans are so loathed in the US market that trucks and mini-SUVs, on the current trajectory, will entirely dominate the market. A future kid’s car game on long journeys: see if you can spot a four door sedan.

But adults can play a different game next year. As VW, Ford, GM, and Stellantis struggle to meet EV demand, we can track the constraints in semiconductors, battery production capacity, and of course, costs. The example of Volkswagen is particularly apt, as one of the legacy automakers that actually has a lead on the rest. Most analysts thought that VW might produce as many EV this year as Tesla. Well, that’s not going to happen. But a key differentiator between the two companies tells us much about our current juncture: Tesla presides over its own battery production and in addition has a better pipeline of chips. Right about now, therefore, the legacy OEMs are discovering that building an electric car would be challenging under normal conditions, as it entails a very different kind of supply chain. Add post-pandemic supply-chain problems to that mix, and the bottlenecks multiply. Unsurprisingly, Ford has a battery problem.

This week, Ford CEO Jim Farley told CNBC his company needs batteries for its electric vehicles more than it needs computer chips. “We’ll get the semiconductors. That’s a matter of prioritizing the (battery-electric vehicles) over the (internal combustion engine) vehicles,” Farley said during a webcast for the CNBC Investing Club with Jim Cramer. “The issue is batteries. That’s what we have to solve.”

The exciting and fundamental feature of our current energy transition is that it’s characterized not by extraction of an ever more powerful below-ground resource, but by manufacturing. Making copies is a phenomenon that governs evolution and biology, and it’s a framework in which this, the third historic energy transition of the past 250 years, will come to be understood. Stamping out copies within the domain of manufacturing adheres to a lovely upward curve of efficiency increases. But it can be challenging, as we see right now, because mass production is capable of overwhelming the supply of inputs. Why? Speed. Notice how fast transition is starting to move as we shift more fully from a policy dependent regime to a consumer and business preference domain. And rapid cost declines don’t merely allow for better adoption, they allow for an expanded set of possibilities. In the journey from the insanely expensive to the surprisingly cheap, the landscape shifts from difficult business decision making, to one of convenience and surplus. That’s why the latest idea in renewables, to overbuild solar, is now possible.

Even the most resistant processes can somehow be pulled into this phenomenon. The physical properties of wind power, for example, in which energy captured can be increased non-linearly through increases in blade length can be leveraged through this same learning rate, in pursuit of much higher wind resources offshore.

There are a couple of broad themes for readers to consider, therefore, as we head into 2022. First, the upside risk to material science breakthroughs and other material substitutions that could upend the current inevitability of constrained battery capacity and lithium. There are innovations brewing in the battery world—everything from iron-air technology in big-box storage, to the prospect of aluminum-ion—that are not going to be commercialized next year, but could pose a threat or a complication to lithium-ion dominance. Second, if oil prices remain elevated through the current OPEC policy, which is of course a discretionary not a geological constraint, then the demand shift to EV could be even more accelerated. But that leads us to the primary theme for 2022: production constraints as everyone from Ford to Rivian to Stellantis and GM scrambles to build battery production capacity. We might say that streamlining an energy transition down to the level of making copies is absolutely disruptive in a way that is thrilling. But the disruption itself could be disrupted by its own capabilities. To put a fine point on the risk: investors are currently riding a giddy wave of capital expenditures and rising demand for new products, and asset prices reflect that future growth. But growth rates could be reduced substantially as demand pushes either capacity or input prices to crippling levels.

China’s EV market has now converted from one controlled by policy to one led by consumer preference. Those were the comments from CAAM spokesman Chen Shihua after the latest stunning data on the country’s EV adoption surge. China’s plug-in sales are now on course to hit 3.3 million units this year, with one month of data to go. Given how strong sales have been this Autumn, total sales might actually reach 3.4 million.

To put this in context, EV sales have now achieved 10X growth from 331,000 in 2015. That is astonishing. EV market share also conforms to growth patterns long observed, showing that the 5% market share level tends to be a take-off point. Plug-in share will hit somewhere between 12.5%-13.00% this year. ICE sales are in collapse.

Imagine, for example, that in 2015 you forecasted that “while EV will eventually be compelling, ICE sales will still grow nicely for many years as EV slowly come online.” That outlook would have enjoyed great comfort in the next two years, as ICE sales rose into a peak while the EV share looked weak, at just 2.69%. 2018 was the big warning however that the key 5% market share level was near. But a small reprieve occurred: tariff wars, and a pandemic reduced total auto market sales, and delayed the 5% threshold to the pandemic year. And then, woosh!

Relatedly, is it really a coincidence that China’s road fuel demand has not grown at all since 2016? Perhaps it is. But how likely is that? Remember, the near term thesis about the ICE/EV changeover is not that it causes oil demand to decline. Rather, that the onset of EV places a growth constraint on oil demand. The chart below combines both gasoline and gasoil/fueloil as recorded by the IEA.

And just a note on IEA forecasts. For three consecutive years the IEA had China road fuel growth at wildly high levels, only to erase those forecasts each year through downward revisions. Is the agency making the same mistake again?

Higher oil prices are so persuasive they’ve apparently caused investors to back off completely from peak demand views they held prior to the pandemic. That’s from a recent Bloomberg survey, and it’s fascinating given that nothing at all has changed in the demand picture. 2021 demand will come in lower than 2019, and both EIA and IEA forecast that next year’s demand will, at best, match 2019’s levels.

When, then, might oil demand peak? Bloomberg Intelligence analysts frequently survey oil investor clients on that question, offering intervals of time in which these sector experts think that global oil demand will reach its top before rolling over.

In June of 2019, a fifth of those surveyed said that oil demand would peak as recently as February of this year, more than a third of investors said that demand would peak in just a few years, by 2025. In the first four surveys, the majority of respondents said that oil demand would peak within this decade.

That is, until Bloomberg Intelligence’s most recent survey last month — in which only 2% of investors responding said that oil demand would peak before 2025, and fewer than 40% said that it would peak before the end of the decade. More than a third of investors responding expect demand to peak between 2025 and 2030, but nearly the same number see that peak happening later, between 2030 and 2035.

The dramatic change in outlook is explained by the psychological vulnerability humans have to confusing rates vs levels, a concept that is taught in most Economics 101 classes. Because the price increase and the demand increase from the March 2020 lows was so dramatic (well of course, considering the depth of the lows) this has entirely changed demand outlooks. It’s comical, but revealing. The Bloomberg article gains an extra layer of meaning for the fact that it carries this chart.

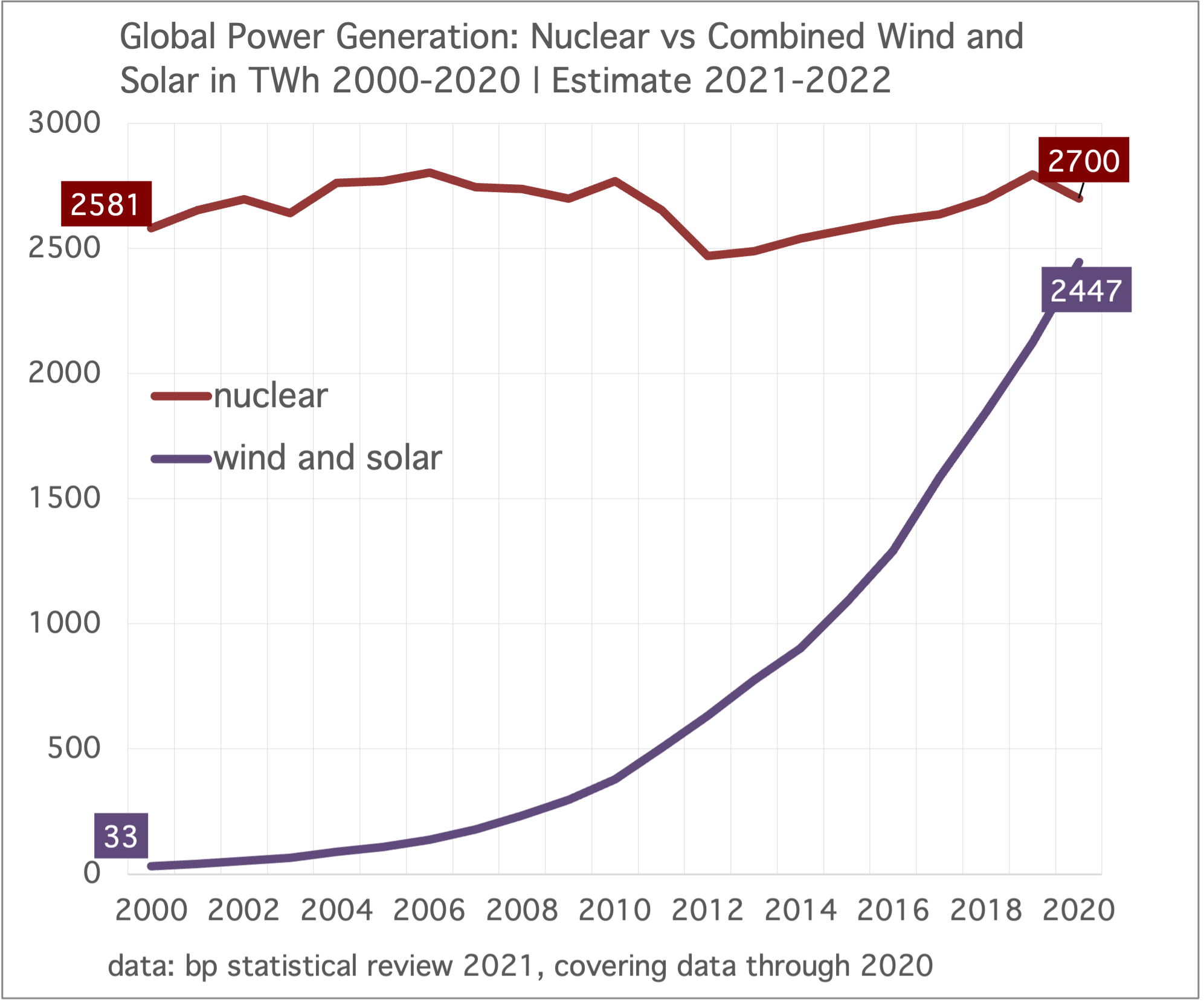

Nuclear power continues to be chosen by intelligent non-experts as the only real way to decarbonize the world. The common through-line in these views concentrates without fail, on the rate by which nuclear can be deployed. David Frum is the latest to fall into this trap in an otherwise reasonable piece about Germany’s mistake in closing nuclear capacity. Frum very specifically says: Nuclear energy, too, has costs and hazards: radiation risks in the present; the disposal of spent fuel that must be safeguarded for centuries to come. But no other technology can so massively and so rapidly substitute for carbon-emitting electrical generation. And he repeats that theme in a series of tweets, about his essay. To be honest, this really feels like a borrowed idea that gets passed around alot. One often hears the claim: there is no climate solution without nuclear. It’s just math.

Why these commentators don’t check the data before coalescing around this shared myth is a mystery, but like so many beliefs these days, herding is not uncommon. Nuclear is in fact awful in achieving speed. Even in fast-market domains like China it can take at least five years to bring new capacity online. Solar, by contrast, is so fast that in a comparable market like India, large utility scale solar can, and has, come online in as little as a year. The super-contrast between the engineering complexity between the two technologies explains the difference. Let’s put this plainly: imagine a domain which has no material constraints, no public feedback constraints, no political constraints. Solar construction would beat nuclear construction continually. There is simply no contest.

The Gregor Letter remains a strong advocate of building new nuclear, and has been on record in that position for years. It’s because solar and wind have so clearly won the race on both cost and speed, ironically, that makes for an opening for nuclear as a booster or amplifier of decarbonization. With nuclear, we could be going even faster. Just don’t make the case that nuclear is fastest, or that it’s the leader we’re ignoring. It’s not the leader, and it could not be the leader. Though it’s true, we are ignoring it. The chart below is indeed a testament to the speed of wind and solar. But it’s not an accurate reflection of nuclear’s potential. Nuclear could grow nicely, at a much slower rate of course, and it could greatly aid in decarbonization as a support structure to the main buildout to come in wind, solar, and storage.

But there are new reasons to support not only the rescue of existing nuclear power plants—many of them old, and in need of government support—along with the building of new nuclear. In domains like the US, for example, the closing of existing power plants creates a new hole to be filled, and that gap is often more readily filled by natural gas. The reason for this is natural gas capacity is quite ample already. Yes, rescuing old plants costs money, and lots of it, but the cost argument begins to lose its edge when the risks of climate change are so high. As for new nuclear, the way in which the world could seriously leverage new nuclear would be through creating plentiful and steady clean electricity to make green hydrogen. And we need alot of green hydrogen to decarbonize the hardest, most impervious sectors like steel.

The nuclear waste problem of course remains a fiasco. Plants like Pilgrim in Plymouth, Massachusetts (now closed, and near where I grew up) have functionally been converted into a nuclear waste storage sites. To expand new nuclear, society will have to come to terms with this problem; one it’s been unwilling to face for decades. And that brings us to the central issue around nuclear. It’s not that it’s slower to deploy. So what? And it’s not that it “costs” more. Again, future costs from climate change are brutal, they tower over such costs. No, nuclear has an ongoing social problem. That flatline in the above chart going back two decades is derived exclusively from this challenge. Where nuclear is needed most—near population centers that already have robust natural gas infrastructure, but which have less land for solar—is where you will find the strongest opposition. That is where you will also find wealthy, connected, influential people who have, can, and will express their influence successfully to stop nuclear.

Accordingly, essays in magazines exhorting and blaming and claiming that we can only decarbonize through nuclear—because man it’s just math you know?—are just recreational exercises.

The mean reversion folks are going to have to take a loss on their view that society is going back to work, fully resurrecting the old ways. The Gregor Letter has forecasted for the past year that the majority of workers will indeed return to workplaces, but office workers will not—and the hybrid solution of part-time office and part-time at home will come to dominate. This reality is unfolding in real time, and it has major implications for oil demand growth. Or rather, it adds support to the view that the world has now permanently lost a tranche of commuting demand that helped form the steady baseline in OECD demand.

The Wall Street Journal has a very extensive, probing piece on this subject. Values in commercial and office real estate are also changing permanently, as a result. Simply put, while hangers-on still make the case for a return to normal, office properties are already undergoing conversion to warehouses and apartments. The future of offices themselves frankly looks more like a downsized, but flexible workspace—something along the lines of a WeWork property where conference rooms, swing spaces, and perhaps an auditorium are required. Just not the vast hallways and numerous floors to house every employee. Westchester County in NY, parts of New Jersey and suburban Washington DC are classic examples of regions where massive corporate headquarters once stood, and still remain. But the future looks more like one where these are sold, redeveloped, converted.

One of the more insightful but unintentionally prescient pieces to publish last year observed that many US workers these days wake up early, check information on a home PC, mobile device, or laptop, and then commute by driving to a train station, arriving in a big city 60 minutes later, only to arrive at work to log back on again to a screen. It was not an optimal or efficient arrangement, and the pandemic kind of blew the lid off the waste of it all.

Just to bring this back around to oil: the US EIA started expressing the view about two to three years ago that US road fuel demand had peaked. And they were right. In their latest forecast, US gasoline demand makes it back to 9.0 million barrels per day next year, but that is down from 9.3 mbpd in 2019, and demand had flatlined around that level for years before. The kicker: and unlike China and Europe, US EV adoption has barely even started yet, on a national basis. That comes next.

—Gregor Macdonald

The Gregor Letter is a companion to TerraJoule Publishing, whose current release is Oil Fall. If you've not had a chance to read the Oil Fall series, just hit the picture below.