Markets II - Thales and the Future

Monday 1 June 2026

A surprisingly relaxed year for global power growth made it easier for wind and solar in their ongoing effort to cover marginal demand in 2025. According to the IEA, in fact, combined generation from new wind and solar, along with the help from nuclear power growth, almost met total demand. Impressive! As energy transitionists understand, that is the holy-grail crossover point that, if breached—and then breached repeatedly—would inevitably trigger emissions declines in the global power sector. Alas, we are still not there.

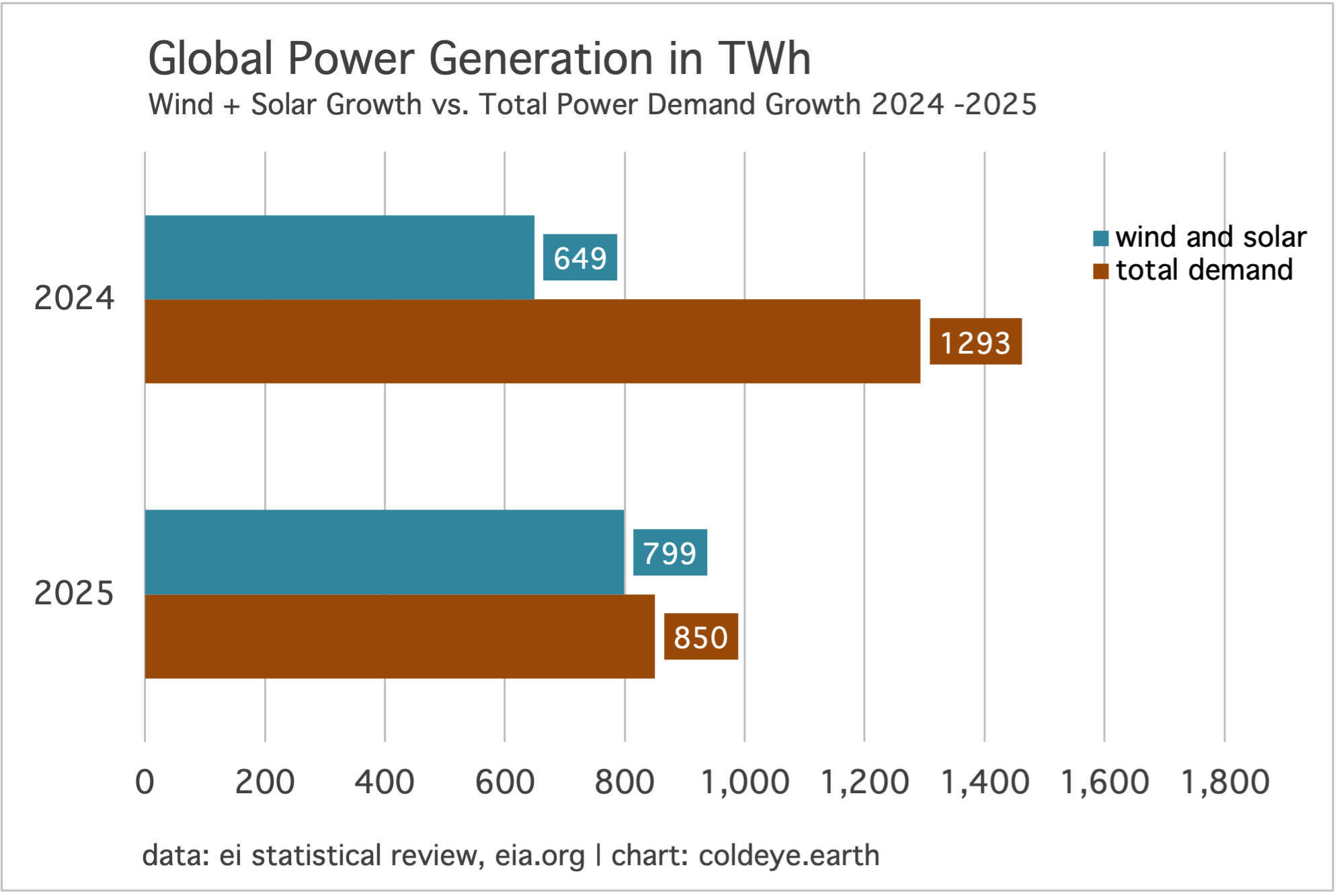

According to the IEA, total global power demand rose by an unexpectedly weak 850 TWh in 2025. That represented just 3% growth during a period when the IEA had confidently forecasted steady, sequential 4% annual growth for last year, this year, and the next. In the chart below, you can see the year-over-year deceleration in total demand, and how combined wind and solar growth fared by comparison. While nuclear is not shown, according to the IEA, it alone advanced by 34 TWh. Ergo, when you add that to wind and solar’s 799 TWh of growth, the total nearly covers the entire 850 TWh.

Just to remind, Cold Eye Earth remains uncomfortable with the catch-all category known as “renewables,” which is a kind of jambalaya stew composed of everything from highly unstable hydropower to dreaded biofuels (ugh). This is not to say that emerging sources like geothermal, for example, aren’t both exciting and promising, but rather that sources like wind, solar, and nuclear are superior for tracking purposes, because they adhere to manufacturing and thus learning rate dynamics in addition to being either zero or near-zero carbon sources. Moreover, as Cold Eye Earth has pointed out for years, wind and solar are the clear leaders—by leaps and bounds—beyond all the other “renewable” sources. If you’re looking for the tip of the spear in how we’ll eventually decarbonize the power sector, look always to those two (with nuclear just behind) until some radical scientific and economic breakthrough occurs that can scale. Hint: If pressed to identify where that breakthrough may arrive among geothermal, hydropower, biofuels, wave (ocean) energy, hydrogen, and some as-yet-unnamed energy source, the current choice would have to be geothermal.

Of particular note in the IEA’s assessment of last year: The agency reported that the big swing downward in power demand was driven largely by a more relaxed year for cooling demand in India and Southeast Asia. This reminds us that climate change and climate volatility are increasingly competing as major factors in our more routine efforts to track trajectories from fossil fuels, wind and solar, and overall economic growth. Indeed, it sounds like the downshift in electricity growth was a major factor in bringing total global growth for all energy down to a slower pace in 2025:

All major energy fuels and technologies grew in 2025 – but at very different rates. Overall global energy demand growth slowed to 1.3%, just below the average for the previous decade. Slower economic growth and slower growth in energy-intensive industries in some regions, lower cooling demand, and faster efficiency improvements all contributed to slower demand growth.

To put some numbers on this thorny problem, it is estimated that global air-conditioning accounted for 7% of total power demand in 2022, or about 2,100 TWh out of 29,000 TWh total. That’s just about exactly half the power consumed in the U.S. that same year. At this scale, uncertainties over how much new demand will come from, say, data centers, start to fade rather quickly because we literally find ourselves in an era where volatility in cooling demand is so substantial that it alone can turn the knob on global power and our efforts to decarbonize it. Here we run into an old nemesis, a flaw in human thinking: We are not good at understanding scale. This flaw is how we get such axioms as “One death is a tragedy, but a million deaths is a statistic.” This bias leads us rather habitually to discount the system as it currently exists—colossal, profoundly embedded, hard to dislocate—while overfocusing on local disputes around a transmission wire, an offshore wind farm, or the location of a battery installation.

Why don’t wind and solar simply race ahead and quickly bury continued growth from fossil fuels in the global power sector? Why don’t they put this contest to bed already? Why does the volume of new generation each year from wind and solar pretty reliably come up to the line of marginal growth, and then halt? Why don’t wind and solar simply overrun the system, in a spectacular viral distribution? The reason is that wind and solar, while cheap, are not nearly as cheap when compared to other historical technologies that quickly overwhelmed their markets. Essentially, wind and solar are cheap enough to be the obvious choice for replacing retiring power generation, but not so cheap as to economically destroy existing generation. Just a few examples from the past:

Keep reading with a 7-day free trial

Subscribe to Cold Eye Earth to keep reading this post and get 7 days of free access to the full post archives.