Not Fast Enough

Monday 7 July 2025

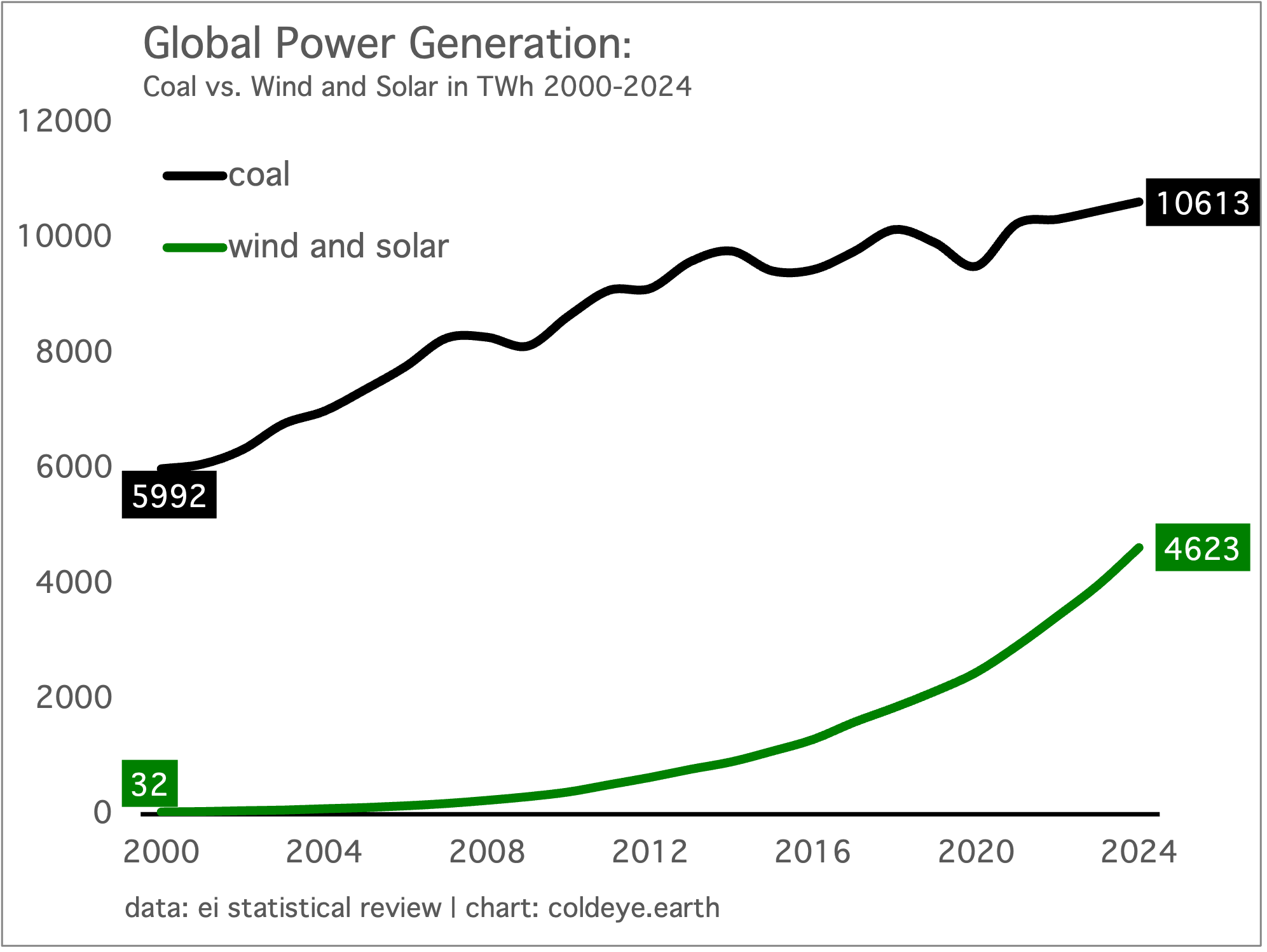

Global growth of power demand last year once again overwhelmed growth of wind and solar. Power generation grew by a heady 4.3%, or 1,293 TWh from 29,963 to 31,256 TWh. Combined wind and solar generation grew by just half that total, 649 TWh. The gap between the two, 644 TWh, was filled with both good news and bad news. Nuclear and hydro generation grew by a combined 272 TWh. Yes, that’s encouraging; but neither nuclear power nor hydro is a reliable growth technology and cannot be forecasted with any ease, as they are volatile year to year. Meanwhile, coal in global power continued to grow, by a very unfortunate 152 TWh; and natural gas grew an even larger 192 TWh. The remainder, 28 TWh, was met by various minor sources, like geothermal and biomass.

Notice that the difference between a 4.0% and a 2.9% growth rate from this year through 2030 is substantial, and winds up as a total spread of 2,444 TWh (39,549 vs. 37,105 TWh). For comparison, that’s nearly twice the size of last year’s total growth of 1,293 TWh, allowing us to say that what appears to be a minor difference in growth rates translates to nearly two years of growth by the end of this decade.

We should favor the higher forecast. If we assume a continuation of the 4% growth rate per the ongoing IEA forecast—which sees at least three straight years, starting last year, in which global power demand is expected to grow by 4.0%—then total global power generation growth will add another 1,250 TWh in 2025, 1,300 TWh in 2006, and 1,352 TWh in 2027. Cold Eye Earth has been writing about this problem for some time now. Here is an excerpt from the February 17, 2025, issue, Downside of a Power Boom:

The most recent IEA electricity report confirms no progress will be made in the decarbonization of global power over the next three years as total global system growth is now running so hot it will consume 100% of renewables growth from 2024 through 2027. Cold Eye Earth has warned repeatedly that any sustained acceleration in total system growth would erect an even higher hurdle for decarbonization and the IEA’s Electricity 2025, released just last week, points exactly in that direction—increasing its own forecast substantially that global power grew 4.3% last year, and is set to grow by at least 4.0% each year through 2027. In such a scenario, the fossil fuel underlayer in global power will remain safe and intact, entirely undisturbed or reduced by fast growing renewables.

With respect to the power sector, however, the Additive model of energy transition implies that both coal and natural gas growth will eventually fall toward zero, and all marginal growth in power will eventually be dominated by new clean generation. And yet we are now mid-decade, and wind and solar are still not covering this growth—far from it.

Data note: If we adjust for the leap year in 2024—which is the practice of the EI Statistical Review—global power grew by 4.03%, not 4.3%. This is relevant to discussions centered on single-year performance, but not so over time.

Energy transition was already running into two notable hurdles, even before the Republican Party returned to power in the U.S. It will therefore be important in the years ahead not to fool ourselves into thinking that a fast transition was underway until U.S. policy shifted hard in the other direction.

• Hurdle 1: Wind and solar are not competitive with existing, economically viable fossil fuel power generation. As a result, wind and solar are not accelerating the fleet turnover cycle, and no single case or handful of cases contradicts this point. The existing fossil fuel fleet is turning over on its own schedule.

• Hurdle 2: Electrification is a foundational goal of energy transition, but its success places pressure on clean generation to cover marginal growth when that growth rate steps up to higher levels.

The first hurdle is far more imposing than the second. Wind and solar are fast and cheap, so it’s inevitable that they will indeed cover nearly 100% of global marginal growth in power. The second hurdle therefore is surmountable. The first hurdle however will not be solved until some combination of costs actually crosses key thresholds, such that the opex (operational expenditures) of existing fossil generation moves higher, as wind and solar and batteries get even cheaper.

Coal has proven to be quite a devilish problem in global power. While few think we can easily displace coal at scale in various industrial uses like steelmaking, wind and solar and batteries are a formidable competitor to coal for new capacity in power. And yet coal continues to make small but steady advances despite attacks from all sides—not just renewables, but natural gas too.

There’s no question that the advent of wind, solar, and batteries has slowed and will continue to slow coal growth in global electricity. But this is the outcome we can already expect in the Additive model of energy transition, a concept recently clarified by historian Jean-Baptiste Fressoz. | see: the review in The London Review of Books, and also the Cold Eye Earth coverage in Momentum Lost. | In the Additive model, new energy resources greatly slow and occasionally halt the growth of legacy energy sources, eventually coming to dominate all growth. Yet the legacy sources—because they are embedded or aligned with legacy infrastructure—maintain their toehold long enough to eventually grow again, if even just a little.

The declines, however, never quite arrive. And if they do, they do not last.

We may indeed already be seeing such an outcome with coal. After hitting an initial peak in 2014, coal used for power actually declined for two years, then recovered in 2017 and peaked again in 2018, before falling for another two years in 2019 and 2020. And now, after that oscillation, coal in global electricity is back on the move again, rising for its fourth straight year in 2024, advancing by a newly steady 1.0% or more per year.

Editor’s Note: A number of global climate think tanks and voices have notably stopped making forecasts for peak emissions in global power this year, after having failed at that project for several years running. That’s a far more appropriate and rational response to actual conditions. Also, thanks for reading Cold Eye Earth.

Counting renewables growth may very well be an enjoyable pastime, but doing so rather misses the point. Global wind and solar expansion has progressed at a very exciting, rock’n’ roll pace for 15 years now as the two technologies swept the globe. They prevented a ton of new fossil capacity from being built and have reached high levels of penetration in big domains like China, Europe, and the U.S. Together they produced 4,623 TWh of power last year. That’s just a bit more than total U.S. power generation from all sources. Alas, while this is not sufficient to solve the climate problem, it is crucial to the task. We couldn’t possibly decarbonize without wind and solar, but as Cold Eye Earth has pointed out for several years, to actually get total emissions into decline, or power sector emissions into decline, will require unpalatable policy responses that are very hard to sell to voters.

One gets the strong impression that many in the climate community religiously count renewables growth as part of an ongoing, maybe next year framework. The collective belief is clearly that if we just build faster, and bigger, we can not just catch up but overtake fossil capacity in power. The catching-up part, as discussed, is attainable. It’s the overtaking part where the framework breaks down, where the belief runs aground on the stubborn economics of existing capacity, which is why we’ll be saying maybe next year for a long while.

With that out of the way, let’s go ahead and count some renewables! Generation from combined wind and solar grew by 16.33% last year, advancing by 648 TWh, from 3,974 to 4,623 TWh. This growth rate was just slightly below the trailing five-year compound annual growth rate of 17%, and thus pulls that historical rate down just a touch to 16.77%. Put another way, the simple five-year trailing historical growth rate chosen by Cold Eye Earth has proven to be a highly reliable forecasting tool, which continues to pretty much nail down the annual advance of wind and solar generation. (Cold Eye Earth would be quite happy to see a few years of forecasts ruined if it meant that combined wind and solar grew well above projections).

Global power consumption is on course to outdistance the growth of wind and solar generation through the end of the decade. Using the 4.0% growth rate for global power expansion and the 16.77% rate for wind and solar expansion, global power is set to advance by 8,293 TWh through 2030, while combined wind and solar generation is on course to advance 7,097 TWh. If this scenario plays out, not only will clean generation fail to trigger any decline in fossil generation, but we won’t even witness peak emissions in global power. To be sure, miracles could take place in either nuclear power or hydro power that fill the gaps and actually get us “pretty close” to peak emissions, but it’s not something you could forecast. As always, hope is not a strategy.

Oil may actually be the one fossil fuel whose growth is not only slowing, but may be hard to revive. The primary factor here of course is the torrent of electrified transportation solutions that are fanning out across the world in the form of EV passenger vehicles, EV trucks and buses, and in Asia specifically, EV two and three-wheelers. Collectively, these have been placing a moderate drag on petroleum consumption growth for several years now. The big twist that’s hitting petroleum a bit harder now however is that global ground zero for EV adoption happens to be taking place in the same country that’s also the remaining growth engine for oil: China. As a result, global oil consumption grew less than 1.0% last year.

China’s oil consumption actually fell in 2024 by 1.1%, according to the just released EI Statistical Review. EV sales both passenger and commercial reached a legitimately heroic 47% of China’s vehicle market last year. While fleet turnover is a big hill to climb—because despite EV taking half the market, ICE vehicles are still taking the other half—this is the kind of overtaking that could really put a lid on China’s oil demand growth. Remember too: China is much more of a power based economy, than an oil based economy, as much of its manufacturing base is yoked to electricity. The widespread personal automobile ownership is a more recent phenomenon, especially when compared to a country like the U.S.

The free market has done a remarkable job so far in conducting global energy transition. Yes, there have been important policy incentives over the past two decades that helped deliver us to our current location, but the learning rate in manufacturing and continued tech advances—driven greatly by the profit motive—have done most of the work. The challenge now is that to make the next leg of progress will require a big, second round of incentives and disincentives, many of which would cause inconvenience. Global energy transition is not at a standstill, but it’s not progressing fast enough at all to bring the emissions declines we hope for into view.

—Gregor Macdonald