Oil Fall At Mid Year

Monday 1 July 2019

The primary Oil Fall forecast—an acceleration towards EV and global electrification—is paradoxically getting extra support this year from mounting downward pressures on the global economy. This week’s letter will be a tour of charts, therefore, to update readers on how car markets, oil markets, and electrification are progressing in China, the United States, and, Oil Fall’s ever reliable case study, California.

If you’ve not had a chance to read Oil Fall, you should. Much of the ongoing discussion in The Gregor Letter concentrates on the three major themes of the book: how electricity will disrupt oil in transportation; how China and the US will lead the world in creating enormous new supplies of this electricity through new wind and new solar; and, how energy transition itself is not a cost-making, but rather a cost-saving endeavor the world should not only undertake, but kick forward now at greater speed.

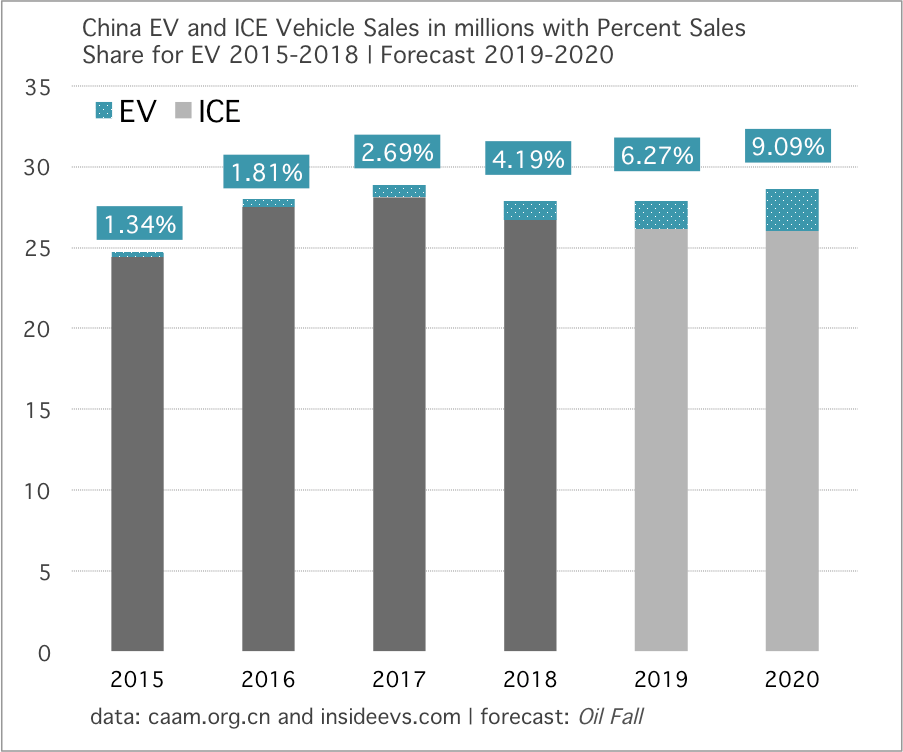

Let’s begin with the most important chart in the world right now—even if saying so risks indulgent hyperbole. The foundational shift in China’s vehicle market (the largest in the world) is taking place where rate-changes in global oil demand, and electrification of transport, come together in a flashpoint. China’s total vehicle market, which started to crumble in July of last year, is falling harder and for longer than most expected and has pressed further downward through the first five months of 2019. This has brought the 2019 full year forecast of EV sales down slightly, from around 2 million to 1.8 million, but, has actually increased the market share forecast for EV because the entire market is currently on pace to fall by a very substantial 12-13%.

EV sales in China last year reached 1.26 million in a total vehicle market that fell only gently from 28.88 million in 2017, to 28.08 million in 2018—giving EV a market share of 4.49%. But this year, China’s total vehicle market is getting hammered. Total sales are set to fall by 3.5 million units, from last year’s 28.08 million to 24.57 million.

Let’s compare the above chart to the one published in December, when the Oil Fall series completed and was released as a single eBook. Notice how the EV market share forecast has grown to 7.43% this year (chart above), from the 6.27% estimate published with Oil Fall (chart below). Notice also the strong rebound in total sales forecasted for next year, to levels back above 26 million (chart above), but how the rebound is almost entirely dominated by EV sales, pushing EV market share next year to 10.87% (chart above). In short, ICE sales in China peaked in 2017 above 28 million, and will never make it back to those levels. Even though ICE sales are slated to rebound very slightly next year—as a typical offset to this year’s very steep fall—they only make it back to 23.6 million units in sales (chart above).

The impact on the global oil market from China’s broad slowdown is likely to carry through from this year, into next. Oil prices have recently bounced off their lows on a short-term combination of rising Middle East tensions, expectations that a rate cutting cycle is to begin, a brief reprieve in the China-US trade conflict, and the announcement this week that OPEC will extend production cuts. But these short-term trading effects only serve to interrupt oil’s healing process. Oil, to its credit, was trying to find a better price to balance supply and demand around $52 a barrel, just last month. A big mistake that oil had made earlier this year, and was trying not to repeat, was its advance along with SP500 in Q1 2019. When the SP500 recovered in June from a second decline, oil made a solid effort to not get fooled again.

But alas, oil has reluctantly and harmfully been dragged higher a second time, and we are back at prices closer to $60. Such prices are not supported, and can’t be supported, by the rate-of-change taking place in China’s oil demand, as driven by its road fuel consumption. Road fuel demand fell gently last year by 1.00%, and is on course to fall by a much larger 6.00% this year.

Meanwhile, the IEA which remains ever biased towards higher oil consumption growth has, predictably, started to backpeddle. Lowering their 2019 forecast from 1.4 mbpd of growth to 1.2 mbpd is a start, but the IEA remains behind OPEC for example, which has already lowered to 1.0 mbpd of growth. In early February, The Gregor Letter explained why the downward risk for this year’s demand growth was as low as half the IEA forecast, at just 0.7 mbpd.

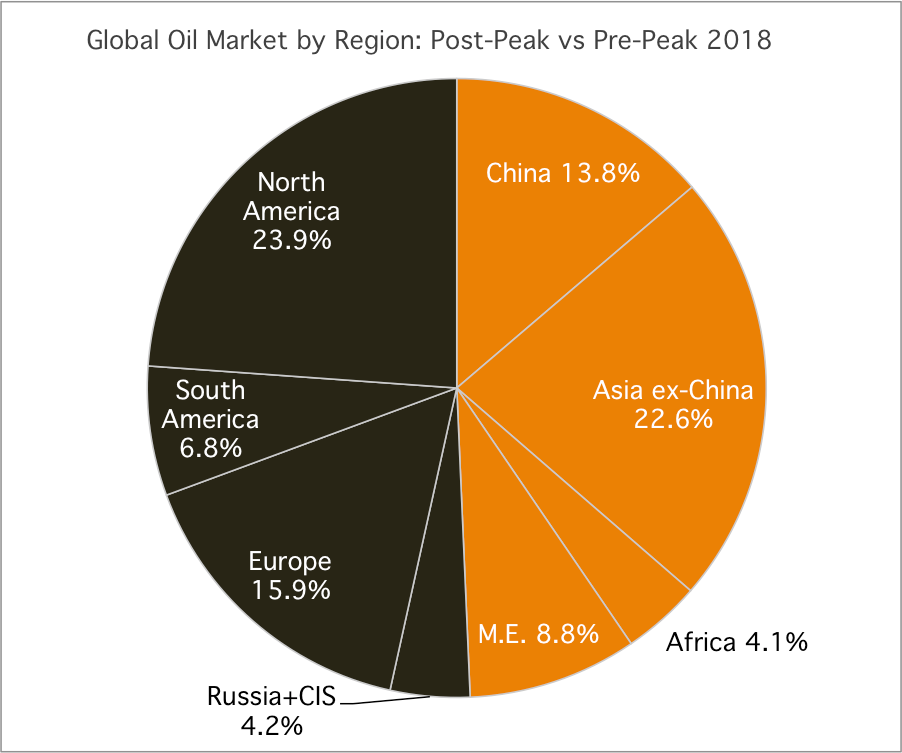

One very simple idea that many seem not to have fully absorbed is that China is the epicenter now of all rates of change in global oil demand. Half the world is either recently past peak demand, or well past peak demand. Worse, for the oil industry, is that Asia ex-China, Africa, and the Middle East—which have all yet to reach peak demand—grew poorly last year. Let’s take a look at another chart that originally appeared in Oil Fall, and which has now been updated with the most recent data.

All the regions on the left side of the chart are past peak demand. The right side, yet to reach peak demand. But oil demand in Africa and the Middle East (ME) actually fell last year. And while China’s oil demand grew, Asia ex-China grew by just 1.3%. That means that Asia ex-China grew by roughly the same as global average, of 1.22%. Not very impressive for a large region long expected to grow oil demand much higher than the global average.

That’s why China, which currently takes 13.8% of the global market, is so important. Half the world is applying no pressure at all on oil demand. Africa and the Middle East are underperforming, and Asia ex-China is not outperforming. Accordingly, when China’s oil demand growth decelerates as it is doing now, that change alone delivers the bulk of the impact to the global oil market. I will stay with my forecast from February, that global oil demand growth will be as low as 0.7 mbpd this year. And importantly, that $60 oil is not sustainable with such low demand growth.

Meanwhile, on the macro front, global readings of manufacturing have fallen to multi-year lows. I call this Ricardo’s Revenge: what “seems” like small constraints placed on global trade through tariffs, actually morphs into broader weakness as the purchasing power of workers in trading partner countries hits global demand for everything, including your own products.

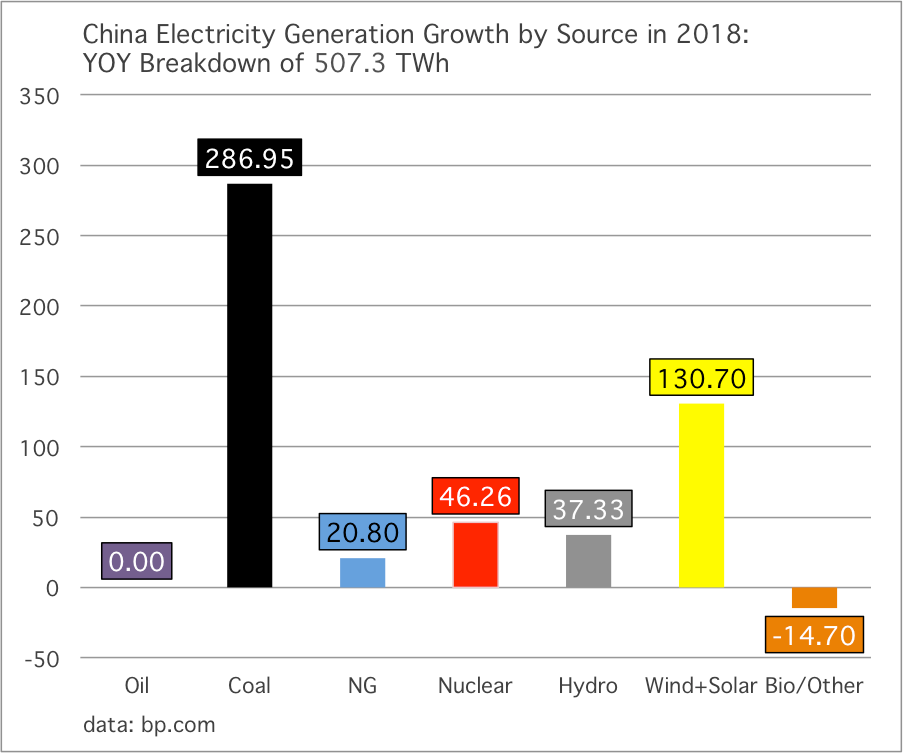

Growth of electricity from wind and solar globally in 2018 overperformed the Oil Fall forecast, reaching 6.97% market share of all power generation, up from the 6.13% estimate published last year. Better still, even though coal use grew in China and India, both countries saw their combined wind and solar share also outperform the Oil Fall estimate, taking a 5.83% share in India, and 7.64% share in China! Finally, California remains the superstar, with wind+solar taking 21.23% of its electricity consumption. The Golden State is zoom, zoom, zooming towards 25%.

Why this matters: because regardless of how many new EV China, the US, or California puts on the road, all three domains are growing their combined wind and solar generation far faster than new demand for power, from EV.

To give one example, China put a fresh 1.825 million EV on the road last year. Being extremely overgenerous, this represents about 6.4 TWh of new electricity demand. (Again, I must emphasize that is an over-safe, overestimate of annual power demand from new, on-road EV, using a factor of 3500 kWh per vehicle). Now let’s ask the question: how much new electricity, just from wind and solar, did China create last year? Answer: 130.7 TWh, 20 times more electricity than required to serve new EV registrations.

The cost of energy transition continues to fall, and the trends described in the April newsletter, We’ve Got Tools, march onward. For domains like California, rich in both sunshine and wind resources—and historically more vulnerable to higher oil prices and smog—the gains to be harvested from a faster transition to renewables can’t come soon enough. In Oil Fall, I speculate that a cleaner Los Angeles, already on course in time for the 2028 Olympics, will emerge as a highly transformed city by the year 2040. Much of the impact will land on real estate prices, as the San Fernando Valley (yes, Frank Zappa’s San Fernando Valley, long the butt of jokes and the minor pop hit, Valley Girl) is resurrected, and becomes once again a desirable place to live—much as it was in the early part of the 20th century. Indeed, the third part of Oil Fall, Waste Crash, sketches the rough outlines of a future Los Angeles as the energy transition accelerates: myriad rail and BRT lines running into the Valley; a crash of ICE vehicles on the road in LA County more generally; and the end of growth in personal car ownership. Interestingly, LA County registered vehicles, which were already growing tepidly, actually flattened out last year.

Meanwhile, California vehicle sales fell by 5% in Q1 2019, a steeper decline than was seen nationally. Just as in China, I have dialed back the forecast for EV unit sales growth in California but from a market share view it really doesn’t matter, because the total market is falling more quickly. With the denominator moving downward, EV as the numerator can triumph. Some might say my market share figures are still a bit aggressive. But consider: EV already hit nearly 8% last year. The 11.3% share forecasted for this year is largely due to ICE vehicles getting hit hard. And this continues next year as well. For readers of Oil Fall, I wish to confirm the main case thesis originally offered: by the time global car markets are set to recover next year, or by 2021, it will be too late for ICE to compete against EV. ICE sales have peaked in China. And they have peaked in California.

Finally, let’s ponder US oil demand in light of an economic slowdown, and a more gentle decline in US vehicle sales. Here in 2019, total US oil demand is now flat through the first 5 months of the year. US gasoline demand, meanwhile, is putting in a third year of no-growth. No market better illustrates the trend than California, and California has now put in a second, lower peak of gasoline demand in 2017, just below the slightly higher peak of 2005.

Let’s finish today’s letter with a flourish: US road fuel demand has also now peaked a second time, at a slightly lower level. From here, given slower economic growth, and the surge of EV choice and affordability that is coming to the US market later this year and next, US oil demand is going to start printing as a subtraction from any hopes that global oil demand can grow much in the years ahead. Recall that even BP forecasts that 78% of total oil demand growth from 2017 to 2040 is done by the year 2025.

—Gregor Macdonald, editor of The Gregor Letter, and Gregor.us

The Gregor Letter is a companion to TerraJoule Publishing, whose current release is Oil Fall. If you've not had a chance to read the Oil Fall series, the single title just published in December and you are strongly encouraged to read it. Just hit the picture below.