Power Signals

Tuesday 27 August 2019

The Gregor Letter is on a lighter schedule here at the end of summer. But there are a couple of readings worth mentioning before I return in September. Until then, I’ll be away from my desk and spending as much time as possible here in Portland, on my bike. —GM

Mark Lewis and the team at BNP Paribas have written up a wonderful report covering wind and solar’s competitive edge, against oil. Wells, Wires, and Wheels (opens to PDF) analyzes how much transportation energy a theoretical $100 billion, put to work today, would ultimately generate by following either the oil path, or the wind and solar path. A particularly nice observation contained therein is that today’s oil extraction and delivery infrastructure partly shields us from the embedded losses in that system, through the advantages of incumbency. But this advantage too is starting to erode. Overall, I see the report as a companion to the Oil Fall series: a different set of authors have come up with a different set of framings, many of them clever, but the target is the same.

Old energy infrastructure and the fossil fuel systems they support increasingly run at a loss. That’s the message of Oil Fall, the BNP Paribas report, and it’s also the message coming through directly from power generation asset owners. Next month, I’ve got reported pieces coming out that peer into the financial details of both the Klamath River Dam Removal project, and also the Northern Indiana Public Service Company’s decision to shutter all of its existing coal assets, replacing them with a combination of wind, solar, and storage. In both cases—and this is crucial to understand—the cost to shutdown existing assets is not only lower than the cost to keep them running, but, the utilities in each case will be able to replace the asset closures with new infrastructure while still delivering savings to customers.

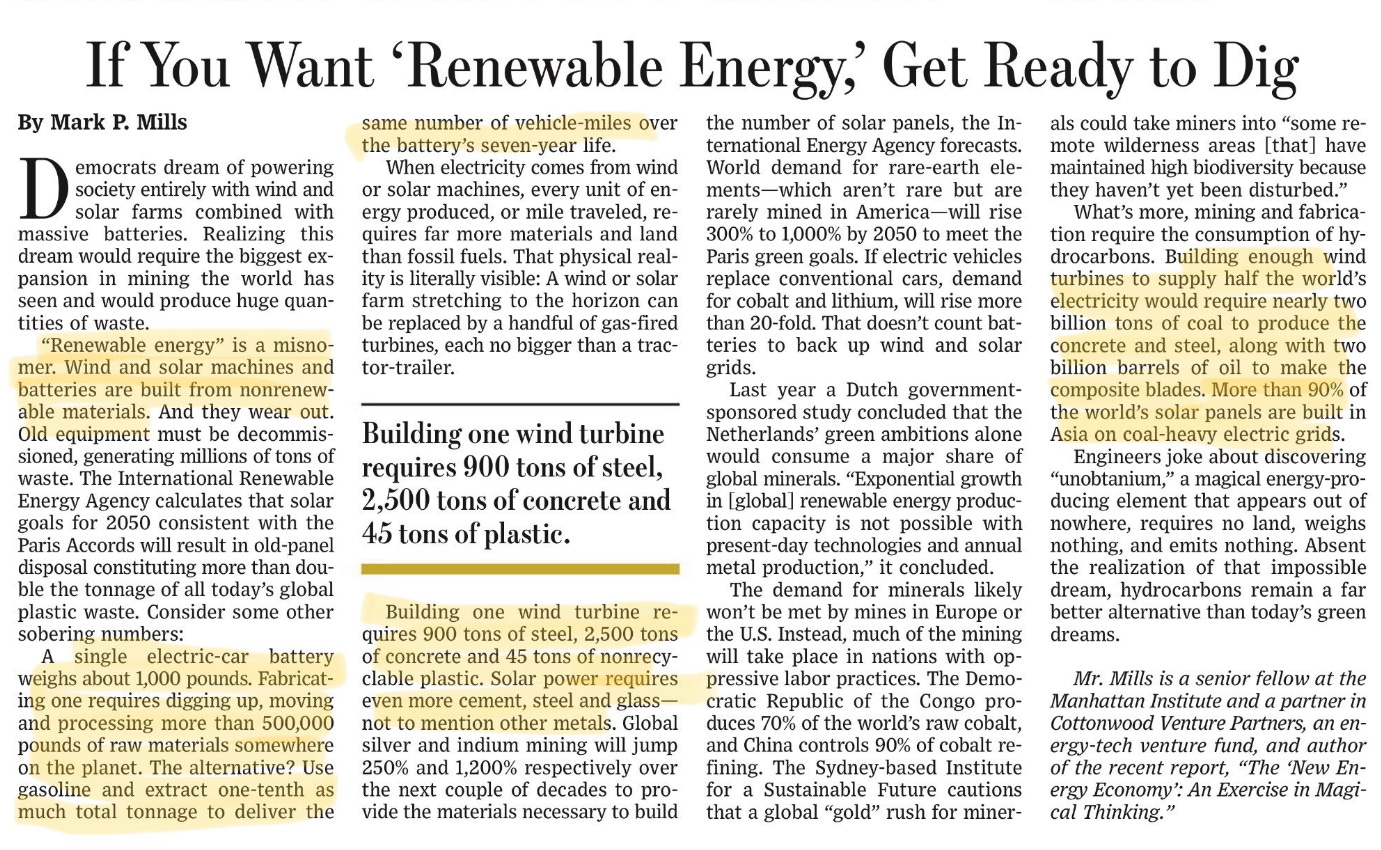

The bullshit detector rang loudly earlier this month, when Mark Mills of the Manhattan Institute published a ridiculous Op-Ed in the WSJ, claiming a steep and onerous call on natural resources to build out clean energy. No one credible anywhere claims that rapid deployment of wind, solar, and battery storage does not represent a new call on resources. Rather, it’s simply that price is a reasonably good proxy for why that new call on resources is significantly lower than trying to maintain investment in the existing fossil fuel system. What Mills doesn’t address (because, of course) is that electricity from wind and solar is generated at extremely low operational costs after a one time capital investment. The industry term, levelized cost of energy (LCOE), does more than an adequate job of making these comparisons. Because the Op-Ed is behind a paywall, I found an internet copy for you to read, below. But don’t feel obligated to waste your time doing so, unless for entertainment purposes only. A final point: Mills willfully represents, and perhaps genuinely doesn’t understand, the term renewable.

Utilities have come through a rough decade, but what if they are ready to lead again in the energy sector? Liam Denning and Nathaniel Bullard of Bloomberg, here in 2019, have considered the signal coming through from the woeful underperformance of oil and gas equities, and discerned that growth prospects now look better in the power sector. Recall that wind and solar began their ascent in Europe—not this decade, but in the previous—and this initially slammed the European utility sector bogged down as it was with nuclear, gas, and coal assets. But a decade of change both in the EU and the US now sees most utilities adopting, owning, and operating new power assets led by wind, solar, and storage. This strikes me as a classic first you get hurt, then you get mad story.

—Gregor Macdonald, editor of The Gregor Letter, and Gregor.us

The Gregor Letter is a companion to TerraJoule Publishing, whose current release is Oil Fall. If you've not had a chance to read the Oil Fall series, the single title just published in December and you are strongly encouraged to read it. Just hit the picture below.