Stocks and Flows

Monday 15 June 2026

As the Iran war winds down, a story worth telling is how, these past several months, we managed to escape an even more dramatic oil price spike. Helpfully, the story and its explanation are not that complicated. Saudi Arabia’s historic investment in bicoastal export capacity tells one part of the tale, and China’s gargantuan oil reserves, steadily built up over years, tells the other. We can probably add in a dash of real-time demand destruction, as global consumers not only reacted to the initial increase in oil prices but anticipated a lengthy period of elevated prices. True, oil did spike and prices remain elevated. But we never suffered a systemic seize-up price like the $200 and even $300 levels many feared. As Cold Eye Earth goes to press (on the same weekend Iran and the U.S. are supposedly about to sign a peace deal), both WTI and Brent oil are back under $90 a barrel.

For years now, oil has suffered from a sustained period of slow demand growth, and technology advancement that keeps reliably pulling down the cost of creating the marginal barrel. This setup has persisted for years, and it is the very best explanation for why energy equities have been such a poor investment (ex temporary price spikes and geopolitical dramas). This new topography for oil, where nothing happens for a long time, a brief interruption arrives, and then oil returns to another lengthy and listless period, says a lot about oil’s overall prospects and fortunes. It’s not great.

The fact that China was able to amass over years a 1.4 billion barrel reserve mountain without disturbing the price of oil also indicates how absolutely lousy the oil business has become, as extraction costs have risen along with inflation but the price of oil itself has been tame, and actually quite cheap. Twenty years ago, Americans were paying on average $66 for a barrel of oil, which after adjusting for inflation would be about $109 today. Stop here and consider the implication: Our “energy crisis price of oil” during the 2026 Iran war this spring took oil prices roughly to the same average recorded for all of benign, humdrum 2006. Again, Cold Eye Earth has been pointing out for about a year now that oil and gas prices today, after adjusting for inflation, are akin to walking into a grocery store and seeing that beef prices are the same as they were two decades ago. Now that oil has returned to below $90 a barrel, it’s once again dirt cheap when compared with wages.

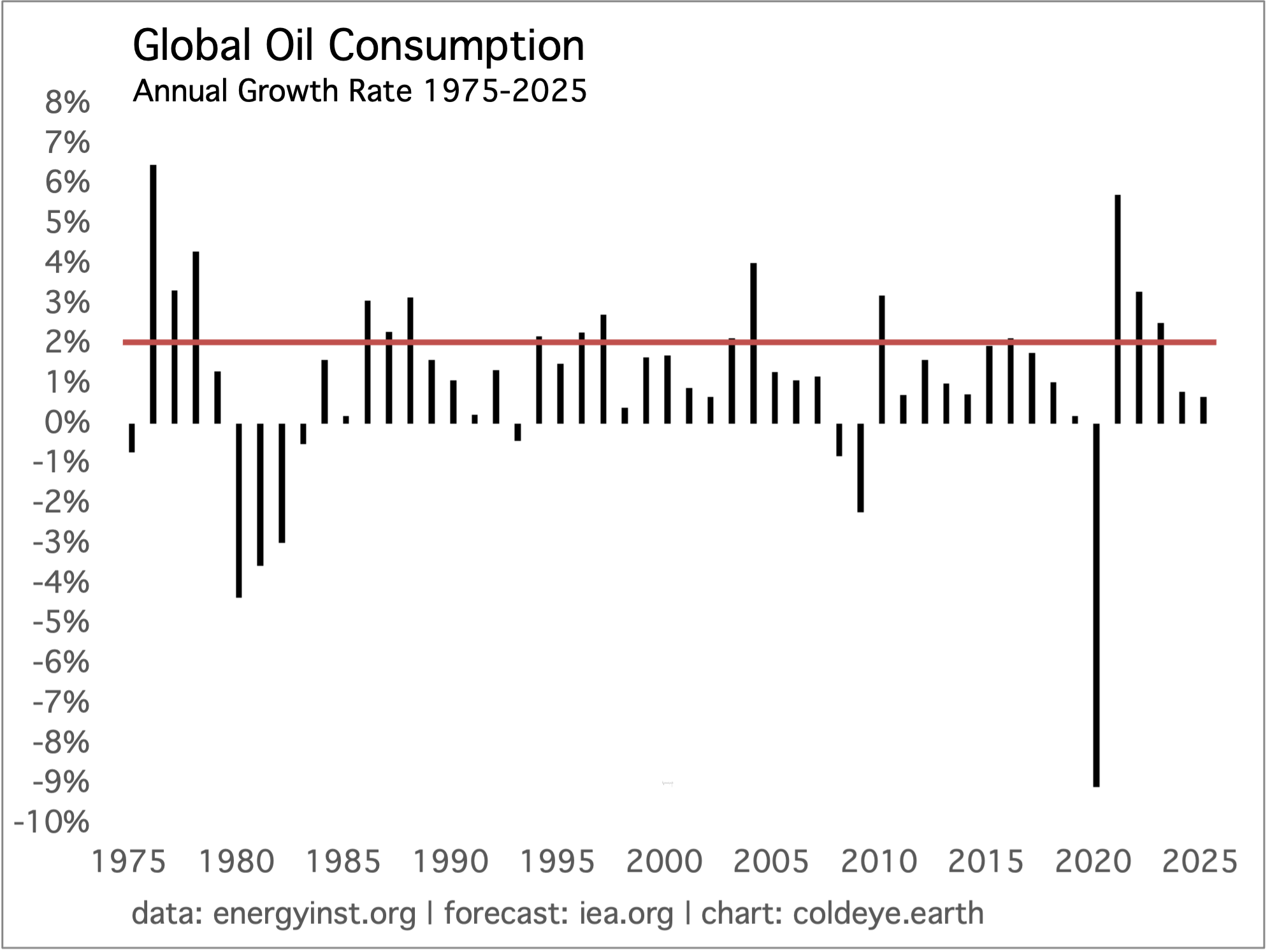

Another perspective worth considering is that, since 2005, global oil demand has either reached or exceeded 2% growth only five times. And of those five instances, at least two of those years have to be considered outlier, rebound years, in which the global economy roared back and oil demand crawled out of a deep hole. It sure is easy to post a “growth” number when you’re starting from the depths.

A number of longtime oil bulls have been frustrated for years about oil’s sluggish performance since the go-go days of 2002–2008. But when you convert to a regime that sees global oil demand rising, at best, at about 1.0% per year, you have to expect that the futures market will see the combination of weak demand growth, steady supply growth, and the reserve-building those conditions foster. If you are familiar with the concept of stocks and flows, what has happened to the oil market since the great recession is that both stocks and flows increased. By how much? This is how much: The world mostly lost the Strait of Hormuz for 90+ days and the price of oil never reached the boiling point!

What comes next? A continuation of the past decade: investors baffled that quality names like Occidental Petroleum are dead money and can’t get off the ground, stocks return to a building phase not just in China but in the OECD, and the relentless ebb of oil demand growth as more of the world’s transportation system electrifies. Oh, and a kicker: While the Saudis were indeed quite correct over a decade ago when they added, at great expense, bicoastal export capacity, we must now acknowledge that it was China, not Saudi, that assumed the role of The Central Bank of Oil during this most recent energy disruption. Assuming they rebuild those stocks over the next few years, we are obligated to keep extending that title to China.

Breaking news on Sunday afternoon, June 14: Iran and the U.S. agreed to their peace deal.

The strategic importance of oil is fading, while that of artificial intelligence is rising. Over the weekend, the Trump administration placed an export ban on the latest AI model from Anthropic, shocking investors across the AI community. As is typical with the current government, everything about the sudden announcement felt rushed, ad hoc, and possibly petty and vengeful. David Sachs, the AI czar, tried to calm the waters over the weekend, saying both sides would almost certainly come up with a compromise. But then Secretary of Defense Pete Hegseth let the cat out of the bag with a dismissive post on X that understandably made many conclude that, yes, this was more about vengeance than any scholarly analysis of Anthropic’s model.

Keep reading with a 7-day free trial

Subscribe to Cold Eye Earth to keep reading this post and get 7 days of free access to the full post archives.