Supply Lines II

Monday 11 October 2021 | Part II

European fossil fuel consumption has been in downtrend for over a decade. This long term decline is a useful fact in understanding today’s energy supply crunch on the continent. Popularly described as a failure of energy policy—or even more incorrectly, a geologically constrained global shortage—European energy supply is struggling instead in the face of logistical deliveries, politically driven supply constraints engineered by Russia, and the same post-pandemic throughput challenges that are affecting everything on the planet from kitchen goods to semiconductors.

Fossil fuel demand declines interrupt the normal flow of investment which fosters their expansion, eventually resulting in periods of supply-chain illiquidity. Capitalist driven industrialism is optimized to serve growth. And in Europe, growth is long since over for fossil fuels. It is exceptionally easy to predict, for example, that the same throughput challenges seen today in Europe’s fossil fuel market will soon begin to affect its incumbent automobile industry, and all the infrastructure that serves legacy ICE vehicles. Just as we’ve seen in China, European sales growth of ICE vehicles is in a state of collapse. Indeed, Europe’s EV market is leaping ahead now, with plug-in market share bolting last year above 10%. This irrevocable pivot from the ICE to the EV platform will be understood readily by anyone with business experience who has watched their market share slip away slowly, and then all at once. EV are now totally in control in two out of three of the world’s largest car markets. Will there be petrol shortages in the future in Europe? Count on it. How about auto parts shortages, a dearth of ICE vehicle skilled labor, a contraction of fueling capabilities, and fuel-tax revenue declines? All those, too.

Europe therefore lives in a state of fossil fuel dependency, rather than fossil fuel growth, while concurrently mounting a new, low carbon energy system built on wind and solar power. There were bound to be gaps, in the way the two systems interact with each other. Now that wind and solar are approaching 20% of continental electricity supply, the system in its current state was going to be vulnerable to either a period of lower wind output or a phase of natural gas supply constraints. At the moment, Europe is having to face both at the same time. But notice the rather predictable explanations and accusations from the usual voices. When the Texas Railroad Commission blamed the Lone Star state's wintertime energy disaster on "windmills" everyone immediately understood the self-serving absurdity of that conclusion. Would there be any sort of continental power supply problem right now without dependency on natural gas from Russia having revealed itself to be a strategic vulnerability? Of course not.

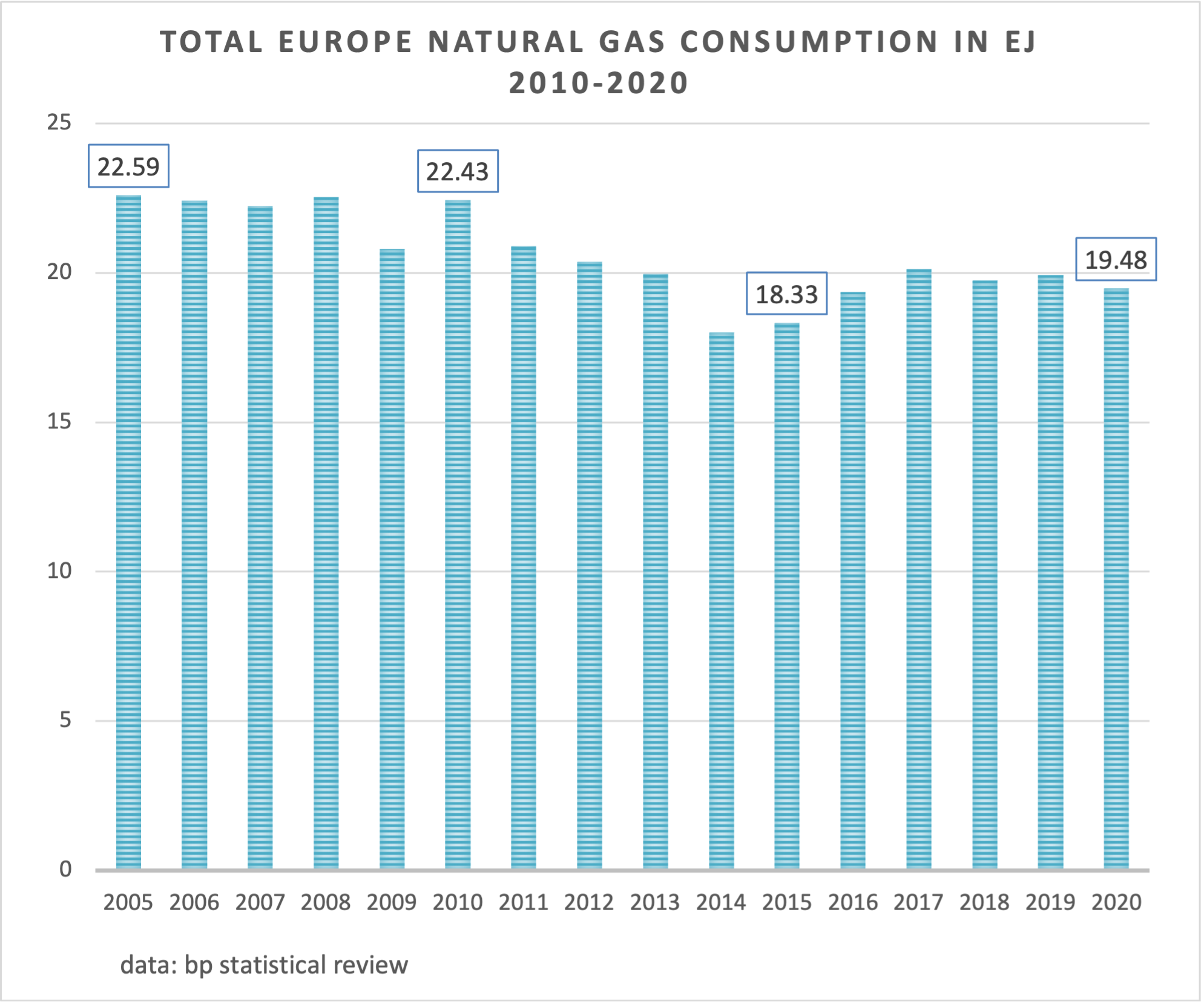

Natural gas consumption in Europe has also been in a downtrend, though at a gentler pace, for over a decade. Contrast this trend with the US, where natural gas consumption has risen an incredible 25% over the same period, along with significant investment in pipelines, extraction, and natural gas fired powerplant construction. Indeed, natural gas adoption can be thought of as a major global trend over the past decade. But not in Europe. Globally, natural gas consumption is up 21% since 2010. But in Europe, consumption is down over 13% in the same period. (Because 2020 will always be an outlier year, it’s responsible to also note the European natural gas consumption decline through 2019, at 11.2%). The message from Europe to the natural gas industry is clear: we will generally be using less natural gas forever, from this point forward.

With fossil fuel demand growth now very much over in Europe, all conversations and especially passionate disagreements must be understood as taking place amidst this decline. Unleash your theory into the boxing ring, if you must, but the fight that remains is over an ever contracting market for petrol and gas, a systemic change that is hardly recent or new. That doesn’t mean there are no valid criticisms of how Europe is building its low carbon system, alongside the legacy system. Governments clearly should have been incentivizing storage deployment as aggressively, or more aggressively than their historical support for new solar and wind generation. You can see how it happened however. After wind and solar no longer needed as much policy support, the learning rate got to work and new zero-carbon generation exploded higher all on its own—offshore wind especially.

But Europe should have got going earlier on deployment of storage. That probably happens now, and not only because of the imbalances currently exposed by natural gas dependency. Indeed, the ascent of EV are going to start placing a stronger marginal call on continental power supply. Emphasis on marginal, however. Collectively, EV do not currently, and will not in the future, place any unmanageable demand call on global powergrids. And every EV takes at least 60% less energy to go one mile, compared to an ICE vehicle. But if you put a fresh one million EV on the road and impute, say, an annual power consumption rate of 3500 kWh per vehicle (for comparison, one imputes 4000 kWh for every vehicle based in the US), then you will need to create a fresh 3.5 TWh of electricity supply. For a region like Europe that generated 3871 TWh in 2020, that is both trivial, yet important nevertheless. Where do markets take place? At the margin. If Europe starts consistently adding a fresh 1%, then 2% and 3% and more to electricity demand from new EV hitting the road each year, then yes, Europe will need to create that supply and the market will feel it should Europe fail to do so.

The story of Europe therefore is one of transmission lines pushing out the pipelines. Advocates of renewables should be sober however about the growing pains of energy transition. And especially about a dynamic we’ll see more often: as renewables scale they actually become increasingly dependent, at the margin, to the availability of natural gas and coal. This is not a volumetric observation. Rather, it’s an observation that tight conditions in a large system can propagate quickly and disruptively.

Data Notes: the category displayed here is the “Total Europe” data series from BP Statistical Review which is a broader representation of the continent that includes the EU, the United Kingdom (no longer part of the EU) and countries like Ukraine and Turkey. For comparison, in the series that contains only the EU the natural gas decline of 2005-2020 was gentler at -9.2% compared to -13.8% in Total Europe, while the fossil fuel decline was nearly the same at -26.7% in the EU versus -26.2% in Total Europe. Perhaps we could say: when it comes to scrutinizing policies specifically, it might be better to track data series for EU members only, even though that category no longer includes the UK. But for population, energy demand, industrial growth, and automobile demand, the broader category is preferred.

The recent California oil spill is depressing on a number of levels. The initial reaction, are we still doing this, really? is perfectly stated. But it’s also a reminder that California still engages climate policy along every possible avenue except the one that would make for a direct hit on the existing ICE fleet. The Golden State has a robust set of incentives and rulemaking that touches buildings, solar at both the domestic and utility scale, and promotes EV adoption. But with only a few micro exceptions, driving in California is unmetered. That’s crazy. The state is still essentially running the road system as it was in the 1950’s. Before we get to that data, a requisite and well justified joke about oil spills:

Here’s the bet California is making: that petrol consumption will eventually go into decline through the adoption of EV, without any road charges or tolling that would place direct pressure on existing ICE cars. Politically, you can see why even in a deep blue state, Sacramento has taken that route. But has this particular bet paid off? Possibly. Now that EV have reached at least a 10% share of the state’s car market, and especially given that California’s tech companies are on the leading edge of new work-from-home arrangements, petrol demand in 2021 is struggling to recover to the plateau seen over the past decade. The Gregor Letter has made this point several times now, when it comes to global road fuel demand: EV adoption strength is super impressive and accelerating, but is still not sufficient as a single factor to tip global petrol demand into decline. But, in combination with post-pandemic changes to commuting, the two factors together have likely helped to mark a peak in demand.

Road fuel demand growth in China flattened after the country reached the peak of ICE sales in 2017. Relatedly, it’s never a bad time to remind readers of the three conditions possible in energy demand: when demand is growing; when demand is neither growing nor falling; and when demand is falling. Most people skip or fail to absorb the meaning of the second condition, intuiting that demand must be either rising or falling. And that’s an error, because the transition to flat road fuel demand in China, if it holds, is a very big deal. According to data from the IEA, combined gasoline and diesel/gas oil demand was growing at a healthy annual clip, roughly 3% - 5% per year, in the years leading up to the EV/ICE crossover in 2017.

As readers know from data presented in Part I of this two part post, ICE vehicle sales growth in China is in collapse, falling from over 28 million in 2017 and on course to come in below 23 million units this year as EV sales skyrocket in both absolute and market share terms. What to watch for in the conversation: with EV now busting through 10% market share in both China and Europe rather suddenly, most will be entirely unaware of this acceleration as they impulsively argue against EV. And there is no shortage of poorly constructed, negative analysis of EV more generally, even as they storm the market. See this dismantling of the latest effort from the FT.

You are reading the second of a two-part free post from The Gregor Letter. Part I published last Monday, 4 October. If you are still carrying a free subscription to the letter, please consider subscribing. Here’s why: there are very few free posts throughout the year. To learn more, see the About section. Many thanks as always to the international institutions, agencies, and investment professionals who rely on the letter for its energy and climate analysis.

• News briefs • Extreme heat exposure in urban areas has tripled since the 1980’s. The data and research comes from a study of over 13,000 cities worldwide. • The mega-drought in the US West continues to hit hydropower production very hard, with loss estimates continuing to climb. The EIA in late September forecast a 14% decline this year in output. • Under the assumption that global solar will continue to expand to the year 2050 and beyond, a significant increase in global glass production will be necessary. The study comes from the Fraunhofer Institute. Coverage at PV Magazine, and the original paper at Energy and Environmental Science. • Lithium carbonate prices have hit new all time highs, and Benchmark Minerals Intelligence is forecasting the market gets even tighter next year. • Europe’s natural gas supply problem would be solved more quickly if Russia was treated less as an adversary, says its ambassador to the EU. • Spain has ample reserves of rare earths, and tension is rising over their extraction. This is a pressure that will be increasingly felt in developed world domains.

There is no structural shortage in the global oil market, and any tightness could be resolved by OPEC in a day. The global oil market stood at 99.7 mbpd in 2019, and according to the IEA will recover to just 96.1 mbpd this year. That alone is a very significant shortfall—of demand. But when you add EIA’s estimate of OPEC spare capacity, at an enormous 7 mbpd, it’s simply unsupportable to argue there is any actual shortage in global oil supply. Indeed, even if you slightly increase 2021 oil demand, to say 97 mbpd, and reduce the OPEC spare capacity estimate to 5 mbpd, prices above $80 a barrel and any market perception of tightness could literally be solved in a single day, were OPEC to take action.

Reviewing previous forecasts is always a healthy exercise. Readers are encouraged to listen to my Bloomberg Odd Lots podcast interview from January of 2020, as I discuss the prospects for growth in wind, solar, and electric vehicles. Excerpt below, and direct link here.

The IMF has published a very broad, or perhaps an overly broad, accounting of the world’s subsidies to fossil fuels. The perspective could trigger some justified criticism as the IMF’s estimates expand way beyond direct subsidies to the industry. But the IMF’s accounting is a rather classic economic approach, and attempts to incorporate all the losses to the environment, and to people. Those are called externalities, and attempting to account for them is not exactly radical. But the subsidy the IMF needs to consider is the vast inventory of vehicle infrastructure, and the world’s unpriced highways and roads. Mark Lewis, formerly of BNP Paribas, wrote an excellent report about these issues in 2019 titled Wells, Wires and Wheels. (opens to PDF). Lewis’ main point: the world is currently set up to quickly and easily deliver a unit of petrol, oil, natural gas, and coal. And that confers an embedded price advantage to fossil fuels.

Energy transition slows demand for fossil fuels, sending a signal to investors to invest less in them, which leads to supply hiccups and price spikes, which will only accelerate energy transition. As the Op-Ed pages now proliferate with poorly constructed analysis of the “energy crisis,” it’s useful to consider that these price spikes are going to spur even more adoption of EV, wind, solar, and storage especially. This is not news, nor is it a surprise. It’s a dynamic that was predicted long ago, and now it’s coming true. The theoretical dispute over how to interpret this rather messy moment will animate the conversation for some time to come, as the legacy system of oil, natural gas, and coal contracts further while the new system expands. But the destination has visibility, is inevitable, and will steadily come into view this decade.

—Gregor Macdonald

The Gregor Letter is a companion to TerraJoule Publishing, whose current release is Oil Fall. If you've not had a chance to read the Oil Fall series, just hit the picture below.