The Big Miss

Monday 10 June 2024

Congestion pricing is increasingly popular around the world but in the United States its first steps may have just been crushed, by the governor of New York. With less than 30 days to go before a fee-for-use program was set to come into effect in lower Manhattan, Governor Hochul has placed a “pause” on the scheme’s implementation. This appears to be a way around the conventional legal structure which grants the right to make laws to legislatures, and the duty of executives to apply them. While a legal battle is likely to ensue, Hochul can probably burn up months in the gray area created by her decision. It’s unclear why, however, the governor has taken this course of action, or how it can possibly help her politically. The loudest voices in opposition to the program have largely come from neighboring residents of New Jersey and Connecticut, while passionate support is broad and deep among the millions who live in New York City.

The loss of nerve in the face of America’s first road-charging scheme is, however, another reminder of the crucial difference between stated and revealed preferences when it comes to taking action on emissions. The Democratic populations of the big, blue states like California, Illinois, and New York are overwhelmingly in favor of decarbonization policies. In this way, they are distinct from rural state populations that are either disinterested or hostile to such policies. But blue state populations find it much easier to state these preferences than to actually undertake them. As New York City’s scheme was about to get underway, Hochul—rightly or wrongly—must have decided she will get blowback after the program gets underway. In other words, even in New York City, Hochul faces what other blue state governors face, which is why congestion charging is not even on the table in all of America’s big blue cities like Portland, San Francisco, Los Angeles, Boston, Chicago, and Seattle.

There is also a potential knock-on effect that the New York decision may unleash. If it is already politically risky to even mention or propose congestion charging in the rest of the United States, the New York case may bring a kind of iron curtain down on the entire idea. And it’s important to note that many American cities have been “studying the idea” of road-charging for decades while taking no action whatsoever. So, it’s encouraging that the state and city of New York did in fact take the step, but it’s equally amazing the executive of the state has decided to bring the high drama of its disabling upon herself, and her administration.

As we know, transportation is now the top emitting sector in the United States so anyone who claims to be serious about fighting emissions must not just admit to the problem, but must do something about it. And what we find again and again is that the majority of Democratic voting populations across the United States are not serious about fighting emissions at all. Instead, they prefer to think they are. This is the inconvenient truth that many left-leaning writers who cover climate change would prefer to ignore. It’s so much easier to finger the open hostility to climate policy among the right than to admit that this huge deadweight from the left is also structural to our inability to make progress. And, the outlook is very dim. The only policy left standing in the US to reduce transport emissions is the adoption of electric vehicles. That single-bullet solution is deeply-flawed, of course, because of the length of time it takes to turn the fleet over. If your only solution is to electrify, then you are choosing to delay transportation sector emissions declines into next decade.

There are many tragedies here. A big one: the US has the power to finally kick oil consumption off a 20 year oscillating plateau (a great example of how long the condition of peak can endure, without any meaningful decline). Were the US to introduce such schemes across many cities, we would finally see petroleum use decline. That would send a shockwave through the oil market (already under pressure from overcapacity) and would shift the timeline of the oil age as the world’s number one oil consumer embarked on a new era. Well, it’s a nice thought, regardless.

The China peak emissions callers have returned once again, like a flock of migratory birds. The irony in all the zeal however is that even when China’s emissions do eventually peak, it will not necessarily usher in an era of declines. The world has produced multiple examples of peak consumption levels that carry on for years if not decades. Global coal consumption “peaked” in 2013/14 but limped along for seven years before going on to a new high. Total North America oil consumption peaked in 2005, yet declined just 6% by 2022, seventeen years later. How encouraged would you be to read the hundredth article about imminent, peak emissions in China, if it was equally projected that emissions will subsequently fall by just two to three 10ths of a percentage point, each year thereafter?

What are the China peak emissions callers offering? Not much. Just the same arguments about the astonishing level of clean energy newbuild. Again, we don’t need any new analysis or more pom-pom waving about the titanic deployment of wind and solar in China. That story, and its future projections of growth, is extremely encouraging—but not exactly a mystery. What we need is analysis of consumption, and economic growth. One thought on that: it was generally after industrialism peaked in the US , not before, that the country transitioned to becoming a consumer economy, and saw a great upswing in US energy consumption mostly after WW2. While China’s industrial economy has not yet peaked it is certainly maturing, and the wealth created over the past 40 years in China is more than sufficient for China to play out similarly.

While oil in China will not, in the opinion of Cold Eye Earth, be the growth fuel of choice as it was in the US, it’s a certainty that electricity and its various inputs will be the platform that guides China’s economy—as it has done for decades. Which means that all the renewables newbuild must not only cover marginal, annual growth but it must eat into the existing base, largely running on coal. We’re just not there yet.

The Energy Institute’s Statistical Review of World Energy comes out later in the month and it’s worthwhile to offer a preview. First, global emissions rose again last year, and the main culprit was China and in particular (surprise!) coal in China and India. We know this from the first release of 2023 analysis from the IEA. Unfortunately, 1.1% annual growth of emissions is a rate that suggests far too much compounding if maintained, and confirms that while clean energy growth is terrific, the main problem is underlying system expansion.

The next item to look for is natural gas consumption in Europe. The energy shock of 2022 triggered a massive deployment of heat pumps which tailed off some in 2023. The two year comparison of natural gas consumption will be instructive. Overall, however, all three fossil fuels are in decline in Europe so the game now is to see how well the EU can keep the decline rate going.

The most important data in the report will cover global electricity and the ongoing effort to cover all marginal power system growth with clean energy. Three numbers matter: total generation growth of wind and solar; total generation growth of fossil fuel driven power; and most important of all, total system growth and its rate. It’s this latter number that will give us the most information about the prospect that clean power can finally catch up to the system, and overtake it.

The EI Statistical Review will be released on Thursday 20 June.

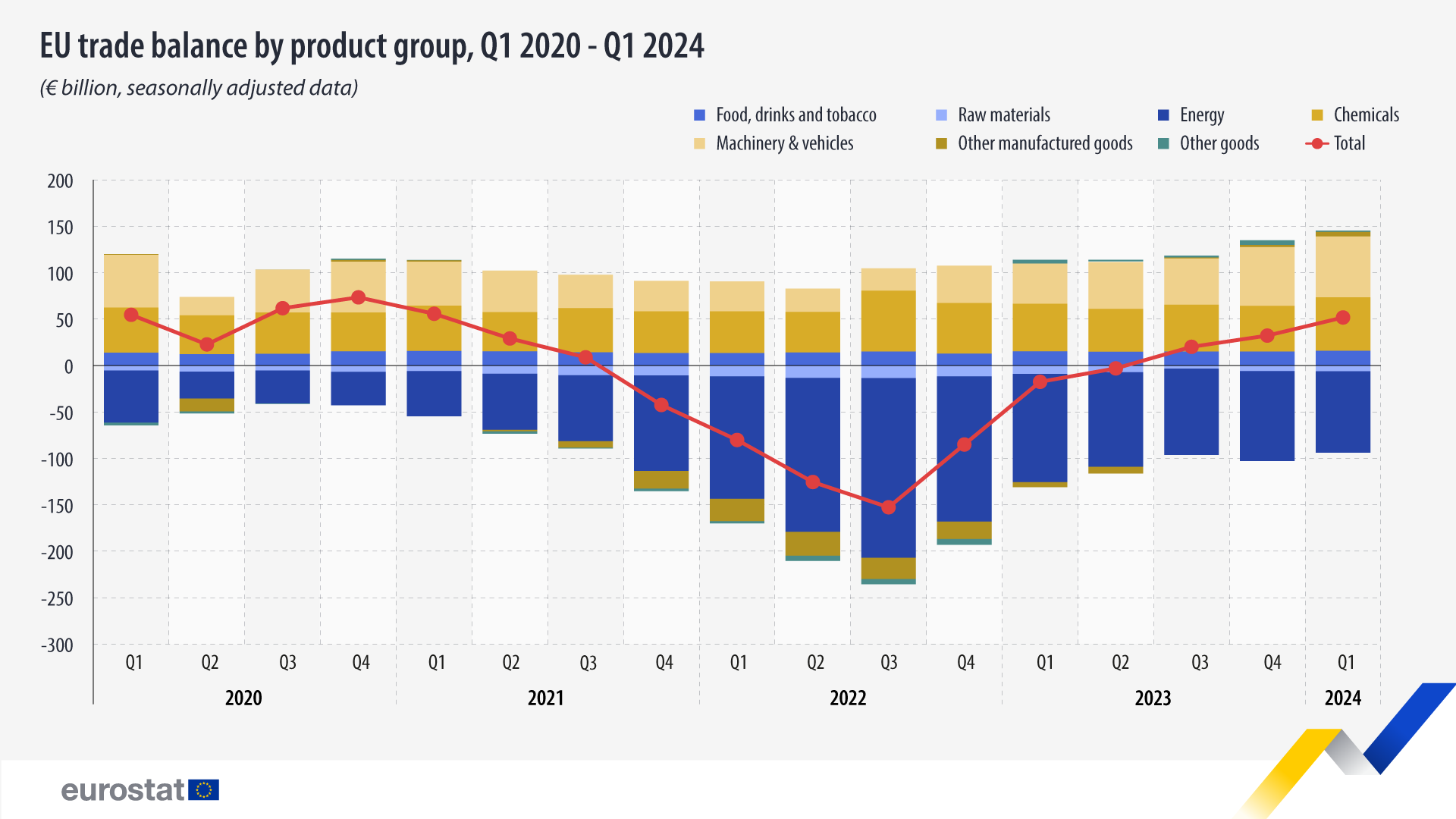

Europe’s industrial base is now recovering, two years after the continent’s energy shock. There’s been no shortage of I-told-you-so heckling since 2022, castigating the EU and Germany in particular for having built up a dependency on imported energy—natural gas mainly, from Russia. But dependence on foreign energy supply has been a common condition globally since the 20th century for most regions and there was nothing irrational about utilizing cheap Russian gas while it lasted. Meanwhile, the EU has been furiously deploying clean energy, and pressing onward with its efficiency programs. The result? Energy dependent sectors like chemicals are thriving again, and exports are recovering nicely, as can be seen in this Eurostat chart.

The data comes from the EU Commission, in a blog post titled EU trade in goods records a growing surplus which notes that, despite energy and raw materials deficits, exports of machinery, food and beverages, other manufactured goods and machinery are all pushing the trade balance back into surplus for the third quarter in a row. Naysayers and doomers typically only see the dependency side of energy supply, forgetting that human civilization has forever used energy to transform goods and services into profitable undertakings. Yes, there are price levels that restrict this ageless process should scarcity take energy costs higher. But this too is an old story. To be honest, the EU has handled the 2022 crisis extremely well.

As Nvidia now emerges as the most valuable company in the world, the wealth effect from its quickly expanding market valuation has only just begun to flow. This Spring, for example, ground broke on a new $200 million computing and research center at Oregon State University, a gift from Nvidia’s co-founder Jen-Hsun (Jenson) Huang, who obtained his undergraduate degree in engineering from the school. Meanwhile, on the other side of the country, another Nvidia co-founder, Curtis Priem, continues to unload his fortune onto his alma mater, Rensselaer Polytechnic Institute. Global data center deployment, and the AI revolution that will drive it, is going to generate economic impacts far beyond the mere energy requirements to fund that growth.

The US presidential race has tightened to even, since the conviction of candidate Trump on business records and election law violations. The recent movement in the polls, which now has Biden and Trump evenly matched both at the national level and in the battleground states, has apparently come about largely through Biden voters “starting to come home” as the GOP nominee is now officially a felon. If we ask the simple question—could a candidate’s guilty verdict affect the outcome of a close race?—the answer so far appears to be a rather conventional and unsurprising, “yes.” As CNN’s Harry Enten put it: The majority (not all) of the evidence suggests a bump for Biden post-Trump conviction... Not a large bump... But 1 to 2 points in a tight race ain't nothing.

In the view of Cold Eye Earth, this nudges the November election back towards an outcome that is also conventional. For example, former Vice President Pence, and former Speaker of the House Paul Ryan, have announced they will not vote for Trump. Since 2016, those kinds of old-school defections never mattered. They probably matter now. It’s simply not going to be possible for many older Republicans to vote for a felon, and one of the ways these voters may ease their dilemma is to simply stay home.

The move in the polls (for example, the recent CBS/YouGov poll) suggests that the vast majority of Americans, as so often is the case, have long since made up their mind. With just five months to go, therefore, it’s the action at the thin margins of the race that matter, and those are historically quite sensitive to news flow. It bears remembering that Trump is also still facing multiple indictments on far more serious charges, and his conviction in the recent case likely makes those charges seem more credible.

What might the November electoral map look like this autumn? We begin as always with the 2020 result projected on the 2024 map, and ask the age-old question: which states if any will flip towards the other candidate? As you look at the first map, let’s remember that Biden’s three narrowest victories occurred in states by margins less than 1.00%. So no matter who Biden was facing in 2024, it was always going to be the case that these three states would be risky:

Georgia 0.24%

Arizona 0.31%

Wisconsin 0.63%

Unfortunately, if Biden did lose all three of GA, AZ, and WI this year he would lose the election. A variation: Biden could lose both GA and AZ but if he lost Nevada rather than Wisconsin he could still win the presidency with the bare minimum of 270 electoral votes. Relatedly, this risk also expresses itself in the possibility that the electoral college could wind up in a tie, at 269-269 and all that would be required is for Biden, in this variation, to lose a single electoral vote either in Maine or Nebraska—which you can see on the map of those states. For readers outside the US who may not be familiar, the US has indeed seen one previous electoral college tie in the year 1800, and you can read about the procedure to “cure” such a tie in this wrap-up of that year’s election.

Trump’s 2020 electoral vote loss by contrast was composed of far larger margins in the states that he won, and that includes the three states where Biden lost, but was most competitive. They are:

Texas 5.58%

Florida 3.36%

N.C. 1.35%

What are the prospects that Biden could put one of these states into his own column, in 2024? When you look at the margins and you consider the cultures of these states, the chances Biden could grab one of these seems remote. There’s long been a dream, for example, that Texas could turn blue. But that demographic hope still has not come true, and it seems highly unlikely Biden could flip Texas. He has no edge.

But Florida is different, this time. The main reason is the abortion issue, which will be on the ballot this November and which has been super-charged for voters through a recent ban on abortions in the state for pregnancies longer than 6 weeks. That 3.36% victory margin that Trump enjoyed in 2020 could be eroded first by his felony conviction but especially by the abortion vote, which is going to drive alot of Democrats to the polls. Important note: the Florida Democratic Party has historically been disorganized but the abortion issue—which continues to poll horribly for Republicans—will overwhelm the party’s historical ineptitude.

Which then leaves us with North Carolina. Last won by Obama in 2008, the shift leftward many expected over the past decade has indeed taken place, with successive elections in the state becoming tighter between the two parties. Importantly, Trump’s margin of victory there in 2016 of 3.66% contracted greatly in 2020, down to just 1.35%. There’s no reason to believe that couldn’t shrink by a similar amount this year, and hand Biden a very thin victory.

Accordingly, it makes sense to consider Trump losing two states he won last time, and Biden losing three. Here is what the map would look like with those five states now unlocked from their 2020 results.

Notice that while it would be far easier for Trump to win any of those three Biden states of GA, AZ, WI, the potential loss of Florida and or North Carolina for Trump are deal breakers, especially Florida with its rich collection of 30 EV. Put another way, it’s amazing that Trump won Florida last time, and still could not eke out an EV win. Were Biden to actually win Florida, it’s a near certainty that victory would tie up the election on his behalf.

The Trump indictments still outstanding, the felony conviction, and the huge money judgments in the defamation and business fraud cases have not hurt Trump with his base. But he can’t win on his base alone. The problem these legal troubles present for Trump therefore occur in the following three voting segments: democratic voters who have soured on Biden and are once again finding a reason to return to the fold; the tranche of independent swing-voters found in each state; and older, educated Republicans.

Cold Eye Earth concludes that we are, therefore, entering the phase of the election where people are more frequently prodded to make up their minds. For a while over the past year, it did seem like Trump was the likely winner. That no longer seems to be the case. To an older person, it would seem strange to be having this conversation in the first place. Unemployment is low which favors the incumbent and the challenger is a convicted felon with more criminal trials up ahead. Perhaps we are headed not to a surprising or unusual outcome this November, therefore, but a conventional one.

—Gregor Macdonald