War Premia

Monday 23 June 2025

The U.S. bombing strike on Iran’s nuclear facilities could open up a Pandora’s box of problems for the region, or perhaps it will function as an exclamation point, bringing the Israeli attack to a close. We don’t have a good handle on Iran’s military reserves, and we especially don’t know what actions the regime will take. Iran might hunker down, but it may also lash out in the region, potentially catalyzing a wider war that brings in other players, like Saudi Arabia. A much easier call, prior to the president’s brief address to the nation Saturday night, was that the administration would be inclined to assert that no further action is contemplated, now that the nuclear enrichment facility at Fordo has been destroyed. And that’s essentially the message we received. There have long been fears in the U.S. about a potential war with Iran, and whether that would mean “boots on the ground.” For now, however, it’s probably best to go with the assumption that this administration wants nothing to do with such scenarios. Moreover, until otherwise indicated, one should favor the view that Iran is currently crippled.

Oil is likely to carry a price premium for a while, even if markets turn their attention to slower economic growth. Elevated prices for oil—even on the back of strong demand—can quickly convert to weakness when economic outlooks turn down, but that may not be the case here, at least for the balance of the summer. The reason is that there’s simply no escape from higher insurance rates infecting the market, and thus pushing up transportation costs. Yet another example of how insurance itself is a kind of truth teller.

But if oil prices stay elevated for too long, it could absolutely invite a crash. That’s in part because oil supply globally is quite robust right now. The IEA reported last week that inventories had been building rapidly, at a rate of 1 million barrels per day (mbpd) since February. Why might that be? Well, consider the downward revisions to global growth we’re seeing already from IMF and World Bank GDP forecasts. Trump’s doomed-to-fail tariffs were very much a global shock when unveiled in early April, and their effects are still winding their way through the system. When lumped all together, it’s understandable that some economists are concerned that in Q3—the 90-day period starting in July and running through the end of September—inflation readings could turn up as growth readings turn down.

A sure way for oil to get itself into trouble would be to carry a price premium for at least 6 to 8 weeks, only to find itself way overpriced by late August, when we start to see signs of further slowing in global growth. That could turn a price spike into a nasty crash, right when oil tends to be seasonally weaker anyway, around Labor Day.

Global markets were doing a decent job digesting Israel’s attack on Iran, but it’s a very different thing now that the U.S. has laid its hands upon the conflict. Despite the one-and-done assertion from the U.S. president over the weekend, it is still the case that Trump has become the first U.S. leader to actually drop bombs on the country, after 40 years in which that prospect remained limited to a mere possibility. Markets will regard this as something new. Let’s recall that some portion of Trump’s base is fully anti-war. So, setting aside the rationales for this limited action, Trump’s “big, beautiful, bunker-busting” will be regarded as a betrayal to many of his supporters.

Like oil, which is now fated to remain elevated in price, equity markets may be fated to travel along at a lower price for a while, until matters become more clear in the Gulf. As readers know, the U.S. indexes were getting into position to challenge the previous highs. And stock markets tend to be twitchy and nervous whenever they are nearing old highs, especially after a dramatic fall of the kind we endured in April and May. For example, on Monday, markets will probably have to face the fact that although the administration reportedly communicated to Iran that “the strikes are now done, and regime change is not a goal,” we have new, bellicose threats coming from Iran itself (closing the Strait of Hormuz, attacking U.S. bases) and Trump’s additional warning that Iran better not attack any U.S. assets, territory, or persons. It’s doubtful the market will be able to figure out that complicated math anytime soon.

Emissions growth is likely to weaken this year because the global economy is on a much softer path. The World Bank just cut its GDP forecast from 2.7% to 2.3%, and that follows the earlier cut from the IMF in April, marking down global growth from 3.3% to 2.7%. Both the World Bank and the IMF will update forecasts again, and the IMF has said that its coming assessment in late July will take into account further disruptions, including the extra tariffs on steel.

These forecasts do not yet include the conflict between Israel and Iran, of course, and in particular the strikes on Iran by the U.S. this weekend. Should oil start carrying a premium (to reflect higher shipping costs due to insurance rates), that would surely slow the global economy further. For reference, global GDP in 2023 advanced by 3.0% while emissions grew by 1.1%.

Without trying to quantify the relationship between global economic and emissions growth too precisely, we know that global GDP has steadily decarbonized in the current technology-driven era as greater portions of output are digital, service-based, intellectual, and far less industrial. In the 20th century, and even coming into the 21st century, the relationship between the marginal unit of global GDP and energy consumption (from fossil fuels) was still fairly tight. That relationship is now quite a bit looser, especially since 2010:

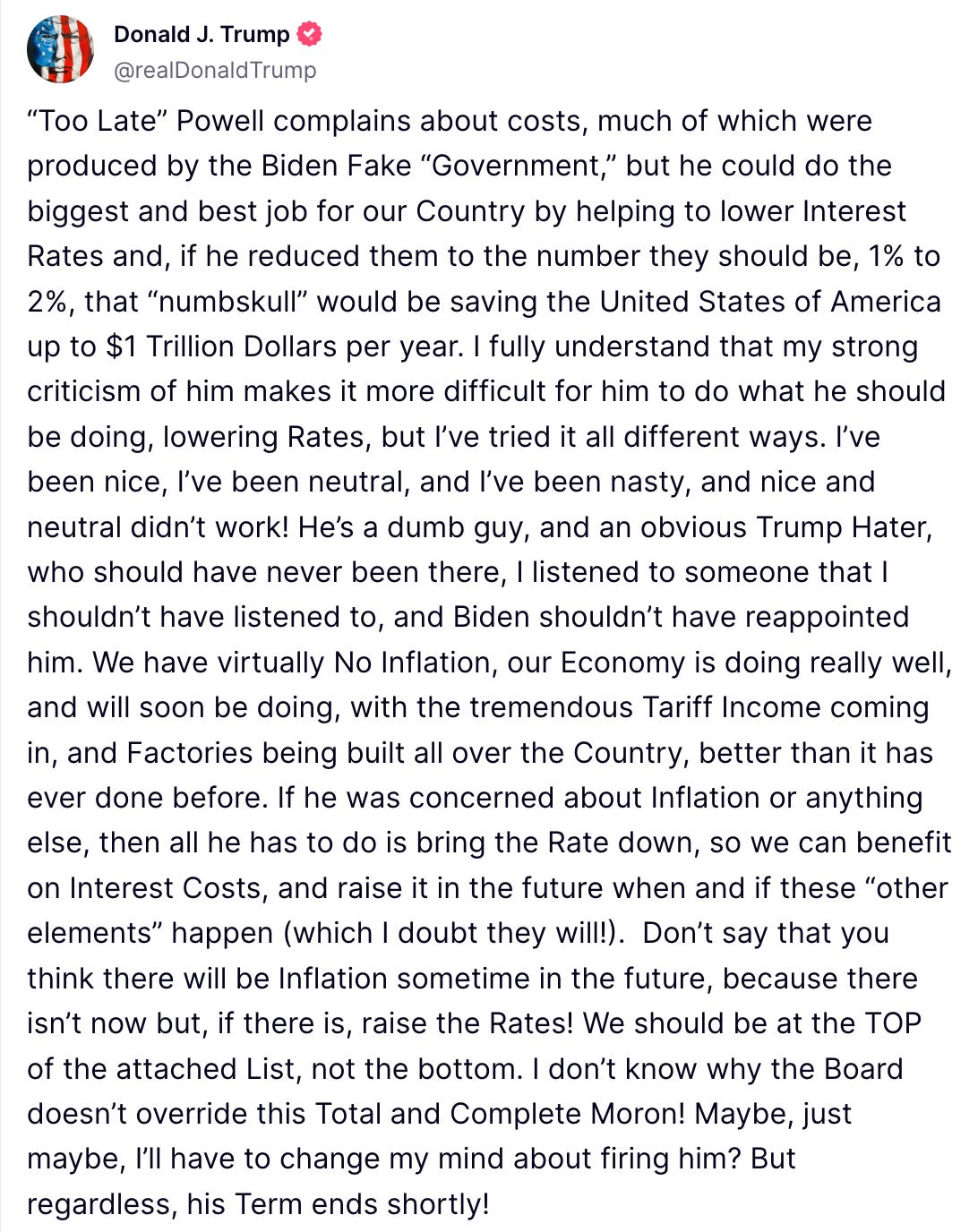

The Federal Reserve will soon be forced to choose between the threat of firmer inflation from tariffs, or a weakening job market. The forward march of soft economic data has pressed onward in recent weeks, and the Fed is now more explicit in saying it’s the tariffs themselves that are in the way of further rate cuts. At the press conference following the Fed’s decision to hold rates on Wednesday June 18, Chairman Powell must have said the word “tariff” at least 10 or 15 times, bringing the issue to center stage.

Did the president hear this signal? He sure did. Two days passed, and then the eruption took place on Friday, on his Truth Social account:

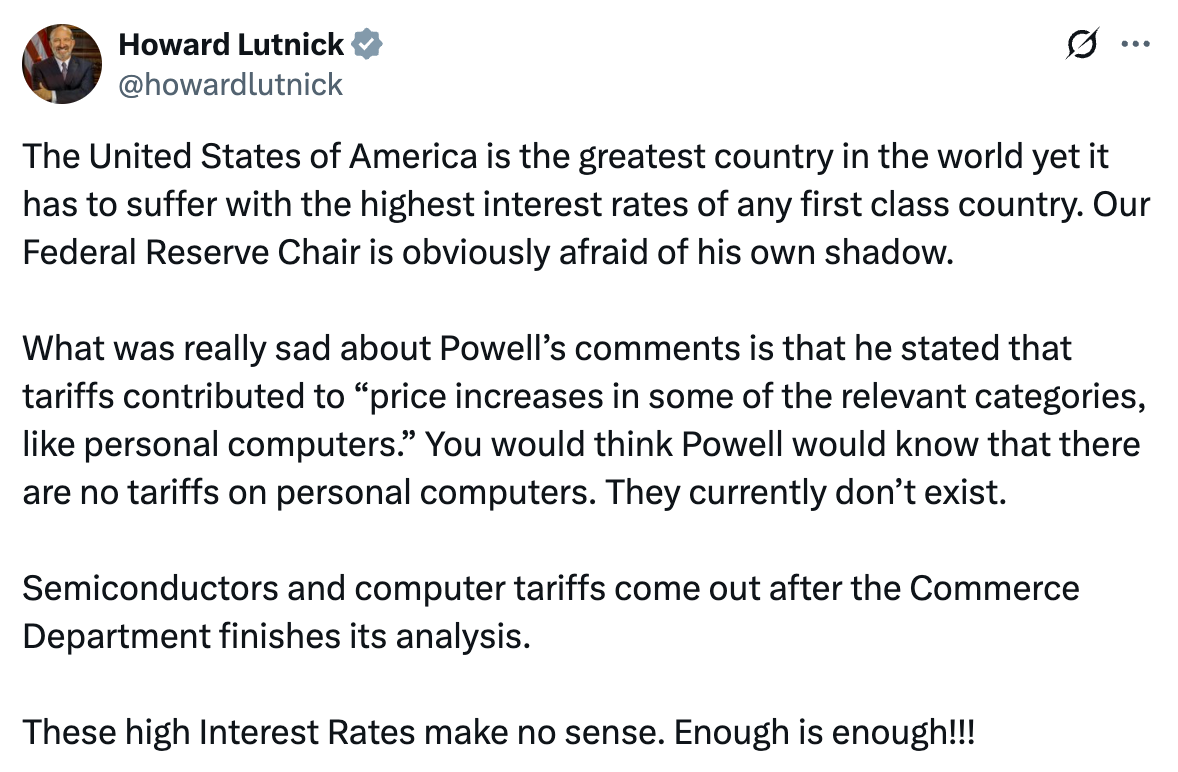

The flogging of tariffs as a complicating factor in setting monetary policy clearly got through not just to the president, but to Howard Lutnick, the hapless and clueless commerce secretary. He too took to social media, to complain bitterly about the tariff accusations. That makes sense, of course. No one has promoted tariffs more vigorously, nor done a worse job of explaining them.

Functionally, Powell’s strong assertions this week that tariffs risk inflationary pressure wound up acting as a kind of test of the administration’s touchy, defensive reactions to any criticism of the policy. Let’s also remember—even if it seems tangential—that when Musk and Trump had a falling-out and Musk accused Trump of being on the Epstein list, one of the bombs he lobbed toward the White House was “Ha ha, and the tariffs are already going to cause a recession in the second half of the year.” So we can conclude that tariff discourse inside the administration has likely not been uniform, and there has no doubt been some consternation about the potential damage the tariffs could wind up doing to the economy.

If it’s demonstrated in the July, August, and September inflation readings that tariffs have indeed started to flow through the system, pushing up prices, it’s certainly possible that the White House will panic, and actually withdraw from the policy more forcefully. It’s also possible that Powell and the Federal Reserve will also weigh in at such a juncture and make it even more explicit that if not for lingering tariffs, the Fed would be cutting already. The important takeaway is that we are coming into a major inflection point in the ongoing uncertainty over monetary policy, and these questions will undoubtedly be resolved by the end of the quarter (September 30, 2025).

By any reasonable measure, the Trump administration has done real damage to the US economy in both the near and medium term. And there is nothing constructive to show for any of their other policies, either. U.S. tourism is down, the U.S. Dollar is down, interest rates are stubbornly high, there is no plan to curb the growth of the deficit, the tariffs have delivered a shock to world trade, and now the administration hopes to pass a legislative tax and spending bill that’s skewed so hard in favor of high wage earners that it may actually wind up as an austerity bill, one that reduces the purchasing power of all the other tiers of income. Moreover, this is not to mention the structural damage done to the country’s future through the mindless reductions in research funding in health care, and other technologies.

One of the aspirational goals of the administration is to re-privatize the economy. Supposedly, the array of destructive policy actions is in service of that plan. But this intention lifts off from a profound misunderstanding: the US already runs a largely private economy, and our government spends money on defense, health care, and social safety nets that shore up our functioning as a nation. Indeed, when Johns Hopkins university takes in hundreds of millions of dollars each year for research in medicine, that contract is similar in nature to defense contracts handed out by the Defense Department. In other words, the US government already farms out myriad work to non-governmental entities, whether they be universities or corporations. There is no need to privatize the economy further.

Overall, we can think of the administration as having embarked on a number of bold policy initiatives which are entirely unsustainable. Tariffs have long since been adjudicated in the economics profession, which has understandably concluded they do damage while in place, while failing additionally to encourage much if any reshoring of manufacturing. The immigration raids as well are looking like the least efficient, most injurious form of deportation—something which the Biden, Obama, and Bush administrations all accomplished using normal rules of laws. It’s not going to be sustainable to keep running the ICE raids as they are. Consider: how many Americans will enjoy seeing another immigration raid on the news, if consumer prices are rising again as the economy slows? Now add higher gasoline prices to that mix. Serious question: have folks forgotten already what the price of gasoline did to the fortunes of Joe Biden?

Meanwhile, whether its discretionary wars on Harvard and Columbia universities, on government departments, or on legal immigrants, the court system is starting to fire back on all these efforts, curbing their reach, restoring positions in federal agencies, and releasing individuals from custody. The administration has very few wins, and lots of losses, and it’s only 6 months old. If Iran finds ways to retaliate, and Americans must endure a summer of high priced gasoline, and the Fed refuses to lower interest rates because of a new bump up in goods inflation, the White House could find itself in a rather difficult and unhappy place before this year comes to a close.

—Gregor Macdonald