War Weary

Monday 23 March 2026

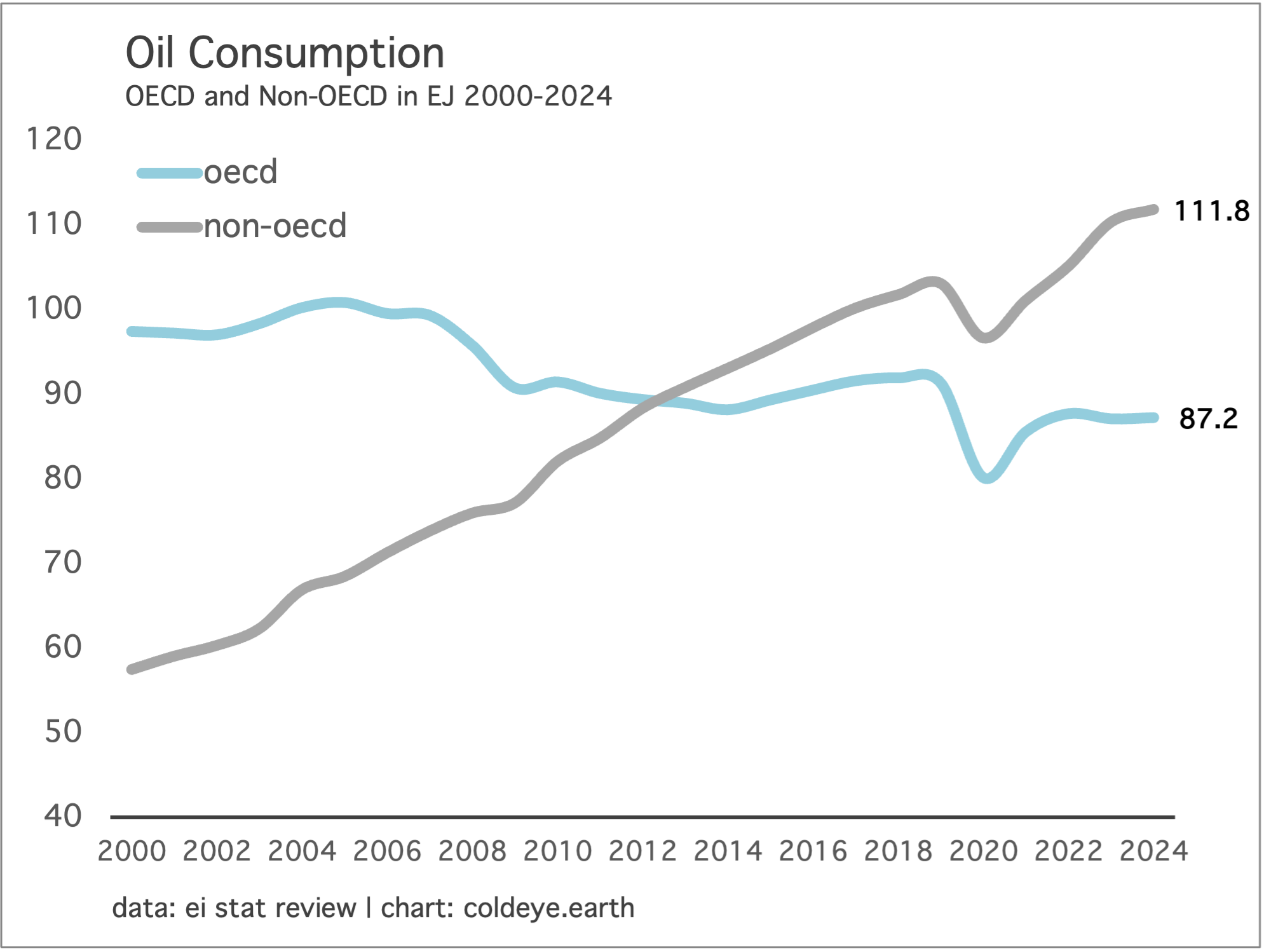

Forever is a long time. And yet the events now set in motion by the U.S. attack on Iran are likely to give way to a new energy security regime of very lengthy duration. While energy history is anchored by the great, singular transitions, it’s also the case that wars, embargoes, and shortages also play a reshaping role, cutting deep grooves in the psyches of nations and kicking off new policy regimes. In the aftermath of Russia’s attack on Ukraine, for example, the EU’s natural gas consumption stepped down about 20% from its 2021 highs; and that demand destruction has roughly been maintained as the EU has raced forward to adopt heat pumps and other gas-saving measures. Going back a bit further, the 2004—2008 global bull market in oil, which resolved into a fearsome spike, put a halt to decades-long OECD demand growth. And that growth never recovered (see chart below). Going even further back, oil enjoyed a dominant 50% share of all energy consumed in the world coming into the oil crises of the 1970s. Today? Oil has fallen to just a 33% share of total world energy consumption. Pain, as always, is a stern teacher.

When George H.W. Bush attacked Iraqi forces back in 1991, driving them out of Kuwait, he was criticized for not following up Desert Storm with a march on Baghdad. American hawks wanted Bush to “finish the job.” But Bush, among several considerations, understood that despite the serial tensions that defined the Middle East then (as now), a kind of equilibrium had long since formed around flows of oil from the Persian Gulf, and disturbing that equilibrium was far more likely to open up a box of furies, and other nasty surprises. Here we might recall the Odyssean dilemma, in which our hero has to navigate a strait and choose whether to sail closer to a six-headed monster, on one side of the passage, or a whirlpool on the other. Figuring the whirlpool was certain death, Odysseus sailed nearer to the monster, losing a few men in the process, but survived. March on Baghdad? No way, concluded Bush.

By attacking the country that owns the most beachfront real estate on the Strait of Hormuz, you might say that President Trump, by contrast, has sailed closer to the whirlpool. Everyone knows that Iran is a brutal theocracy and has been meddling and causing trouble since forever through its proxies around the region. Attacking Iran, however, with the intent to drive them into submission has pierced the stability of a system that is far larger than either the U.S. or Iran: the global economy, and its continued dependence on petroleum. Proper war planning for an attack on Iran ideally would have recognized that this larger system requires at least as much, if not more, attention and care than the direct attacks on the Iranian state.

What are some of the painful adjustments that therefore are likely to evolve as the risk premium around oil remains elevated for some time to come? Let’s go through some of the most obvious.

• In a repeat of 2022, global coal consumption is likely to soar. The pain point in 2022 was natural gas via the Russia-Ukraine war and Putin’s gas policies, but this time around it’s the reduction in Gulf LNG capacity that’s going to deliver a lot of pain to Asia. Global coal consumption reached a new all-time high in 2022—and then hit two more highs in 2023 and 2024—entirely undoing the moderate progress made in coal demand-reduction over the previous decade. A country like Japan, which has an enormous industrial base but must import energy to run it, is at great risk in this scenario. If Japan can’t get enough LNG, it will partly turn to coal, and you can apply that to other nations across Asia that manufacture but are dependent to some extent on imported energy. As someone quipped on the internet this week, maybe it’s time for Japan to do its part to clear the Strait of Hormuz:

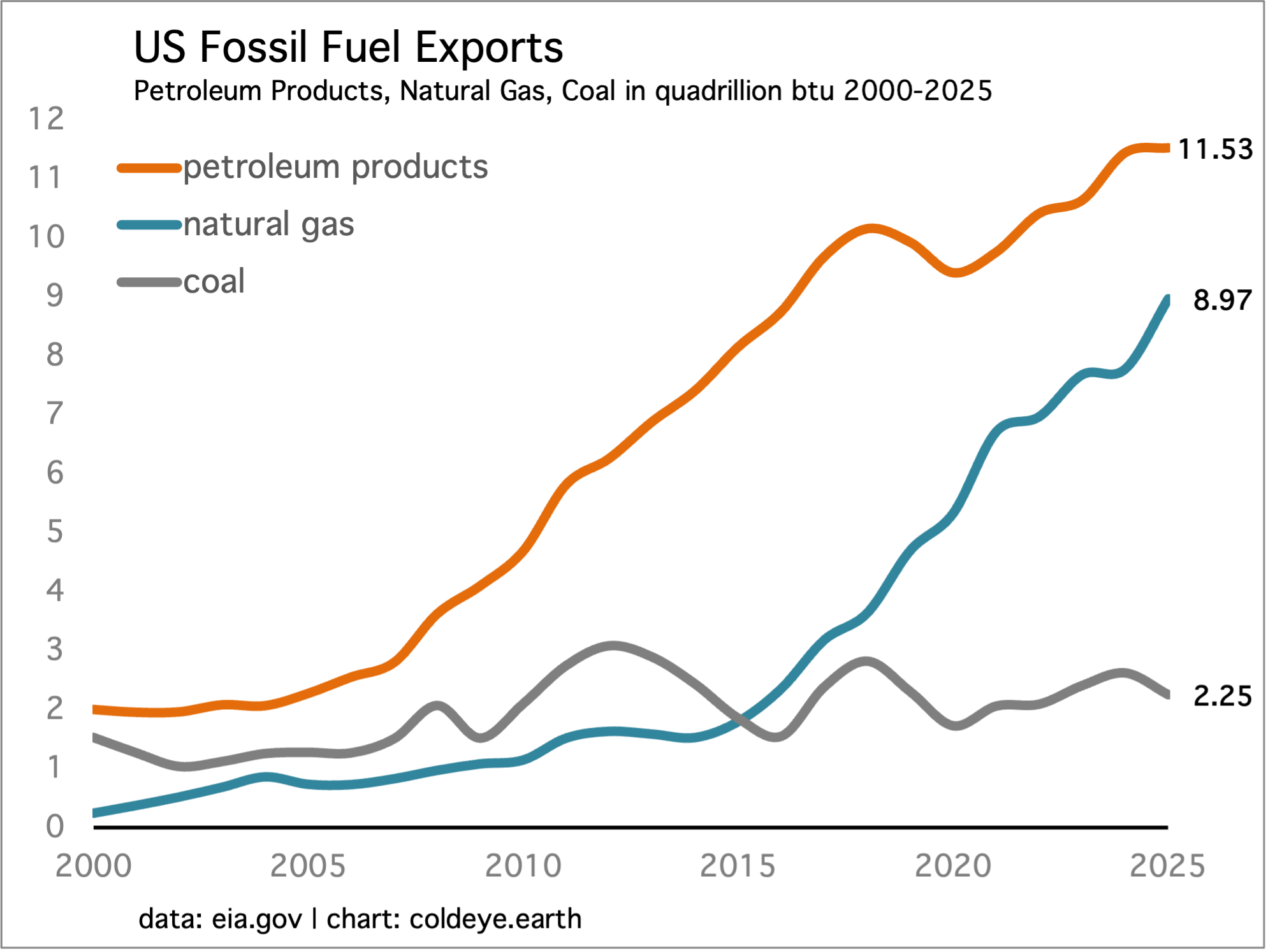

• U.S. exports of both coal and natural gas in the form of LNG will quickly rise to meet current export capacity; and if demand for those two fuels doesn’t let up, the U.S. energy economy will start exploring ways to expand that capacity. We must also remember that the U.S. has been expanding exports of both these fuels steadily over the past decade. U.S. coal exports have risen over this time partly due to the reduction in domestic demand. LNG capacity has risen in part because North America has economically recoverable natural gas reserves that are nothing less than gargantuan. So export momentum is already in the mix. Finally, U.S. petroleum product exports (not crude oil) may be constrained from increasing much as the combination of lower lower global supply but also lower global demand makes may offset each other. However, there’s no question that prices for those products will rise.

• Leaving aside the associated snarling of global supply chains that may constrain all production of any kind, demand for renewables and planning for more renewables will soar, along with demand for battery energy storage systems (BESS). The Iran war is shaping up to become a second major blow in less than five years to fossil fuel dependency in the power sector. The world will become weary. The Asian countries, led by India, are the domains where we are likely to see enormous jumps in renewables growth. China already builds renewables at a frantic pace, so the rate of change possible in China is far less. India, meanwhile, has a lot of catching up to do, and this probably triggers that long-overdue need to build new solar capacity.

Let’s pause here to remember a golden rule on which you can rely: Fossil fuel price shocks are a wonderful gift to producers of those fuels in the short term but are terrible for those producers in the long term. ‘Twas always thus.

Keep reading with a 7-day free trial

Subscribe to Cold Eye Earth to keep reading this post and get 7 days of free access to the full post archives.