The free market approach has turned the United States into nothing less than a 21st century colossus of global energy supply. Who could possibly claim there’s a problem here, which needs solving? The people who are about to come to power in the US, that’s who. With the election now behind us, the important idea which Cold Eye Earth seeks to highlight this week is that, when it comes to energy policy, overly strong executive power is a serious concern, but unreason and ideology are far more threatening. The incoming administration is populated by people who reliably base their arguments and policy plans on bizarre misreadings of the current landscape. They are passionate, and highly animated, in their attachment to ideological fantasy.

The United States runs a mostly free-market energy system of production, processing, consumption, and exports. Unlike many other commodity producing nations, the US places no resource-separation tax on production, and more broadly, most US energy activity takes place on private lands. A typical day in the life of American energy production sees landowners—farmers, ranchers, investors—collecting rents for the natural gas production, or wind power generation, or pipeline transmission, that occurs on their property. While the US energy industry as a whole certainly intersects frequently with federal and state regulations, on balance the industry is free to prospect for new oil and gas; new territory on which to place wind farms, solar arrays, or transmission lines; and explore regions to experiment with new forms of energy, like geo-thermal. One energy source that is indeed the focus of the most intense regulatory scrutiny is of course nuclear power. Nuclear is entirely dominated by the federal regulatory apparatus, but in contrast, the rest of the US energy sector doesn’t come under that level of governance. This matters because the public in general doesn’t understand that distinction. And the blur, the general fog that gathers around these distinctions is the entry point for the politics of energy in the US. If you are on the left, no one can convince you that we have enough regulation of energy. If you are on the right, you are certain we have too much.

A useful case to understand how the reality US of energy policy actually unfolds, in contrast to political beliefs and other misunderstandings, is the state of Texas. Over the past fifteen years, uneconomic coal-fired generation has contracted, new natural gas generation has expanded, and the production of oil, gas, wind power, and now solar power, have skyrocketed higher in Texas. The state has also seen an enormous expansion of petrochemical refining and processing volumes, along with LNG export capacity. LNG and refined petroleum product exports have played a big role in changing the country’s energy balance, as these exports from Texas have increasingly offset the country’s remaining, dwindling imports of energy. As the top producer of oil, natural gas, and wind power in the United States, Texas ranks 5th in global wind power production, produces 43% of US oil, and 27% of its natural gas.

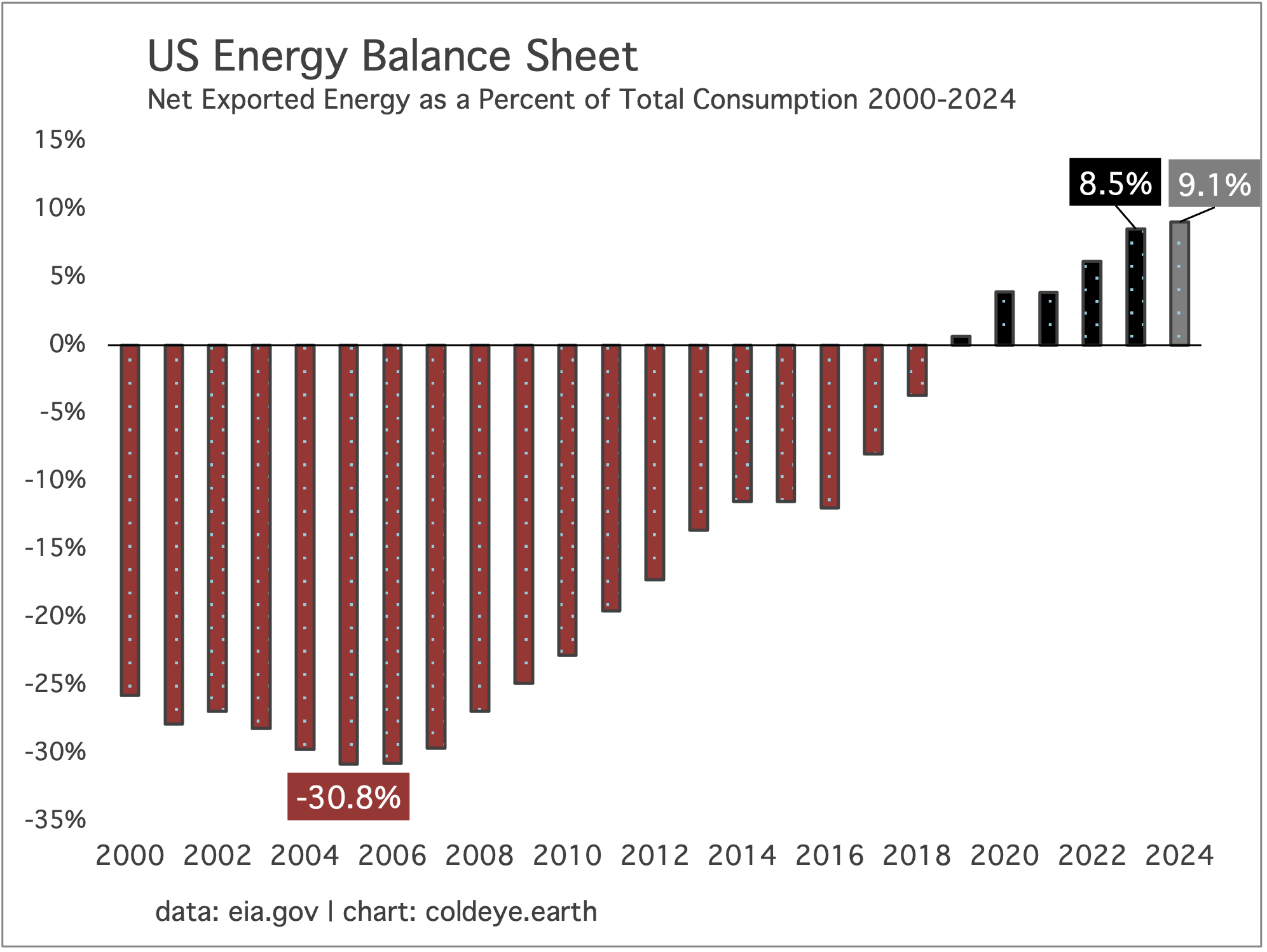

The US position in energy today looks unassailable. At home, we keep expanding the share of wind, solar, and batteries in the power system—which at the margin frees up more coal, and more natural gas for export. Abroad, our LNG export capacity has already been demonstrated to be an effective, geo-political management tool. Our oil production, which relentlessly keeps hitting new highs, has forced OPEC to continually pare back their own output, increasing OPEC spare capacity to a sustained, higher level. Moreover, the US is now fully energy independent, as we produce about 11-12 million barrels a day of crude oil, and additionally produce about 7-8 million barrels a day of petroleum liquids, which are key to the petrochemical industry. As longtime readers of this newsletter know, these enormous changes have unfolded steadily over the past 15 years, and now the US is a net exporter of energy. We preside over surpluses of coal and natural gas production, and our petrochemical complex pumps out products, also free for export. And look at the results:

Does the incoming administration understand that wind, solar, batteries, and electric vehicles all curtail domestic demand for oil, natgas, and coal—which can then be exported? Do they understand what energy independence actually means, and how it is constructed? Because according to them, US energy policy is one of the biggest fiascos of all time, and needs to be addressed almost on an emergency basis. For example, despite natural gas prices at 25 year lows in inflation-adjusted terms, and oil at 10 year lows also in inflation adjusted terms, their plan is to absolutely drench the market with even more oil and natural gas. How can the companies who produce oil and gas, and which have all seen stiff inflation in labor and equipment costs, survive such a plan? Like so many other “concepts of a plan” floated by the incoming administration—from chopping down health care, to raising tariffs—there is no follow-through to these policy assertions that contains any logic.

To pursue a course of unreason, the administration may find it has to contort itself into very strange shapes. Perhaps they could offer an above market rate price to oil companies to purchase their oil for a US reserve, while letting the market price fall steeply for consumers. The administration could also pull the geo-political lever, naturally embedded in LNG exports, to punish enemies, reward allies—or perhaps even, to punish allies. Perhaps the administration tends to push tariffs on solar panels to even higher levels, which would eventually increase domestic demand for natural gas, thus raising its price, and leaving less of a surplus for export. It’s important to remember that if you offered the current US position in energy to just about any administration from the past, Democrat or Republican, they would positively drool at the flexibility, and the power, our surplus production offers. And how would they respond? By doing nothing, mostly. Why would you want to mess up a good thing?

Presidents cannot defy gravity forever, and market realities will eventually intrude. Historically, presidential power over energy markets has been far more curtailed than many assume, as campaign promises can fade quickly in the face of difficulties and challenges. Readers may want to review last year’s overview of this phenomenon, Energy and the Presidents, to learn how rare it is for any incoming administration to use brute force to change the course of the energy sector. All four presidents you see below found that trends already in place were no match for their intentions. George W. Bush was an oil man from Texas who was certain to unleash American fossil fuel production. Instead, US oil production sank to a historic nadir under his watch, and the global economy got smacked hard with a classic oil crunch. Barack Obama was the first climate-forward president, and while he did set in motion good growth for wind and solar, total fossil fuel production and US energy made the biggest move higher in 50 years, under his watch. Trump was certain to save US coal. The trend towards lower coal consumption and coal plant retirements pressed onward, completely unaware of the president’s words. The Biden administration has been almost a perfect echo of the Obama years: solid policy progress to expand renewables, with terrific legislation now in place, but US natural gas and oil production has never been higher. Caveat Emptor: predicting what will occur with US energy under any president is not easy.

Energy and the Presidents

Energy transition has spawned a populist myth that governments around the world are inhibiting production of fossil fuels. The climate community only wishes that were true. There are no efforts in Canada, Australia, the United States, Mexico, South America or elsewhere in the OECD where policies, new or old, are acting to meaningfully constrain fossil fuel production. And there are certainly no climate or ESG policies at work in the Non-OECD—in China, Russia, or the Mideast constraining production in these regions either. You really have to laugh at the idea that high profile climate figures like Greta Thunberg have dissuaded, say, coal production. The climate community just spent the last seven years believing global coal production and consumption had peaked, back in 2014. Nope. In 2021, demand reached back to near all-time highs, and global coal production actually did reach a new high. And so did natural gas.

There’s nothing the Trump administration can do to boost oil demand, because the trend towards slow demand growth has been in place for years. Moreover, the dynamics of revenge and encirclement open up the possibility that much of the western world, in reaction to a Trump presidency, may go even harder against oil consumption. And, if a Trump presidency imposes itself harshly enough on the American people, we have to consider the possibility that Americans—not all Americans—will also undertake personal actions to avoid, where possible, the consumption of oil. Indeed, there are already whispers that some actors in the US oil and gas industry are concerned about becoming overly identified with a Trump presidency, perhaps for this very reason. Sorry guys, probably too late for that.

Behind all these machinations lies the uncomfortable truth that rather than being short oil, the world has too much oil. Cold Eye Earth is here to remind that OPEC spare capacity, far from being an arcane measure, has been one of the most reliable factors over two decades in the pricing of oil. When OPEC spare capacity is sustainably low, as it was in the early 2000’s, it added greatly to that powerful bull market in oil prices during that period. The reason is so incredibly simple: the oil futures market sleeps easy when OPEC spare capacity is high, and tosses and turns all night when capacity is low.

Perhaps you have noticed this year that every time oil tries to mount a price recovery, it soon fails and we fall back either into the low 70’s or high 60’s. The main reason: there is too much OPEC spare capacity. The oil futures market does its job, looking into the future, and here is what it sees: even if demand were to suddenly move higher, there is a ton of OPEC spare capacity that can be turned on to meet that demand, before we arrive at any tightness in the market. The black, horizontal line in the chart above can be thought of as the sleep easy/toss-and-turn dividing line. If you are making oil forecast calls, before wasting your time with loadings at Singapore, Saudi offering prices, and other previously important measures like US inventories, always check first with OPEC spare capacity.

The greatest risk to investors in renewables will come not from Trump energy policies per se, but the economic chaos that could ensue from a string of ideological (and bad) decisions around the macro economy and geo-politics. The incoming administration has big, ambitious plans to deport millions of people, cut taxes, raise tariffs, and attack social programs from healthcare to social security. These are not pro-growth notions, to put it mildly. Somewhere along the way, markets will balk. If the administration undertakes a light version of these stated policies, then so be it. But if it pursues the hard version, then markets will have a say.

For those of you old enough to remember, the bond market has at certain moments played a key role in American policy making by giving a big thumbs down to excessive spending plans, or stimulus. By doing so, the bond market proved itself to be a powerfully influential player, and the actors behind it were dubbed the bond vigilantes. Indeed, James Carville the political consultant famously quipped that if he were ever to be reincarnated, he’s like to come back as the bond market, so that he could “intimidate the hell out of everybody.”

In recent decades, however, the market that has corralled, constrained, and cowed politicians is the stock market. The US equity market is of course the common fabric in American retirement plans, and it also tends to act as a daily news barometer of the economy. Because markets are essentially the free-flow of information, they tend to wind up in opposition to politicians who lie about everything, or who try to jackhammer their way to outcomes which are, at bottom, unachievable.

One curious and surprising outcome to the next four years, therefore, may be that many liberals become more friendly to markets, as they increasingly come to realize that markets act like a regulatory governor to all the steam and heat that pours forth from a reckless administration. Markets are of course roaring right now—an extension of the current bull market—as they digest all the initial goodies, like tax rates, that are about to arrive. But next year, markets will deliver verdicts on all the plans outside of tax cuts, and that will be a momentous juncture indeed.

—Gregor Macdonald